Part 3: In a continuation of their efforts to explore the financial condition of ABC Company, the Board of Directors has now started to explore the various investment strategies of the company. They would like to understand more about the differences between debt versus equity investments. They also wish to learn more about the various types of investments reported on the Balance Sheet. Using your text and outside sources, explain the following: (1) debt versus equity securities; (2) various types of investments such as those listed in Exhibit 15-2; and (3) how to account for these investments (refer to Exhibit 15-8 as a guide). Keep in mind the intended audience of the memo.

| To: | |

| From: | [Student Name] |

| Date: | [Enter Date] |

| Subject: | [Enter Subject] |

| |

Reference:

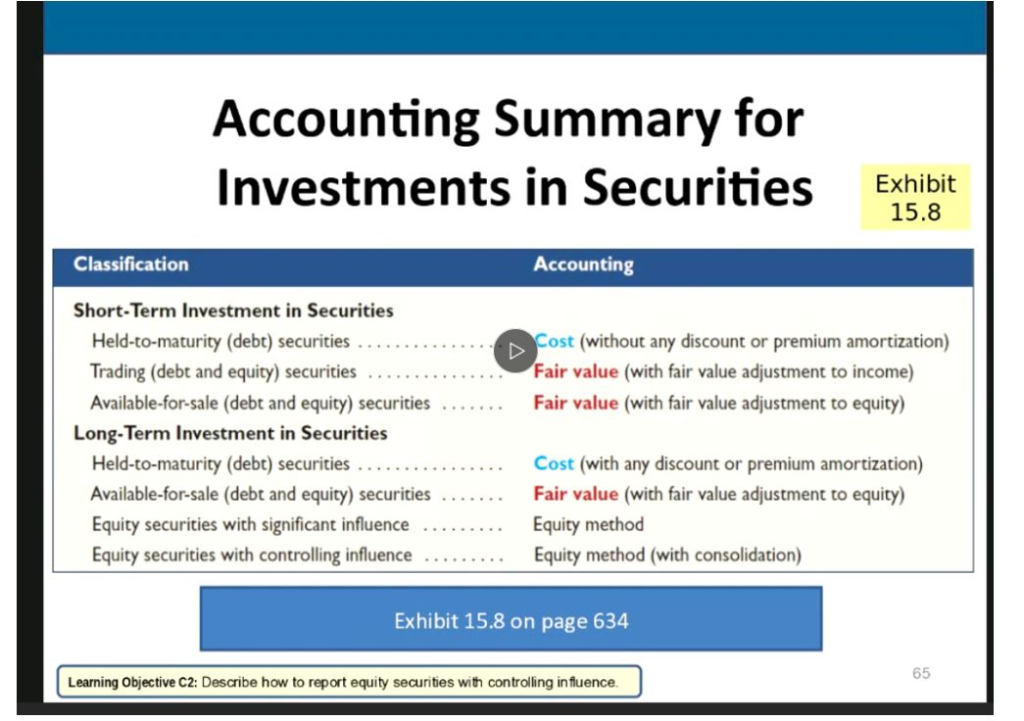

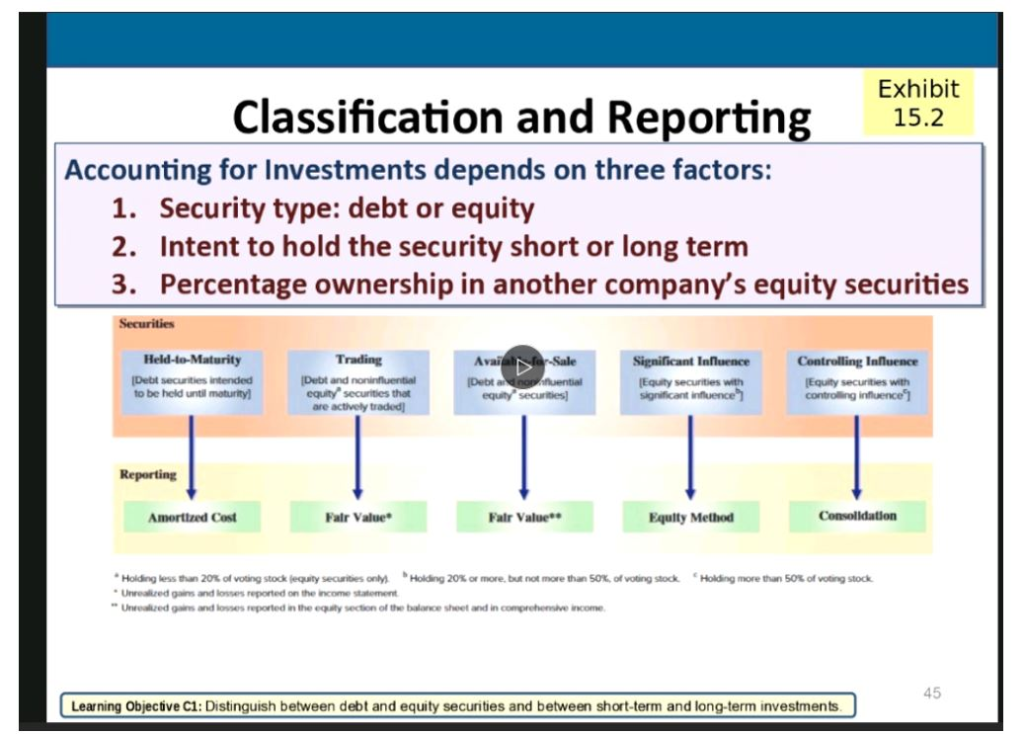

Accounting Summary for Investments in Securities Exhibit 15.8 Classification Accounting Cost (without any discount or premium amortization) Fair value (with fair value adjustment to income) Fair value (with fair value adjustment to equity) Short-Term Investment in Securities Held-to-maturity (debt) securities ....... Trading (debt and equity) securities ...... Available-for-sale (debt and equity) securities ....... Long-Term Investment in Securities Held-to-maturity (debt) securities ........ Available-for-sale (debt and equity) securities ....... Equity securities with significant influence ......... Equity securities with controlling influence ......... Cost (with any discount or premium amortization) Fair value (with fair value adjustment to equity) Equity method Equity method (with consolidation) Exhibit 15.8 on page 634 65 Learning Objective C2: Describe how to report equity securities with controlling influence. Exhibit Classification and Reporting 15.2 Accounting for Investments depends on three factors: 1. Security type: debt or equity 2. Intent to hold the security short or long term 3. Percentage ownership in another company's equity securities Securities Held-to-Maturity Debt securities intended to be held until maturity Trading Debt and noninfluential equity securities that are actively traded] Availe-Sale Debtor fuential equity securities Significant Influence Equity securities with significant influence Controlling Influence Equity securities with controlling influence 11111 Reporting Amortized Cost Fair Value Fair Value Equity Method