Answered step by step

Verified Expert Solution

Question

1 Approved Answer

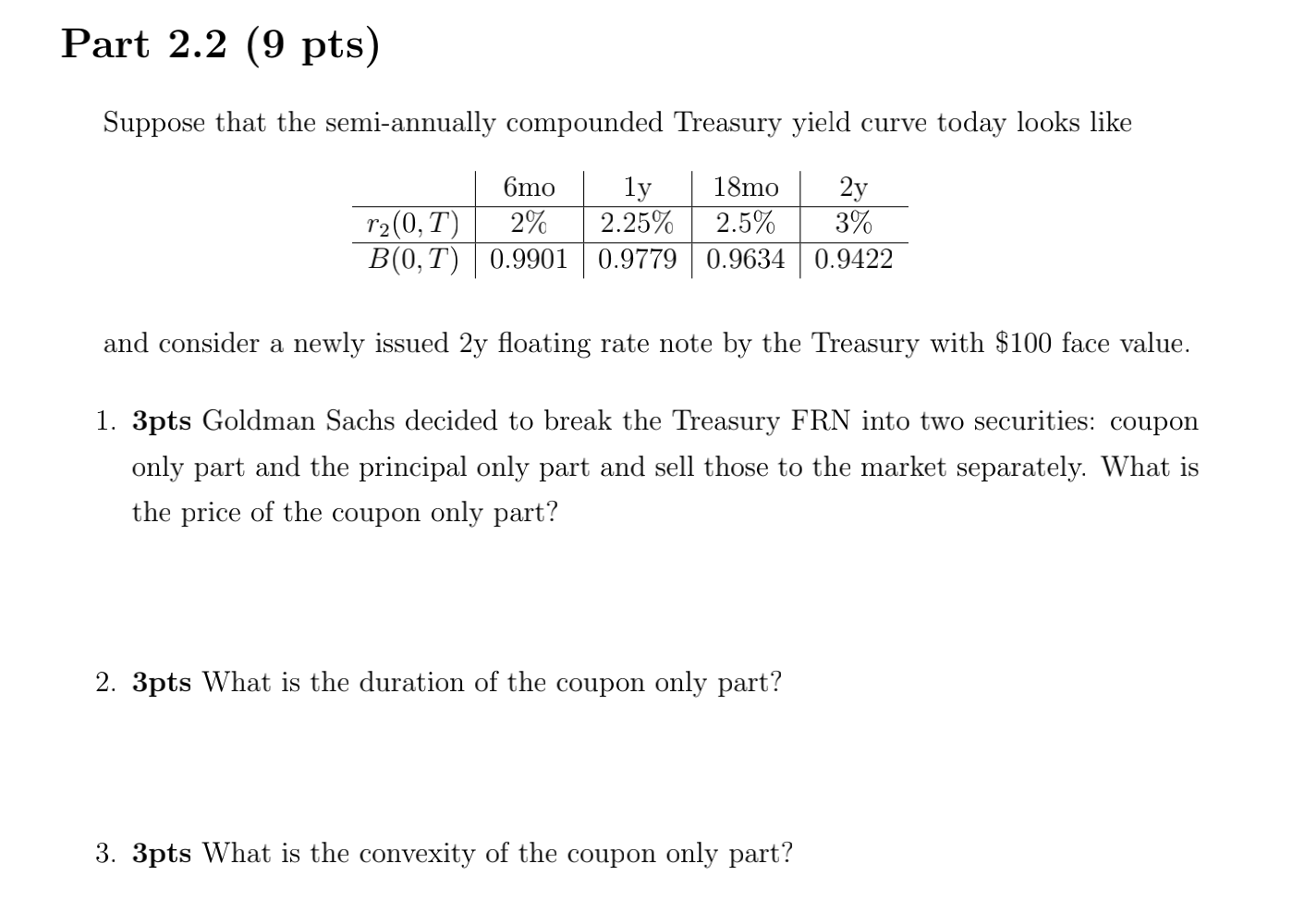

Part 2.2 (9 pts) Suppose that the semi-annually compounded Treasury yield curve today looks like 6mo ly 18mo 2y r2(0,T) 2% 2.25% 2.5% 3% B(0,T)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Trading From Your Gut How To Use Right Brain Instinct And Left Brain Smarts To Become A Master Trader

Authors: Curtis Faith

1st Edition

0137047681,0137051689