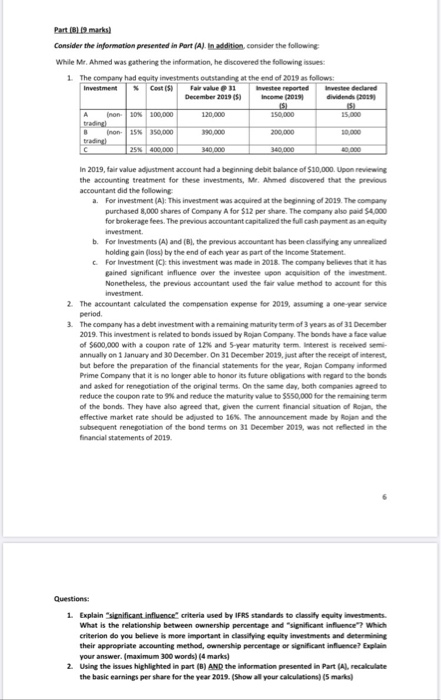

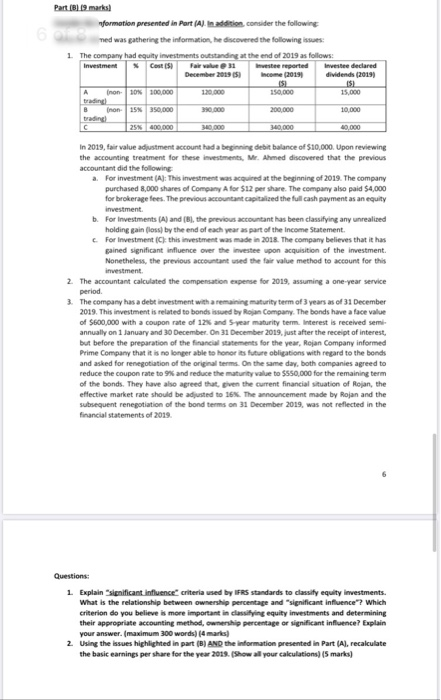

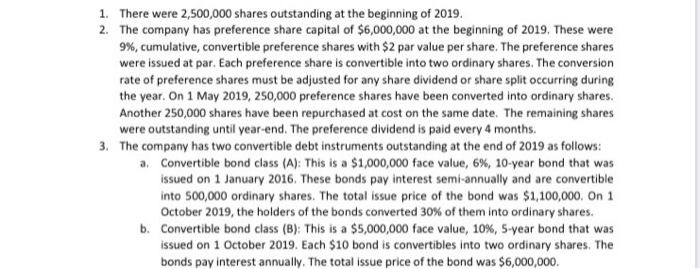

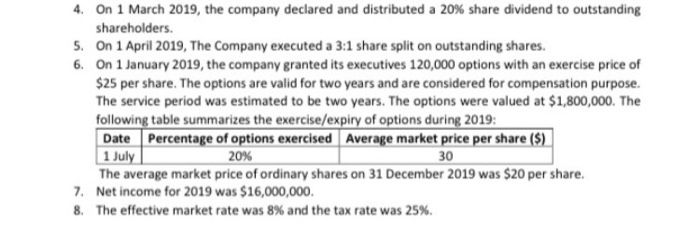

Part 1.marks Consider the information presented in Part (Al. In addition consider the following While Mr. Ahmed was gathering the information, he discovered the following 1 The company had equity investments outstanding at the end of 2019 follow Cost Fair value 11 Interported December 2015 declared 120.000 2 in 2019, avaldustment account had a beginning de hace of $10.000 Ubon g the accounting treatment for these investments, M e discovered that the previous accountant did the following For investment (A): This investment was corred at the being of 2019. The cony purchased 8.000 shares of Company A for $12 per share. The company pod 4.000 for brokerage fees. The previous accountant capitalized the cash payment met investment b. For investments (A) and the previous accountant has been classifying an d holding in loss) by the end of each year as part of the income Statement For investment is this investment was made in 2016. The company believes that has gained significant influence over the investee on siin of the weet Nonetheless, the previous accountant used the value method to account for this investment The accountant calculated the compensation expense for 2019, assuming a one- service period The company has a debt investment with a remaining maturity term of years as of 31 December 2019. This investment is related to bonds issued by Rojan Company. The bonds have a face value of $600,000 with a coupon rate of 12 and 5 year maturity term interest is received annually on 1 January and 30 December. On 31 December 2019, just after the receipt oftest but before the preparation of the financial statements for the year, Rojan Company formed Prime Company that it is no longer able to honor its future obligations with regard to the bonds and asked for renegotiation of the original terms. On the same day, both companies agreed to reduce the coupon rate to and reduce the maturity value to SS50,000 for the remaining term of the bonds. They have also agreed that given the current financial station of the effective market rate should be adjusted to 16%. The announcement made by and the subsequent renegotiation of the bond terms on 31 December 2019, was not reflected in the financial statements of 2019 Questions: 1. Explain Significant influence criteria used by IFRS standards to classily equity investments What is the relationship between ownership percentage and can influence which criterion de you believe is more important in classifying equity investments and determ their appropriate accounting method, ownership percentage or significant influence Exp your answer. maximum 100 words) (4 marks) 2. Using the issues highlighted in part() AND the information presented in Part IAL recalculate the basic earnings per share for the year 2019. (Show all your calculations) (5 m ) PartBl 19. mars formation presented in Port (Allnation consider the following ned was gathering the information, he discovered the following issues 1 The company had equity investments outstanding at the end of 2019 as follows: Cost Fare este declared December 2009 S 30 2 In 2019, far vale m ent account ada begg e balance of $10,000. Upon reviewing the accounting treatment for the Armed discovered that the previous c and the following a for investment . This investment w o rdt the beginning of 2019. The company purchased 1.000 shares of Company for $12 share. The company also paid $4.000 for brokerage fees. The previous contained the cash payment as an equity investment For investment and the previous accountant has been casing any read holding by the end of each part of the income Statement For investment this investment w a de 2016. The company believes that it has gained significant influence over the rest on acquisition of the investment Nonetheless, the previous account wed the value method to account for this investment The accountant calculated the compensation expense for 2019, assuming a one-year service period The company has a debt investment with a re m aturity term of 3 years as of 31 December 2019. This investment is related to bond e d by Ron Company. The bonds have a face value of $600,000 with a coupon rate of 12 and armaturity term interest is received sem annually on 1 January and 30 December. On 31 December 2019. just after the receipt of interest, but before the preparation of the financial statements for the year, Rajan Company