Answered step by step

Verified Expert Solution

Question

1 Approved Answer

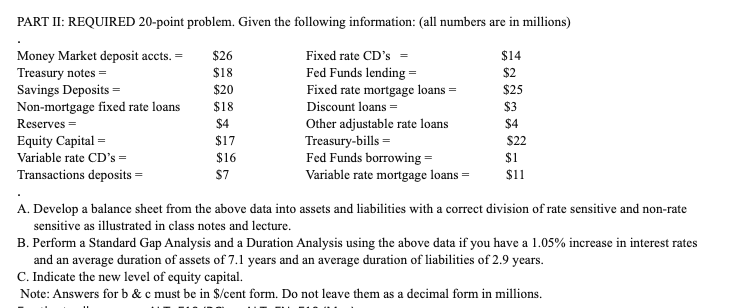

PART II: REQUIRED 20-point problem. Given the following information: (all numbers are in millions) $26 $18 Money Market deposit acets. = Treasury notes = Savings

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Board Of Directors And Audit Committee Guide To Fiduciary Responsibilities Ten Critical Steps To Protecting Yourself And Your Organization

Authors: Sheila Moran CPA CFE, Ronald Kral CPA CMA

1st Edition

0814431666, 978-0814431665