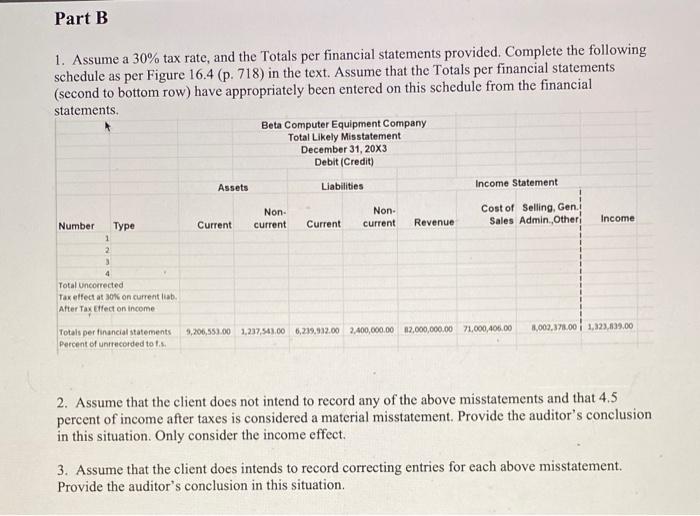

1. Assume a 30% tax rate, and the Totals per financial statements provided. Complete the following schedule as per Figure 16.4 (p. 718) in the text. Assume that the Totals per financial statements (second to bottom row) have appropriately been entered on this schedule from the financial statements. 2. Assume that the client does not intend to record any of the above misstatements and that 4.5 percent of income after taxes is considered a material misstatement. Provide the auditor's conclusion in this situation. Only consider the income effect. 3. Assume that the client does intends to record correcting entries for each above misstatement. Provide the auditor's conclusion in this situation. On February 20, 20X4 you are well into the field work of the 12/31/20X3 audit and the following issues have arisen during the audit of Beta Computer Equipment Company (BCE.) 1. Service revenue 2. Account receivable from officers 3. Prepaid advertising 4. Alan Almond Company receivable Linda Wilson the president of BCE wants you to present your position on each of these issues as she would like your judgment as to "good GAAP" numbers. But, she has also pointed out that she understands that GAAP often does not provide a precise answer, and in such cases, she would rather error on the side of maintaining income rather than being "an overly pessimistic doomsayer." The attitude of Board of Directors members is consistent with that of Linda. Prepare a memo that summarizes relevant professional standards (standard and paragraph should be cited) related to each of the 4 issues and prepare any proposed journal entries. Discuss information that would be included in any note disclosures related to each of the four items (you need not draft formal note disclosures). Prepare entries for all misstatements you identify, regardless of the amount involved. That is, don't simply say no entry is needed because any amount involved would be immaterial. Assume that the current income is $1,323,839. For purposes of preparing journal entries, you may ignore income tax implications as any changes in taxes will be reflected later in the audit process after any entries have been posted to the working trial balance. Summarize the income effects (before taxes) of any entries that you propose on a schedule such as the following (make clear over and understatements of income) : Income Effect 1. Uneamed service revenue Issue 1: Service Revenue BCE has included service revenue of $22,100 as a result of a number of one year service policies sold late in December as an "experiment." These service policies became effective on January 1 , 20X, or shortly thereafter. The policies are sold at an average of $600 per year per customer; the $22,100 represents the total cash received as of year-end (debit cash, credit service revenue). The $600 per customer amount was arrived at by an analysis of previous service provided on a "fee for service" basis to customers. The average cost to BCE was approximately $200 per visit, with an average of 1.7 visits per year to customers. While the service policies allow unlimited visits for service, BCE has restricted the number of policies available due to difficulties in calculating the costs associated with such policies. BCE estimates that the number service calls is likely to increase to about 4 per year; the cost is expected to decrease to around $150 per call. So, at this point, the program is projected to break even. The aggressive pricing of the service policies is due to (1) the experimental nature of the program and (2) a desire to maintain long-tegm customer loyalty for future purchases of equipment. What entry or disclosure, if any, is necessary in this circumstance? Issue 2: Accounts Receivable From Officers At year-end BCE has $110,000 in accounts receivables from officers on the books. The Board of Directors approved these loans which are in the form of "demand" notes. One of the staff assistants asked whether there was any intent to require officers to pay back these loans. Linda Wilson and Jan Wiggs, who each owe 1/2 of the total amount outstanding, agreed that while not much thought had been given to it, they imagined that they might someday repay the loans. On the other hand, they thought that the Board of Directors might forgive the loans some year in lieu of their annual bonus. What entry or disclosure, if any, is necessary in this circumstance? Issue 3: Prepaid Advertising On November 1, 20X3 BCE paid $30,000 in advance for eight months of advertising on radio station KNEWZ, a local news station. The entry was recorded with a debit to prepaid advertising and a credit to cash. At December 31, 20X3 BCE expensed \$7,500 (debit to advertising expense and credit to prepaid advertising for 2 of the 8 months). Earlier, on December 29, 20X3 BCE received a letter from KNEWZ indicating that the radio station was changing its format on January 1,20X4 to "classic heavy metal." In brief, news is being