informed Prime Company that it is no longer able to honor future obligations with regard to the bonds and asked for renegotiation of the original terms. On the same day, both companies agreed to reduce the coupon rate to and reduce the maturity wall to $550,000 for the remaining term of the bonds. They have also agreed that even the current financial station of Rojan, the effective market rate should be adjusted to 16 The wouncement made by Rojan and the subsequent renegotiation of the bond terms on 31 December 2019, was not reflected in the financial statements of 2019 1 Explain Significant influence criteria used by IFRS standards to classify equity Investments What is the relationship between percentage and ficant influence? Which criterion do you believe is more important in s ing equity investments and determining their appropriate accounting method, w h percentage orificant influence? Explain your answer maximum 100 words) 14 mars 2. Using the h i ghlighted in part (8) AND the information presented in Part (Al, recalculate the basic earnings per share for the year 2015. Show all your calculations (5 marks) Read the scenario parts (A) and (B) and answer the questions at the end of each part. Assignment Scenario: Part (A) (16 Marks) Mr. Ahmed is a fresh accounting graduate. He has been employed by a big industrial company in the country; (Prime Company). The company is specialized in manufacturing primary care equipment for various entities in the country. The company is focused on the local market with about 90% of the sales are made for local entities. The company is listed on the local securities market. It is the end of 2019 and Mr. Ahmed was asked to calculate the basic and diluted earnings per share figures for the company. Given the importance of the earnings per share figure to the company and the market, as a performance measure, Mr. Ahmed was keen to do the job properly. Therefore, he started gathering relevant information to be able to calculate these two figures. The following is a summary of the information he gathered: 1. There were 2,500,000 shares outstanding at the beginning of 2019. 2. The company has preference share capital of $6,000,000 at the beginning of 2019. These were 9%, cumulative, convertible preference shares with $2 par value per share. The preference shares were issued at par. Each preference share is convertible into two ordinary shares. The conversion s must be adjusted for any share dividend or share split occurring during 9, 250,000 preference shares have been converted into ordinary shares. Another 250,000 shares have been repurchased at cost on the same date. The remaining shares were outstanding until year-end. The preference dividend is paid every 4 months 3. The company has two convertible debt instruments outstanding at the end of 2019 as follows: a. Convertible bond class (A): This is a $1,000,000 face value, 6%, 10-year bond that was issued on 1 January 2016. These bonds pay interest semi-annually and are convertible into 500,000 ordinary shares. The total issue price of the bond was $1,100,000. On 1 October 2019, the holders of the bonds converted 30% of them into ordinary shares. b. Convertible bond class (B): This is a $5,000,000 face value, 10%, 5-year bond that was issued on 1 October 2019. Each $10 bond is convertibles into two ordinary shares. The bonds pay interest annually. The total issue price of the bond was $6,000,000 4. On 1 March 2019, the company declared and distributed a 20% share dividend to outstanding shareholders. 5. On 1 April 2019, The Company executed a 3:1 share split on outstanding shares. 6. On 1 January 2019, the company granted its executives 120,000 options with an exercise price of $25 per share. The options are valid for two years and are considered for compensation purpose. The service period was estimated to be two years. The options were valued at $1,800,000. The following table summarizes the exercise/expiry of options during 2019: Date Percentage of options exercised Average market price per share ($) 1 July 20% 30 The average market price of ordinary shares on 31 December 2019 was $20 per share. 