Answered step by step

Verified Expert Solution

Question

1 Approved Answer

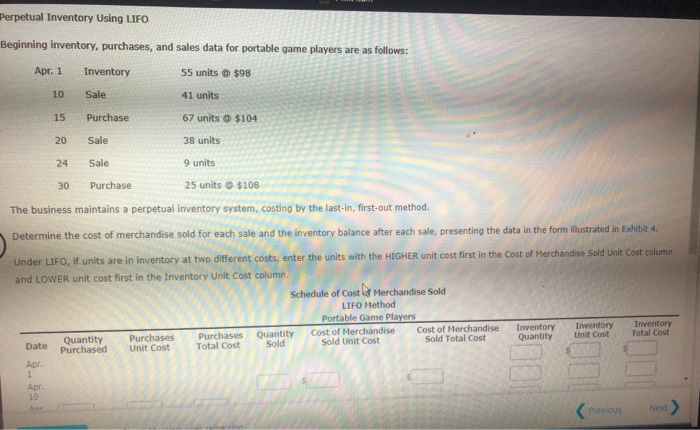

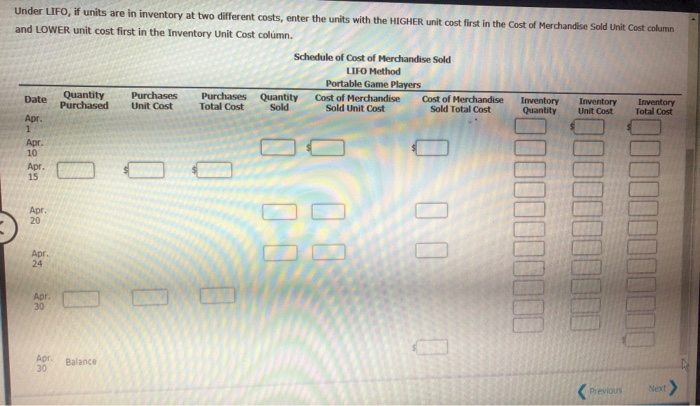

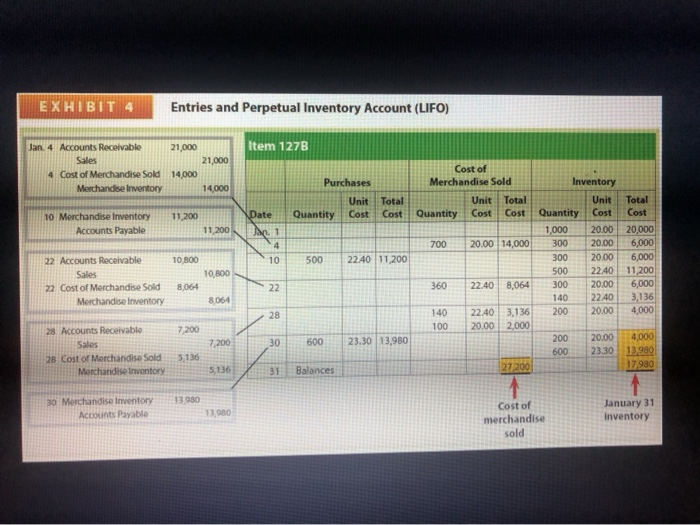

Perpetual Inventory Using LIFO Beginning inventory, purchases, and sales data for portable game players are Apr. 1 Inventory 55 units $98 Sale 41 units Purchase

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Report Chavarria Dinne And Lamey LLC Contract Deliverables Office Of Inspector U.S Department Of The Interior

Authors: United States Department Of The Interior

1st Edition

1511678526, 978-1511678520