Part B Recommendations (60 marks) Prepare a report explaining and making recommendations on the financial reporting issues below. a) The impact of change to preparing consolidated financial statements on Antara Ltds disclosure of financial information. (40 marks) Your response should include: The differences between applying the equity method of accounting in Antara Ltds own accounting records, and applying the equity method of accounting in Antara Ltds consolidation worksheet. The content of Antara Ltds relevant financial statement. The extent of financial information available to Antara Ltds external users. References to the financial information in Part A and relevant accounting standards. b) Potential dividends paid by Blanca Ltd. This is because Blanca Ltd has been profitable and the company management plans to pay dividends to Antara Ltd. (20 marks) Your response should include: How dividends paid by Blanca Ltd are accounted for using the equity method of accounting. How dividends are disclosed in Antara Ltds relevant financial statement.

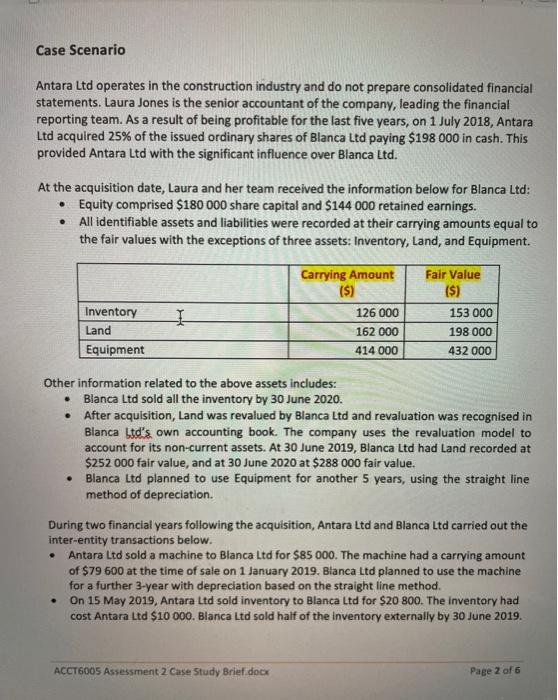

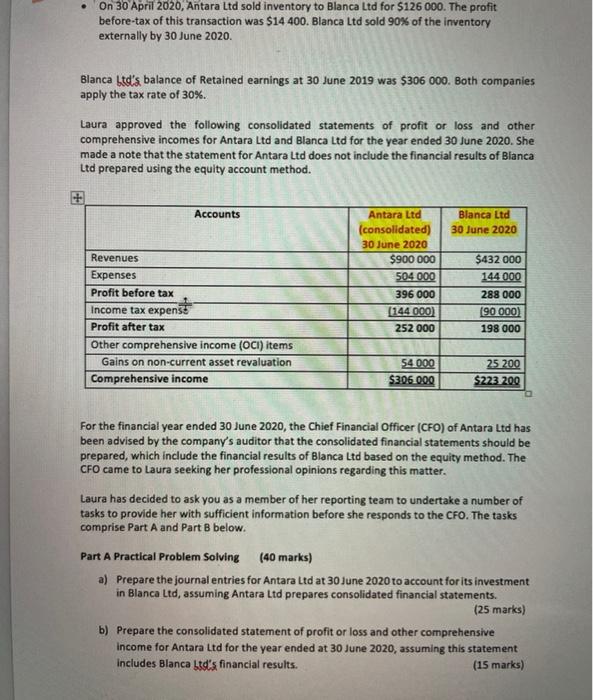

Case Scenario Antara Ltd operates in the construction industry and do not prepare consolidated financial statements. Laura Jones is the senior accountant of the company, leading the financial reporting team. As a result of being profitable for the last five years, on 1 July 2018, Antara Ltd acquired 25% of the issued ordinary shares of Blanca Ltd paying $198 000 in cash. This provided Antara Ltd with the significant influence over Blanca Ltd. At the acquisition date, Laura and her team received the information below for Blanca Ltd: Equity comprised $180 000 share capital and $144 000 retained earnings. All identifiable assets and liabilities were recorded at their carrying amounts equal to the fair values with the exceptions of three assets: Inventory, Land, and Equipment. Carrying Amount ($) Fair Value ($) 1 Inventory Land Equipment 126 000 162 000 414 000 153 000 198 000 432 000 Other information related to the above assets includes: Blanca Ltd sold all the inventory by 30 June 2020. After acquisition, Land was revalued by Blanca Ltd and revaluation was recognised in Blanca Lid's own accounting book. The company uses the revaluation model to account for its non-current assets. At 30 June 2019, Blanca Ltd had Land recorded at $252 000 fair value, and at 30 June 2020 at $288 000 fair value. Blanca Ltd planned to use Equipment for another 5 years, using the straight line method of depreciation. During two financial years following the acquisition, Antara Ltd and Blanca Ltd carried out the inter-entity transactions below. . Antara Ltd sold a machine to Blanca Ltd for $85 000. The machine had a carrying amount of $79 600 at the time of sale on 1 January 2019. Blanca Ltd planned to use the machine for a further 3-year with depreciation based on the straight line method. On 15 May 2019. Antara Ltd sold inventory to Blanca Ltd for $20 800. The inventory had cost Antara Ltd $10 000. Blanca Ltd sold half of the inventory externally by 30 June 2019. ACCT6005 Assessment 2 Case Study Brief.docx Page 2 of 6 On 30 April 2020, Antara Ltd sold inventory to Blanca Ltd for $126 000. The profit before-tax of this transaction was $14 400. Blanca Ltd sold 90% of the inventory externally by 30 June 2020. Blanca Ltd's balance of Retained earnings at 30 June 2019 was $306 000. Both companies apply the tax rate of 30%. Laura approved the following consolidated statements of profit or loss and other comprehensive incomes for Antara Ltd and Blanca Ltd for the year ended 30 June 2020. She made a note that the statement for Antara Ltd does not include the financial results of Blanca Ltd prepared using the equity account method. + Accounts Blanca Ltd 30 June 