7. Net income for 2019 was $16,000,000 8. The effective market rate was 8% and the tax rate was 25%. Questions: 1. The earnings per share figure is one of the most important accounting-based figures to be reported, especially for publicly listed companies such as Prime Company. Explain why. (Maximum 250 words). (3 marks) 2. Do you believe that the earnings per share is also important for privateon-public companies? Explain your answer (maximum 200 words) (2 marks) 3. Using the information in PART (A) above, calculate the following a. The basic earnings per share for the year 2019. (Show all your calculations) (4 marks) b. The diluted earnings per share for the year 2019. (Show all your calculations) (7 marks) Part (B) (9 marks) Consider the information presented in Part (A). In addition, consider the following: While Mr. Ahmed was gathering the information, he discovered the following issues: 1. The company had equity investments outstanding at the end of 2019 as follows: Investment % Cost ($) Fair value @31 Investee reported investee declared December 2019 ($) Income (2019) dividends (2019) ($) A (non- 10% 100,000 120,000 150,000 15,000 trading) (non 15% 350,000 390,000 200,000 10,000 trading) 25% 400,000 340,000 340,000 40,000 In 2019, fair value adjustment account had a beginning debit balance of $10,000. Upon reviewing the accounting treatment for these investments, Mr. Ahmed discovered that the previous accountant did the following: a. For investment (A): This investment was acquired at the beginning of 2019. The company purchased 8,000 shares of Company A for $12 per share. The company also paid $4,000 for brokerage fees. The previous accountant capitalized the full cash payment as an equity investment. b. For Investments (A) and (B), the previous accountant has been classifying any unrealized holding gain (loss) by the end of each year as part of the Income Statement. c. For Investment (C): this investment was made in 2018. The company believes that it has gained significant influence over the investee upon acquisition of the investment. Nonetheless, the previous accountant used the fair value method to account for this investment Questions: 1. Explain "significant influence" criteria used by IFRS standards to classify equity investments. What is the relationship between ownership percentage and "significant influence"? Which criterion do you believe is more important in classifying equity investments and determining their appropriate accounting method, ownership percentage or significant influence? Explain your answer. (maximum 300 words) (4 marks) highlighted in part (B) AND the information presented in Part (A), recalculate the basic earnings per share for the year 2019. (Show all your calculations) (5 marks) Part 1.marks Consider the information presented in Part (Al. In addition consider the following While Mr. Ahmed was gathering the information, he discovered the following 1 The company had equity investments outstanding at the end of 2019 follow Cost Fair value 11 Interported December 2015 declared 120.000 2 in 2019, avaldustment account had a beginning de hace of $10.000 Ubon g the accounting treatment for these investments, M e discovered that the previous accountant did the following For investment (A): This investment was corred at the being of 2019. The cony purchased 8.000 shares of Company A for $12 per share. The company pod 4.000 for brokerage fees. The previous accountant capitalized the cash payment met investment b. For investments (A) and the previous accountant has been classifying an d holding in loss) by the end of each year as part of the income Statement For investment is this investment was made in 2016. The company believes that has gained significant influence over the investee on siin of the weet Nonetheless, the previous accountant used the value method to account for this investment The accountant calculated the compensation expense for 2019, assuming a one- service period The company has a debt investment with a remaining maturity term of years as of 31 December 2019. This investment is related to bonds issued by Rojan Company. The bonds have a face value of $600,000 with a coupon rate of 12 and 5 year maturity term interest is received annually on 1 January and 30 December. On 31 December 2019, just after the receipt oftest but before the preparation of the financial statements for the year, Rojan Company formed Prime Company that it is no longer able to honor its future obligations with regard to the bonds and asked for renegotiation of the original terms. On the same day, both companies agreed to reduce the coupon rate to and reduce the maturity value to SS50,000 for the remaining term of the bonds. They have also agreed that given the current financial station of the effective market rate should be adjusted to 16%. The announcement made by and the subsequent renegotiation of the bond terms on 31 December 2019, was not