Question

Part 4 - Make the necessary adjusting entries to record the following information available at the end of the fiscal period. Please remember that the

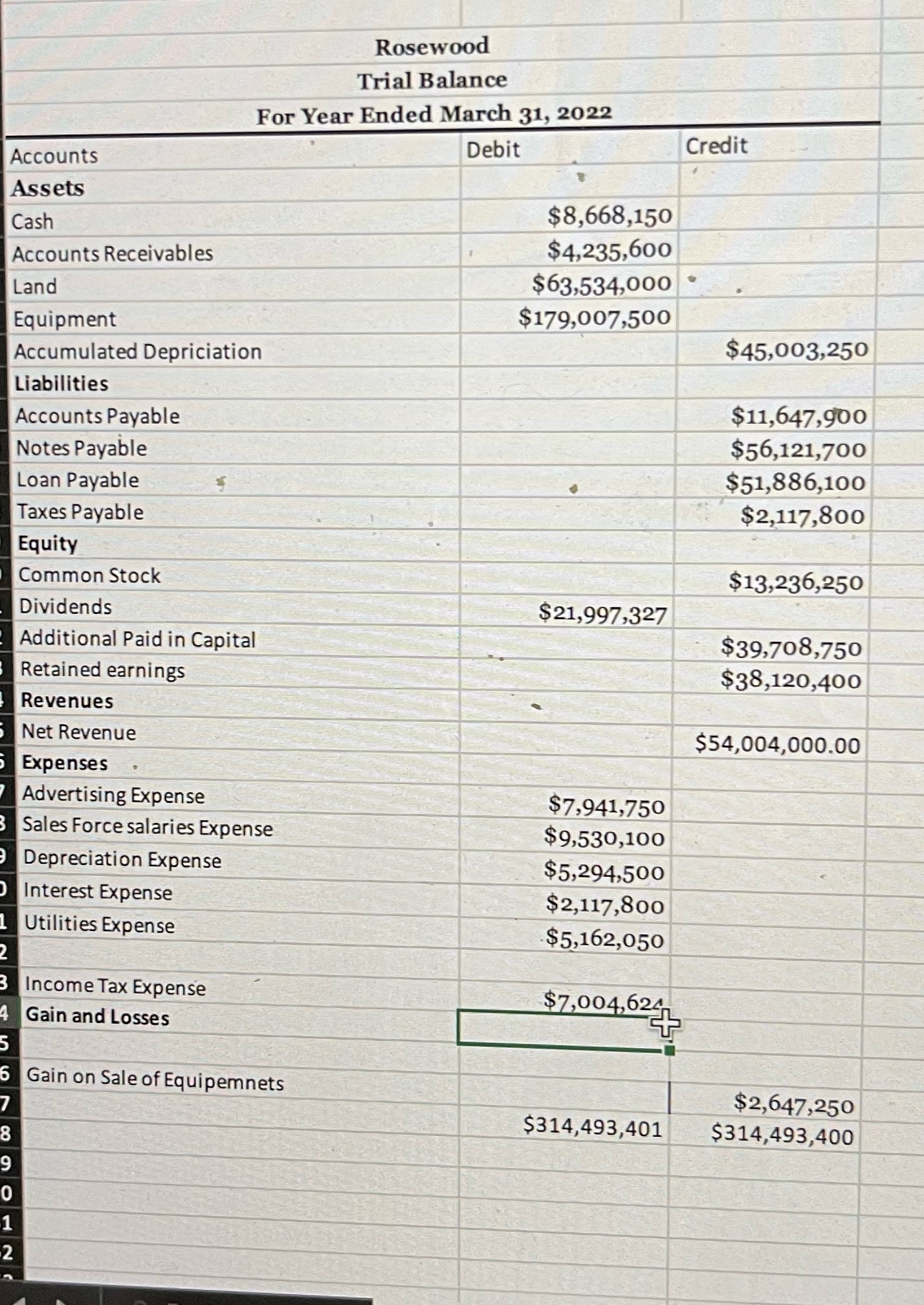

"Part 4 - Make the necessary adjusting entries to record the following information available at the end of the fiscal period. Please remember that the description accompanying adjusting entries should include sufficient detail that your calculation can be checked by the auditor and duplicated next month. This means that your description should include the actual equation you used to come up with the value used in your journal entry.In making your entries, use ONLY existing accounts. You can see all of the company's existing accounts in the ledger in Part 2. As with the original entries, only the entries that appear in the box below will be graded." No depreciation has been recorded on the company's Land or new PPE. Rosewood's accounting staff believes that the Land has a useful life of 30 years with a $5,718,060 salvage value. They also believe that the new PPE has a remaining useful life of 18 years with a $891,064 salvage value. When calculating depreciation, keep in mind that Rosewood does not use partial year depreciation. They record a full year of depreciation, regardless of when an asset was purchased. HINT: New PPE is the amount added this year, and is shown as the debit below the beginning balance of the Equipment account! Rosewood recorded and paid interest on all of their outstanding notes 2 months ago. Payments are due on the notes every 6 months, and the interest rate on both notes is 4.5% (they were issued by the same bank with the same terms, just 2 years apart). Unlike the federal government, the state where Rosewood does business charges property taxes instead of an income tax. These taxes are charged on an assessed market value assigned by the government for tax purposes; the assessed value does not match what Rosewood actually paid for the assets. In fact, the assessed value comes out to 51% of the book value (historical costs - accumulated deprecation, if any) of the company's land owned at the end of the fiscal year. The property tax rate for 2022 is 5%. The taxes will be paid when they are due on May 1, 2022

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modern Advanced Accounting In Canada

Authors: Murray Hilton

6th Edition

0070001537, 978-0070001534