Answered step by step

Verified Expert Solution

Question

1 Approved Answer

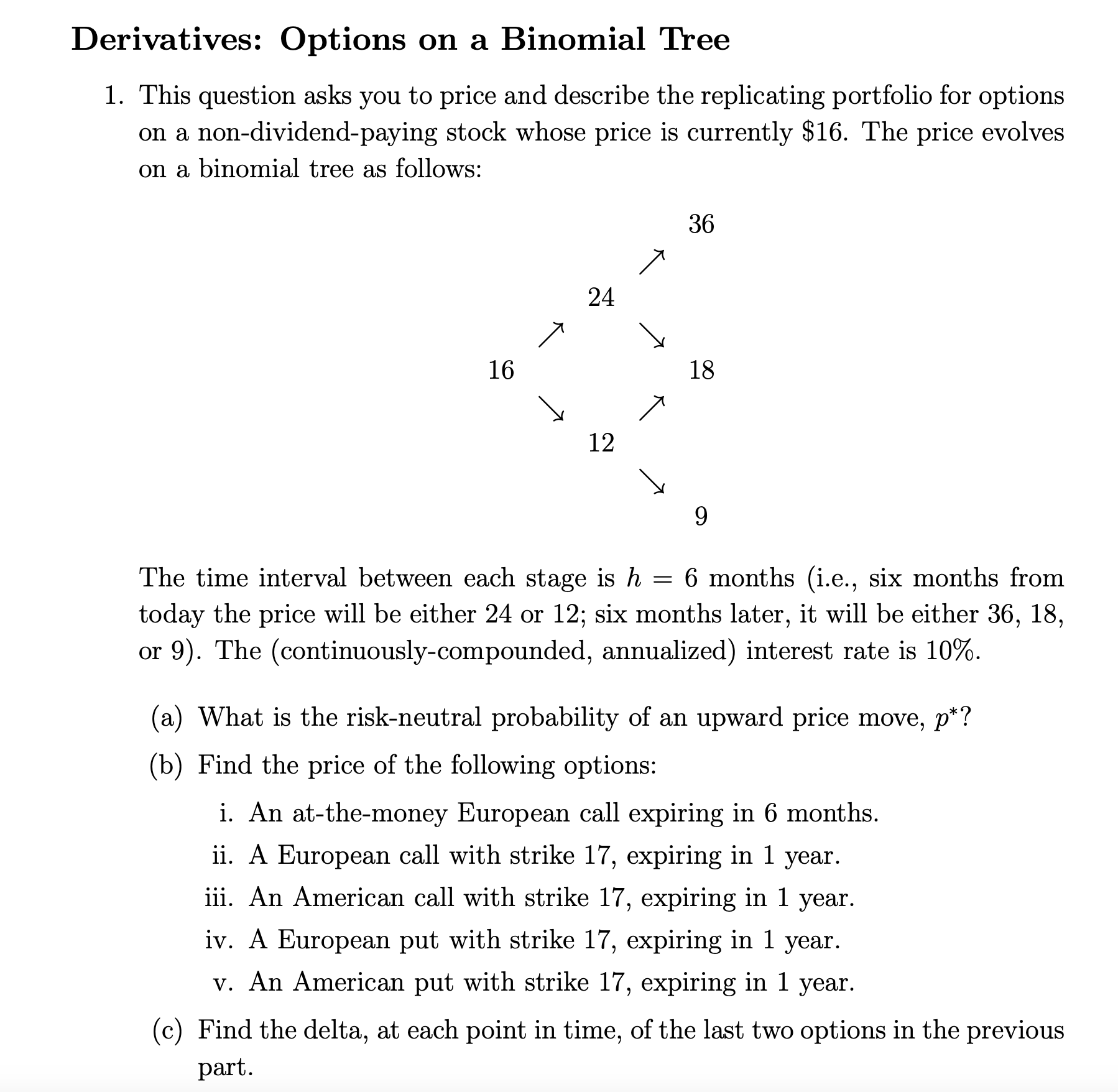

Perivatives: Options on a Binomial Tree 1. This question asks you to price and describe the replicating portfolio for options on a non-dividend-paying stock whose

Perivatives: Options on a Binomial Tree 1. This question asks you to price and describe the replicating portfolio for options on a non-dividend-paying stock whose price is currently $16. The price evolves on a binomial tree as follows: The time interval between each stage is h=6 months (i.e., six months from today the price will be either 24 or 12 ; six months later, it will be either 36,18 , or 9 ). The (continuously-compounded, annualized) interest rate is 10%. (a) What is the risk-neutral probability of an upward price move, p ? (b) Find the price of the following options: i. An at-the-money European call expiring in 6 months. ii. A European call with strike 17, expiring in 1 year. iii. An American call with strike 17, expiring in 1 year. iv. A European put with strike 17, expiring in 1 year. v. An American put with strike 17, expiring in 1 year. (c) Find the delta, at each point in time, of the last two options in the previous part

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Financial Planning For Executives And Entrepreneurs

Authors: Michael J. Nathanson, Jeffrey T. Craig, Jennifer A. Geoghegan, Nadine Gordon Lee, Michael A. Haber, Seth P. Hieken, Matthew C. Ilteris, D. Scott McDonald, Joseph A. Salvati, Stephen R. Stelljes

1st Edition

3030405273, 978-3030405274