2020 Revenues Expenses Profit before tax Income tax expenst Profit after tax Other comprehensive income (OCI) items Gains on non-current asset revaluation Comprehensive income Antara Ltd (consolidated) 30 June 2020 $900 000 504 000 396 000 (144 000 252 000 $432 000 144 000 288 000 190.000) 198 000 54000 $306 000 25 200 $223 200 For the financial year ended 30 June 2020, the Chief Financial Officer (CFO) of Antara Ltd has been advised by the company's auditor that the consolidated financial statements should be prepared, which include the financial results of Blanca Ltd based on the equity method. The CFO came to Laura seeking her professional opinions regarding this matter. Laura has decided to ask you as a member of her reporting team to undertake a number of tasks to provide her with sufficient information before she responds to the CFO. The tasks comprise Part A and Part B below. Part A Practical Problem Solving (40 marks) a) Prepare the journal entries for Antara Ltd at 30 June 2020 to account for its investment in Blanca Ltd, assuming Antara Ltd prepares consolidated financial statements. (25 marks) b) Prepare the consolidated statement of profit or loss and other comprehensive income for Antara Ltd for the year ended at 30 June 2020, assuming this statement includes Blanca Lid's financial results. (15 marks) Part B Recommendations (60 marks) Prepare a report explaining and making recommendations on the financial reporting issues below. a) The impact of change to preparing consolidated financial statements on Antara Ltd's. disclosure of financial information. (40 marks) Your response should include: The differences between applying the equity method of accounting in Antara Ltd's own accounting records, and applying the equity method of accounting in Antara Ltd's consolidation worksheet. The content of Antara Ltd's relevant financial statement. The extent of financial information available to Antara Ltd's external users. References to the financial information in Part A and relevant accounting standards. b) Potential dividends paid by Blanca Ltd. This is because Blanca Ltd has been profitable and the company management plans to pay dividends to Antara Ltd. (20 marks) Your response should include: How dividends paid by Blanca Ltd are accounted for using the equity method of accounting How dividends are disclosed in Antara Ltd's relevant financial statement. References to the financial information in Part A and relevant accounting standards. . Case Scenario Antara Ltd operates in the construction industry and do not prepare consolidated financial statements. Laura Jones is the senior accountant of the company, leading the financial reporting team. As a result of being profitable for the last five years, on 1 July 2018, Antara Ltd acquired 25% of the issued ordinary shares of Blanca Ltd paying $198 000 in cash. This provided Antara Ltd with the significant influence over Blanca Ltd. At the acquisition date, Laura and her team received the information below for Blanca Ltd: Equity comprised $180 000 share capital and $144 000 retained earnings. All identifiable assets and liabilities were recorded at their carrying amounts equal to the fair values with the exceptions of three assets: Inventory, Land, and Equipment. Carrying Amount ($) Fair Value ($) 1 Inventory Land Equipment 126 000 162 000 414 000 153 000 198 000 432 000 Other information related to the above assets includes: Blanca Ltd sold all the inventory by 30 June 2020. After acquisition, Land was revalued by Blanca Ltd and revaluation was recognised in Blanca Lid's own accounting book. The company uses the revaluation model to account for its non-current assets. At 30 June 2019, Blanca Ltd had Land recorded at $252 000 fair value, and at 30 June 2020 at $288 000 fair value. Blanca Ltd planned to use