replaced by old songs of Phish, Ozzie Osboume, and Metallica. It will now use the call letters KDEV. Although BCE has no real data on this, it is management's impression that most Ozzie Osbourne fans buy fewer networked computer systems than news station listeners. Accordingly, management attempted to cancel the agreement and receive a refund. Regrettably, the contract for the advertising provides no assurances about a change in station format and BCE's lawyers say that obtaining any recovery in a court proceeding is doubtful. KDEV has refused any attempts at renegotiation and has suggested that BCE might be surprised at the number of customers that might respond to the commercials. KDEV is even willing to wor: with BCE to redo commercials eliminating the old ones that used the "sappy sounding" news announcers and replacing them with commercials using their new announcers; KDEV is willing to record these commercials for no additional cost. BCE management still questions whether the advertising will be well placed, but does believe that there may be a few listeners who might respond to the advertisement. BCE legal counsel suggests that it is not worth pursuing this matter further. What entry or disclosure, if any, is necessary in this circumstance? Issue 4: Alan Almond Recelvable Alan Almond Company (Alan Almond) owes BCE \$82,000 for a computer system installation that was purchased in March of 203. Alan Almond has run into financial difficulties due to dramatic decreases in the selling price of almonds during recent years. In August of 20X3 Linda Wilson (BCE president) and Jan Wiggs (BCE controller) established a repayment schedule in which Alan Almond Your discussion with management indicates that Alan Almond received a "going concern" modification from its auditors for the year ended 8/30/X3 (the audit report was dated 10/22/X3 ). The going concern modification arose due to a question concerning whether Alan Almond can obtain new financing when needed, on June 30,20X4. However, the situation is not entirely bleak for Alan Almond's future as layoffs of 1/3 of the company's employees resulted in a situation in which Alan Almond operated at break even for the year ended 8/30X3. Alan Almond has discussed filing for bankruptcy with bankruptcy legal counsel and at this point believes it is unnecessary. But, if it becomes necessary, counsel suggests that creditors shouldn't expect to receive more than 50 cents on the dollar. Management has suggested to you that 70 cents on the dollar is more likely if bankruptcy ensues. Your analysis at the date of both the Alan Almond audited annual statements (8/30/X3) and the interim statements (11/30/X3) indicates that if bankruptcy is declared, a recovery of 5060 cents on the dollar (with no amount more probable than another in that range) is likely. Yet, it's difficult to know what the situation will be in the future. BCE Accounting Issues Case, Page 3 Copyright Q2022 McGraw Hill. All rights reserved. No reproduction or distribution without the prior written consent of MoGraw Hill. The sales agreement for the computer system allows BCE to repossess the equipment at any time prior to bankruptcy. But, because the equipment is used and specific to Alan Almond's applications, management believes that the equipment could be sold for a (net) of between $20,000 and $30,000. Also, management points out that such an action would not be considered positively by either Alan Almond or a number of other companies that BCE is attempting to attract as clients. Accordingly, BCE has resisted this option and does not intend to pursue it at this time. Your analysis of the interim statements (unaudited) reveals that Alan Almond operated at a slight prior to bankruptcy. But, because the equipment is used and specitic to Alan Almond's applications, management believes that the equipment could be sold for a (net) of between $20,000 and $30,000. Also, management points out that such an action would not be considered positively by either Alan Almond or a number of other companies that BCE is attempting to attract as clients. Accordingly, BCE has resisted this option and does not intend to pursue it at this time. Your analysis of the interim statements (unaudited) reveals that Alan Almond operated at a slight profit during the first quarter and that almond prices have increased approximately 15 percent. However, experts disagree widely as to future almond prices as there is some concern that a significant increase in almonds from India may enter the US market. Finally, Alan Almond's management, although noncommittal on details, suggests that it believes that it will be able to continue repayments on the debt within the "next few months." But your feeling is that it is probable that Alan Almond will be forced to file for bankruptcy. No allowance for this account is currently included in the allowance for doubtful accounts. What, if any, loss reserve (and/or note disclosure) should be reflected in the financial statements