reflected in the financial statements of 2019 Questions: 1. Explain Significant influence criteria used by IFRS standards to classily equity investments What is the relationship between ownership percentage and can influence which criterion de you believe is more important in classifying equity investments and determ their appropriate accounting method, ownership percentage or significant influence Exp your answer. maximum 100 words) (4 marks) 2. Using the issues highlighted in part() AND the information presented in Part IAL recalculate the basic earnings per share for the year 2019. (Show all your calculations) (5 m ) PartBl 19. mars formation presented in Port (Allnation consider the following ned was gathering the information, he discovered the following issues 1 The company had equity investments outstanding at the end of 2019 as follows: Cost Fare este declared December 2009 S 30 2 In 2019, far vale m ent account ada begg e balance of $10,000. Upon reviewing the accounting treatment for the Armed discovered that the previous c and the following a for investment . This investment w o rdt the beginning of 2019. The company purchased 1.000 shares of Company for $12 share. The company also paid $4.000 for brokerage fees. The previous contained the cash payment as an equity investment For investment and the previous accountant has been casing any read holding by the end of each part of the income Statement For investment this investment w a de 2016. The company believes that it has gained significant influence over the rest on acquisition of the investment Nonetheless, the previous account wed the value method to account for this investment The accountant calculated the compensation expense for 2019, assuming a one-year service period The company has a debt investment with a re m aturity term of 3 years as of 31 December 2019. This investment is related to bond e d by Ron Company. The bonds have a face value of $600,000 with a coupon rate of 12 and armaturity term interest is received sem annually on 1 January and 30 December. On 31 December 2019. just after the receipt of interest, but before the preparation of the financial statements for the year, Rajan Company informed Prime Company that it is no longer able to honor future obligations with regard to the bonds and asked for renegotiation of the original terms. On the same day, both companies agreed to reduce the coupon rate to and reduce the maturity wall to $550,000 for the remaining term of the bonds. They have also agreed that even the current financial station of Rojan, the effective market rate should be adjusted to 16 The wouncement made by Rojan and the subsequent renegotiation of the bond terms on 31 December 2019, was not reflected in the financial statements of 2019 1 Explain Significant influence criteria used by IFRS standards to classify equity Investments What is the relationship between percentage and ficant influence? Which criterion do you believe is more important in s ing equity investments and determining their appropriate accounting method, w h percentage orificant influence? Explain your answer maximum 100 words) 14 mars 2. Using the h i ghlighted in part (8) AND the information presented in Part (Al, recalculate the basic earnings per share for the year 2015. Show all your calculations (5 marks) Read the scenario parts (A) and (B) and answer the questions at the end of each part. Assignment Scenario: Part (A) (16 Marks) Mr. Ahmed is a fresh accounting graduate. He has been employed by a big industrial company in the country; (Prime Company). The company is specialized in manufacturing primary care equipment for various entities in the country. The company is focused on the local market with about 90% of the sales are made for local entities. The company is listed on the local securities market. It is the end of 2019 and Mr. Ahmed was asked to calculate the basic and diluted earnings per share figures for the company. Given the importance of the earnings per share figure to the company and the market, as a performance measure, Mr. Ahmed was keen to do the job properly. Therefore, he started gathering relevant information to be able to calculate these two figures. The following is a summary of the information he gathered: 1. There were 2,500,000 shares outstanding at the beginning of 2019. 