Consolidation Holding more than 50% of voting stock Holding less than 20% of voting stock jequity securities only H olding 20% or more, but not more than 50% of voting stock Unreleed gains and losses reported on the income statement Unvered and lowes reported in the equity section of the balance sheet and incomprehensive income Learning Objective C1: Distinguish between debt and equity securities and between short-term and long-term investments Accounting Summary for Investments in Securities Exhibit 15.8 Classification Accounting Cost (without any discount or premium amortization) Fair value (with fair value adjustment to income) Fair value (with fair value adjustment to equity) Short-Term Investment in Securities Held-to-maturity (debt) securities ....... Trading (debt and equity) securities ...... Available-for-sale (debt and equity) securities ....... Long-Term Investment in Securities Held-to-maturity (debt) securities ........ Available-for-sale (debt and equity) securities ....... Equity securities with significant influence ......... Equity securities with controlling influence ......... Cost (with any discount or premium amortization) Fair value (with fair value adjustment to equity) Equity method Equity method (with consolidation) Exhibit 15.8 on page 634 65 Learning Objective C2: Describe how to report equity securities with controlling influence. Exhibit Classification and Reporting 15.2 Accounting for Investments depends on three factors: 1. Security type: debt or equity 2. Intent to hold the security short or long term 3. Percentage ownership in another company's equity securities Securities Held-to-Maturity Debt securities intended to be held until maturity Trading Debt and noninfluential equity securities that are actively traded] Availe-Sale Debtor fuential equity securities Significant Influence Equity securities with significant influence Controlling Influence Equity securities with controlling influence 11111 Reporting Amortized Cost Fair Value Fair Value Equity Method Consolidation Holding more than 50% of voting stock Holding less than 20% of voting stock jequity securities only H olding 20% or more, but not more than 50% of voting stock Unreleed gains and losses reported on the income statement Unvered and lowes reported in the equity section of the balance sheet and incomprehensive income Learning Objective C1: Distinguish between debt and equity securities and between short-term and long-term investments