Answered step by step

Verified Expert Solution

Question

1 Approved Answer

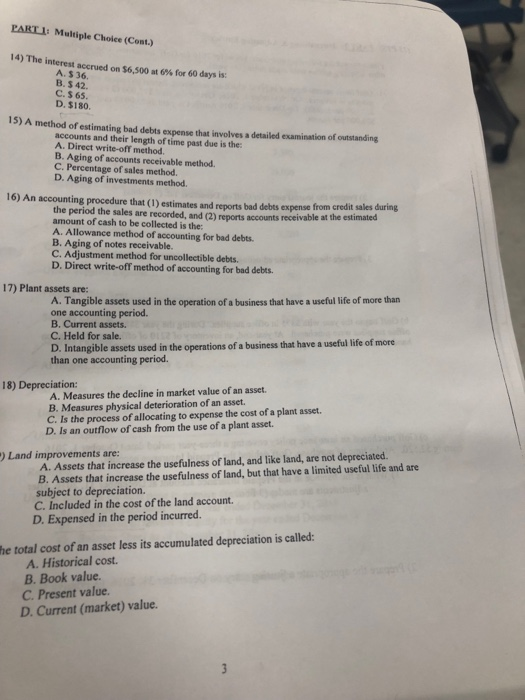

PART I: Multiple Choice (Cont.) 14) The interest accrued on S6.500 at 6% for 60 days is: A. $ 36 B. $ 42. C. $

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cognitive Hack The New Battleground In Cybersecurity The Human Mind Internal Audit And IT Audit

Authors: James Bone

1st Edition

0367567962, 978-0367567965