2. The company has preference share capital of $6,000,000 at the beginning of 2019. These were 9%, cumulative, convertible preference shares with $2 par value per share. The preference shares were issued at par. Each preference share is convertible into two ordinary shares. The conversion s must be adjusted for any share dividend or share split occurring during 9, 250,000 preference shares have been converted into ordinary shares. Another 250,000 shares have been repurchased at cost on the same date. The remaining shares were outstanding until year-end. The preference dividend is paid every 4 months 3. The company has two convertible debt instruments outstanding at the end of 2019 as follows: a. Convertible bond class (A): This is a $1,000,000 face value, 6%, 10-year bond that was issued on 1 January 2016. These bonds pay interest semi-annually and are convertible into 500,000 ordinary shares. The total issue price of the bond was $1,100,000. On 1 October 2019, the holders of the bonds converted 30% of them into ordinary shares. b. Convertible bond class (B): This is a $5,000,000 face value, 10%, 5-year bond that was issued on 1 October 2019. Each $10 bond is convertibles into two ordinary shares. The bonds pay interest annually. The total issue price of the bond was $6,000,000 4. On 1 March 2019, the company declared and distributed a 20% share dividend to outstanding shareholders. 5. On 1 April 2019, The Company executed a 3:1 share split on outstanding shares. 6. On 1 January 2019, the company granted its executives 120,000 options with an exercise price of $25 per share. The options are valid for two years and are considered for compensation purpose. The service period was estimated to be two years. The options were valued at $1,800,000. The following table summarizes the exercise/expiry of options during 2019: Date Percentage of options exercised Average market price per share ($) 1 July 20% 30 The average market price of ordinary shares on 31 December 2019 was $20 per share. 7. Net income for 2019 was $16,000,000 8. The effective market rate was 8% and the tax rate was 25%. Questions: 1. The earnings per share figure is one of the most important accounting-based figures to be reported, especially for publicly listed companies such as Prime Company. Explain why. (Maximum 250 words). (3 marks) 2. Do you believe that the earnings per share is also important for privateon-public companies? Explain your answer (maximum 200 words) (2 marks) 3. Using the information in PART (A) above, calculate the following a. The basic earnings per share for the year 2019. (Show all your calculations) (4 marks) b. The diluted earnings per share for the year 2019. (Show all your calculations) (7 marks) Part (B) (9 marks) Consider the information presented in Part (A). In addition, consider the following: While Mr. Ahmed was gathering the information, he discovered the following issues: 1. The company had equity investments outstanding at the end of 2019 as follows: Investment % Cost ($) Fair value @31 Investee reported investee declared December 2019 ($) Income (2019) dividends (2019) ($) A (non- 10% 100,000 120,000 150,000 15,000 trading) (non 15% 350,000 390,000 200,000 10,000 trading) 25% 400,000 340,000 340,000 40,000 In 2019, fair value adjustment account had a beginning debit balance of $10,000. Upon reviewing the accounting treatment for these investments, Mr. Ahmed discovered that the previous accountant did the following: a. For investment (A): This investment was acquired at the beginning of 2019. The company purchased 8,000 shares of Company A for $12 per share. The company also paid $4,000 for brokerage fees. The previous accountant capitalized the full cash payment as an equity investment. b. For Investments (A) and (B), the previous accountant has been classifying any unrealized holding gain (loss) by the end of each year as part of the Income Statement. c. For Investment (C): this investment was made in 2018. The company believes that it has gained significant influence over the investee upon acquisition of the investment. Nonetheless, the previous accountant used the fair value method to account for this investment Questions: 1. Explain "significant influence" criteria used by IFRS standards to classify equity investments. What is the relationship between ownership percentage and "significant influence"? Which criterion do you believe is more important in classifying equity investments and determining their appropriate accounting method, ownership percentage or significant influence? Explain your answer. (maximum 300 words) (4 marks) highlighted in part (B) AND the information presented in Part (A), recalculate the basic earnings per share for the year 2019. (Show all your calculations)