Answered step by step

Verified Expert Solution

Question

1 Approved Answer

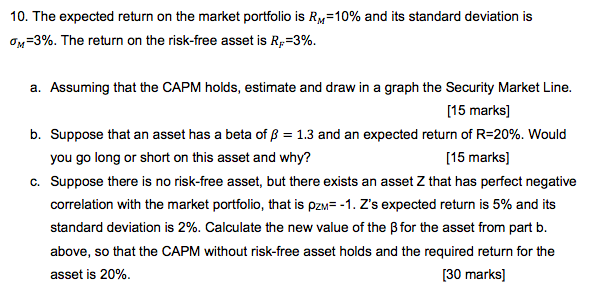

PART B and C 10. The expected return on the market portfolio is Ry=10% and its standard deviation is Ox=3%. The return on the risk-free

PART B and C

10. The expected return on the market portfolio is Ry=10% and its standard deviation is Ox=3%. The return on the risk-free asset is R2=3%. a. Assuming that the CAPM holds, estimate and draw in a graph the Security Market Line. [15 marks) b. Suppose that an asset has a beta of B = 1.3 and an expected return of R=20%. Would you go long or short on this asset and why? [15 marks] C. Suppose there is no risk-free asset, but there exists an asset Z that has perfect negative correlation with the market portfolio, that is pzm=-1. Z's expected return is 5% and its standard deviation is 2%. Calculate the new value of the Bfor the asset from part b. above, so that the CAPM without risk-free asset holds and the required return for the asset is 20% [30 marks]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Military Spouse Finance Guide Financial Advice For The Homefront

Authors: Pioneer Services

1st Edition

0595477771, 9780595477777