Performance evaluation

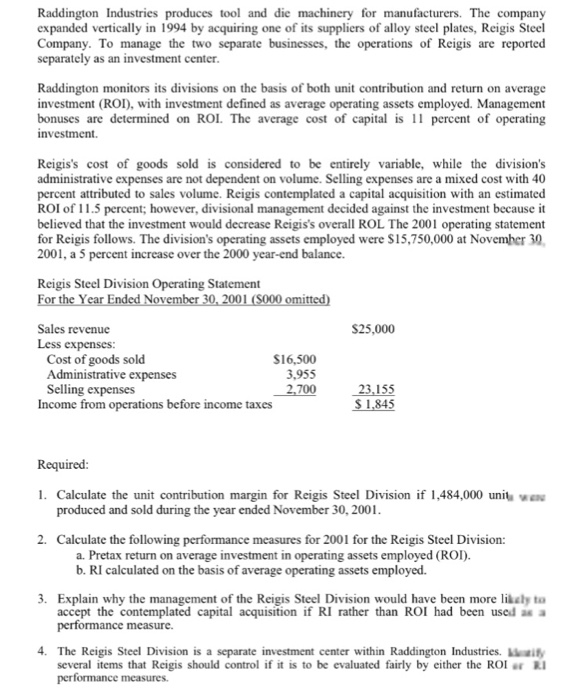

Raddington Industries produces tool and die machinery for manufacturers. The company expanded vertically in 1994 by acquiring one o f its suppliers of alloy steel plates, Reigis Steel Company. To manage the two separate businesses, the operations of Reigis arc reported separately as an investment center. Raddington monitors its divisions on the basis of both unit contribution and return on average investment (ROI). with investment defined as average operating assets employed. Management bonuses are determined on ROI. The average cost of capital is 11 percent o f operating investment. Reigis's cost of goods sold is considered to be entirely variable, while the division's administrative expenses are not dependent on volume. Selling expenses are a mixed cost with 40 percent attributed to sales volume. Reigis contemplated a capital acquisition with an estimated ROI o f 11.5 percent; however, divisional management decided against the investment because it believed that the investment would decrease Reigis's overall ROL The 2001 operating statement for Reigis follows. The division's operating assets employed were $15,750.000 at November Vi 2001, a 5 percent increase over the 2000 year-end balance. Reigis Steel Division Operating Statement For the Year lindcd November 30. 2001 ($000 omitted) Required: Calculate the unit contribution margin for Reigis Steel Division if 1.484,000 unin produced and sold during the year ended November 30.2001. Calculate the following performance measures for 2001 for the Reigis Steel Division: Pretax return on average investment in operating assets employed (ROI). RI calculated on the basis of av erage operating assets employed. Explain why the management of the Reigis Steel Division would have been more like accept the contemplated capital acquisition if RI rather than ROI had been used as a performance measure. The Reigis Steel Division is a separate investment center within Raddington Industries, k several items that Reigis should control if it is to be evaluated fairly by either the ROI or RI performance measures. Raddington Industries produces tool and die machinery for manufacturers. The company expanded vertically in 1994 by acquiring one o f its suppliers of alloy steel plates, Reigis Steel Company. To manage the two separate businesses, the operations of Reigis arc reported separately as an investment center. Raddington monitors its divisions on the basis of both unit contribution and return on average investment (ROI). with investment defined as average operating assets employed. Management bonuses are determined on ROI. The average cost of capital is 11 percent o f operating investment. Reigis's cost of goods sold is considered to be entirely variable, while the division's administrative expenses are not dependent on volume. Selling expenses are a mixed cost with 40 percent attributed to sales volume. Reigis contemplated a capital acquisition with an estimated ROI o f 11.5 percent; however, divisional management decided against the investment because it believed that the investment would decrease Reigis's overall ROL The 2001 operating statement for Reigis follows. The division's operating assets employed were $15,750.000 at November Vi 2001, a 5 percent increase over the 2000 year-end balance. Reigis Steel Division Operating Statement For the Year lindcd November 30. 2001 ($000 omitted) Required: Calculate the unit contribution margin for Reigis Steel Division if 1.484,000 unin produced and sold during the year ended November 30.2001. Calculate the following performance measures for 2001 for the Reigis Steel Division: Pretax return on average investment in operating assets employed (ROI). RI calculated on the basis of av erage operating assets employed. Explain why the management of the Reigis Steel Division would have been more like accept the contemplated capital acquisition if RI rather than ROI had been used as a performance measure. The Reigis Steel Division is a separate investment center within Raddington Industries, k several items that Reigis should control if it is to be evaluated fairly by either the ROI or RI performance measures