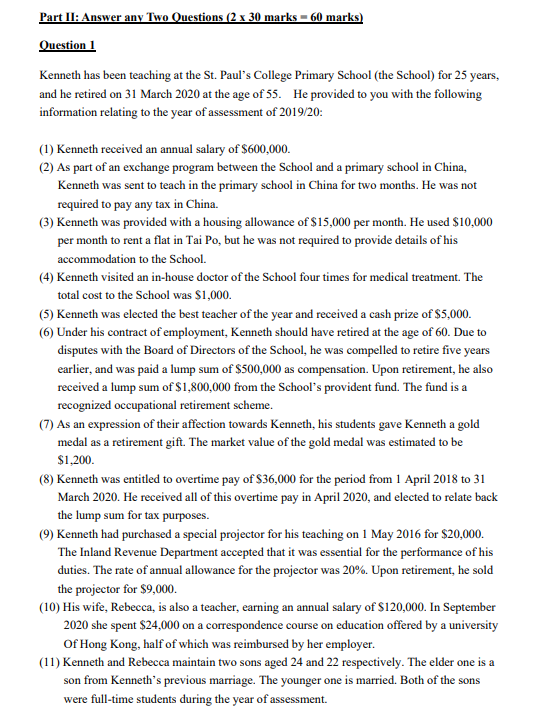

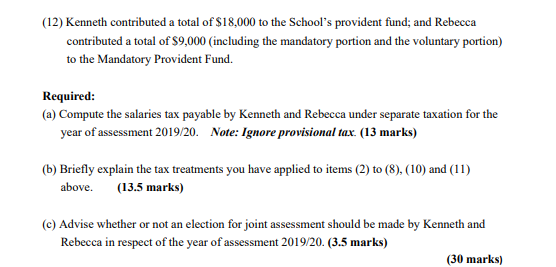

Part II: Answer any Two Questions (2 x 30 marks = 60 marks) Question 1 Kenneth has been teaching at the St. Paul's College Primary School (the School) for 25 years, and he retired on 31 March 2020 at the age of 55. He provided to you with the following information relating to the year of assessment of 2019/20 (1) Kenneth received an annual salary of $600,000. (2) As part of an exchange program between the School and a primary school in China, Kenneth was sent to teach in the primary school in China for two months. He was not required to pay any tax in China. (3) Kenneth was provided with a housing allowance of $15,000 per month. He used $10,000 per month to rent a flat in Tai Po, but he was not required to provide details of his accommodation to the School. (4) Kenneth visited an in-house doctor of the School four times for medical treatment. The total cost to the School was $1,000. (5) Kenneth was elected the best teacher of the year and received a cash prize of $5,000. (6) Under his contract of employment, Kenneth should have retired at the age of 60. Due to disputes with the Board of Directors of the School, he was compelled to retire five years earlier, and was paid a lump sum of $500,000 as compensation. Upon retirement, he also received a lump sum of $1,800,000 from the School's provident fund. The fund is a recognized occupational retirement scheme. (7) As an expression of their affection towards Kenneth, his students gave Kenneth a gold medal as a retirement gift. The market value of the gold medal was estimated to be $1,200. (8) Kenneth was entitled to overtime pay of $36,000 for the period from 1 April 2018 to 31 March 2020. He received all of this overtime pay in April 2020, and elected to relate back the lump sum for tax purposes. (9) Kenneth had purchased a special projector for his teaching on 1 May 2016 for $20,000. The Inland Revenue Department accepted that it was essential for the performance of his duties. The rate of annual allowance for the projector was 20%. Upon retirement, he sold the projector for $9,000. (10) His wife, Rebecca, is also a teacher, earning an annual salary of $120,000. In September 2020 she spent $24,000 on a correspondence course on education offered by a university Of Hong Kong, half of which was reimbursed by her employer. (11) Kenneth and Rebecca maintain two sons aged 24 and 22 respectively. The elder one is a son from Kenneth's previous marriage. The younger one is married. Both of the sons were full-time students during the year of assessment. (12) Kenneth contributed a total of $18,000 to the School's provident fund; and Rebecca contributed a total of $9,000 (including the mandatory portion and the voluntary portion) to the Mandatory Provident Fund. Required: (a) Compute the salaries tax payable by Kenneth and Rebecca under separate taxation for the year of assessment 2019/20. Note: Ignore provisional tax (13 marks) (b) Briefly explain the tax treatments you have applied to items (2) to (8), (10) and (11) above. (13.5 marks) (c) Advise whether or not an election for joint assessment should be made by Kenneth and Rebecca in respect of the year of assessment 2019/20 (3.5 marks) (30 marks) Part II: Answer any Two Questions (2 x 30 marks = 60 marks) Question 1 Kenneth has been teaching at the St. Paul's College Primary School (the School) for 25 years, and he retired on 31 March 2020 at the age of 55. He provided to you with the following information relating to the year of assessment of 2019/20 (1) Kenneth received an annual salary of $600,000. (2) As part of an exchange program between the School and a primary school in China, Kenneth was sent to teach in the primary school in China for two months. He was not required to pay any tax in China. (3) Kenneth was provided with a housing allowance of $15,000 per month. He used $10,000 per month to rent a flat in Tai Po, but he was not required to provide details of his accommodation to the School. (4) Kenneth visited an in-house doctor of the School four times for medical treatment. The total cost to the School was $1,000. (5) Kenneth was elected the best teacher of the year and received a cash prize of $5,000. (6) Under his contract of employment, Kenneth should have retired at the age of 60. Due to disputes with the Board of Directors of the School, he was compelled to retire five years earlier, and was paid a lump sum of $500,000 as compensation. Upon retirement, he also received a lump sum of $1,800,000 from the School's provident fund. The fund is a recognized occupational retirement scheme. (7) As an expression of their affection towards Kenneth, his students gave Kenneth a gold medal as a retirement gift. The market value of the gold medal was estimated to be $1,200. (8) Kenneth was entitled to overtime pay of $36,000 for the period from 1 April 2018 to 31 March 2020. He received all of this overtime pay in April 2020, and elected to relate back the lump sum for tax purposes. (9) Kenneth had purchased a special projector for his teaching on 1 May 2016 for $20,000. The Inland Revenue Department accepted that it was essential for the performance of his duties. The rate of annual allowance for the projector was 20%. Upon retirement, he sold the projector for $9,000. (10) His wife, Rebecca, is also a teacher, earning an annual salary of $120,000. In September 2020 she spent $24,000 on a correspondence course on education offered by a university Of Hong Kong, half of which was reimbursed by her employer. (11) Kenneth and Rebecca maintain two sons aged 24 and 22 respectively. The elder one is a son from Kenneth's previous marriage. The younger one is married. Both of the sons were full-time students during the year of assessment. (12) Kenneth contributed a total of $18,000 to the School's provident fund; and Rebecca contributed a total of $9,000 (including the mandatory portion and the voluntary portion) to the Mandatory Provident Fund. Required: (a) Compute the salaries tax payable by Kenneth and Rebecca under separate taxation for the year of assessment 2019/20. Note: Ignore provisional tax (13 marks) (b) Briefly explain the tax treatments you have applied to items (2) to (8), (10) and (11) above. (13.5 marks) (c) Advise whether or not an election for joint assessment should be made by Kenneth and Rebecca in respect of the year of assessment 2019/20 (3.5 marks) (30 marks)