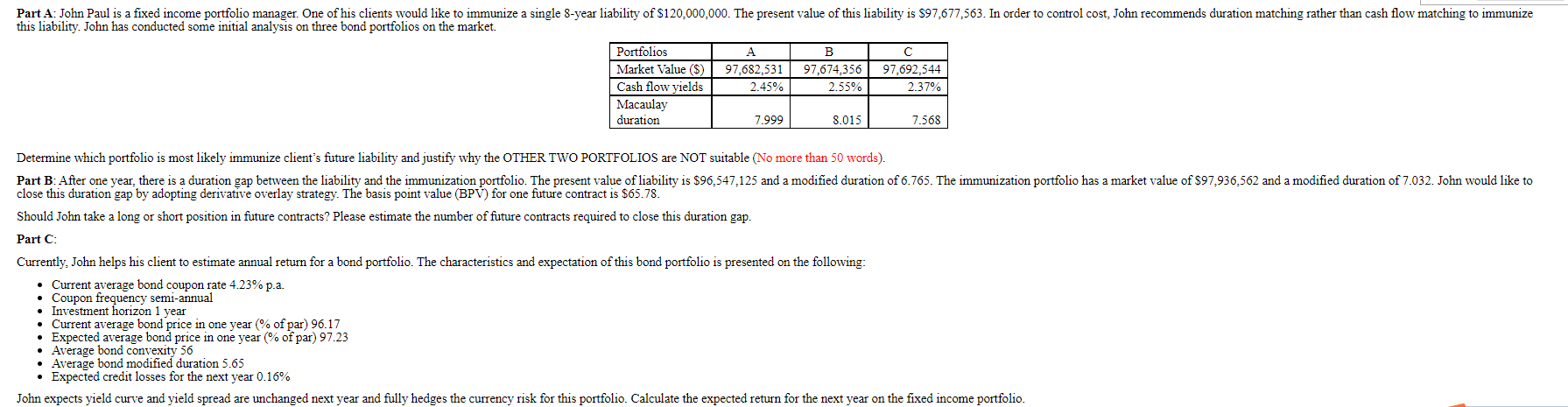

Part A: John Paul is a fixed income portfolio manager. One of his clients would like to immunize a single 8-year liability of $120,000,000. The present value of this liability is $97,677,563. In order to control cost, John recommends duration matching rather than cash flow matching to immunize this liability. John has conducted some initial analysis on three bond portfolios on the market. C Portfolios Market Value ($) Cash flow yields Macaulay duration A 97,682,531 2.45% B 97,674.356 2.55% 97.692,544 2.37% 7.999 8.015 7.568 Determine which portfolio is most likely immunize client's future liability and justify why the OTHER TWO PORTFOLIOS are NOT suitable (No more than 50 words). Part B: After one year, there is a duration gap between the liability and the immunization portfolio. The present value of liability is $96,547,125 and a modified duration of 6.765. The immunization portfolio has a market value of $97.936.562 and a modified duration of 7.032. John would like to close this duration gap by adopting derivative overlay strategy. The basis point value (BPV) for one future contract is $65.78. Should John take a long or short position in future contracts? Please estimate the number of future contracts required to close this duration gap. Part C: Currently, John helps his client to estimate annual return for a bond portfolio. The characteristics and expectation of this bond portfolio is presented on the following: Current average bond coupon rate 4.23% p.a. Coupon frequency semi-annual Investment horizon 1 year Current average bond price in one year of par) 96.17 Expected average bond price in one year % of par) 97.23 Average bond convexity 56 Average bond modified duration 5.65 Expected credit losses for the next year 0.16% John expects yield curve and yield spread are unchanged next year and fully hedges the currency risk for this portfolio. Calculate the expected return for the next year on the fixed income portfolio. Part A: John Paul is a fixed income portfolio manager. One of his clients would like to immunize a single 8-year liability of $120,000,000. The present value of this liability is $97,677,563. In order to control cost, John recommends duration matching rather than cash flow matching to immunize this liability. John has conducted some initial analysis on three bond portfolios on the market. C Portfolios Market Value ($) Cash flow yields Macaulay duration A 97,682,531 2.45% B 97,674.356 2.55% 97.692,544 2.37% 7.999 8.015 7.568 Determine which portfolio is most likely immunize client's future liability and justify why the OTHER TWO PORTFOLIOS are NOT suitable (No more than 50 words). Part B: After one year, there is a duration gap between the liability and the immunization portfolio. The present value of liability is $96,547,125 and a modified duration of 6.765. The immunization portfolio has a market value of $97.936.562 and a modified duration of 7.032. John would like to close this duration gap by adopting derivative overlay strategy. The basis point value (BPV) for one future contract is $65.78. Should John take a long or short position in future contracts? Please estimate the number of future contracts required to close this duration gap. Part C: Currently, John helps his client to estimate annual return for a bond portfolio. The characteristics and expectation of this bond portfolio is presented on the following: Current average bond coupon rate 4.23% p.a. Coupon frequency semi-annual Investment horizon 1 year Current average bond price in one year of par) 96.17 Expected average bond price in one year % of par) 97.23 Average bond convexity 56 Average bond modified duration 5.65 Expected credit losses for the next year 0.16% John expects yield curve and yield spread are unchanged next year and fully hedges the currency risk for this portfolio. Calculate the expected return for the next year on the fixed income portfolio