Equipment for another 5 years, using the straight line method of depreciation. During two financial years following the acquisition, Antara Ltd and Blanca Ltd carried out the inter-entity transactions below. . Antara Ltd sold a machine to Blanca Ltd for $85 000. The machine had a carrying amount of $79 600 at the time of sale on 1 January 2019. Blanca Ltd planned to use the machine for a further 3-year with depreciation based on the straight line method. On 15 May 2019. Antara Ltd sold inventory to Blanca Ltd for $20 800. The inventory had cost Antara Ltd $10 000. Blanca Ltd sold half of the inventory externally by 30 June 2019. ACCT6005 Assessment 2 Case Study Brief.docx Page 2 of 6 On 30 April 2020, Antara Ltd sold inventory to Blanca Ltd for $126 000. The profit before-tax of this transaction was $14 400. Blanca Ltd sold 90% of the inventory externally by 30 June 2020. Blanca Ltd's balance of Retained earnings at 30 June 2019 was $306 000. Both companies apply the tax rate of 30%. Laura approved the following consolidated statements of profit or loss and other comprehensive incomes for Antara Ltd and Blanca Ltd for the year ended 30 June 2020. She made a note that the statement for Antara Ltd does not include the financial results of Blanca Ltd prepared using the equity account method. + Accounts Blanca Ltd 30 June 2020 Revenues Expenses Profit before tax Income tax expenst Profit after tax Other comprehensive income (OCI) items Gains on non-current asset revaluation Comprehensive income Antara Ltd (consolidated) 30 June 2020 $900 000 504 000 396 000 (144 000 252 000 $432 000 144 000 288 000 190.000) 198 000 54000 $306 000 25 200 $223 200 For the financial year ended 30 June 2020, the Chief Financial Officer (CFO) of Antara Ltd has been advised by the company's auditor that the consolidated financial statements should be prepared, which include the financial results of Blanca Ltd based on the equity method. The CFO came to Laura seeking her professional opinions regarding this matter. Laura has decided to ask you as a member of her reporting team to undertake a number of tasks to provide her with sufficient information before she responds to the CFO. The tasks comprise Part A and Part B below. Part A Practical Problem Solving (40 marks) a) Prepare the journal entries for Antara Ltd at 30 June 2020 to account for its investment in Blanca Ltd, assuming Antara Ltd prepares consolidated financial statements. (25 marks) b) Prepare the consolidated statement of profit or loss and other comprehensive income for Antara Ltd for the year ended at 30 June 2020, assuming this statement includes Blanca Lid's financial results. (15 marks) Part B Recommendations (60 marks) Prepare a report explaining and making recommendations on the financial reporting issues below. a) The impact of change to preparing consolidated financial statements on Antara Ltd's. disclosure of financial information. (40 marks) Your response should include: The differences between applying the equity method of accounting in Antara Ltd's own accounting records, and applying the equity method of accounting in Antara Ltd's consolidation worksheet. The content of Antara Ltd's relevant financial statement. The extent of financial information available to Antara Ltd's external users. References to the financial information in Part A and relevant accounting standards. b) Potential dividends paid by Blanca Ltd. This is because Blanca Ltd has been profitable and the company management plans to pay dividends to Antara Ltd. (20 marks) Your response should include: How dividends paid by Blanca Ltd are accounted for using the equity method of accounting How dividends are disclosed in Antara Ltd's relevant financial statement. References to the financial information in Part A and relevant accounting standards