Question: Personal Financial Planning Your derivable for this Activity 5 is to answer the 3 questions given at the end of this information sheet. A little

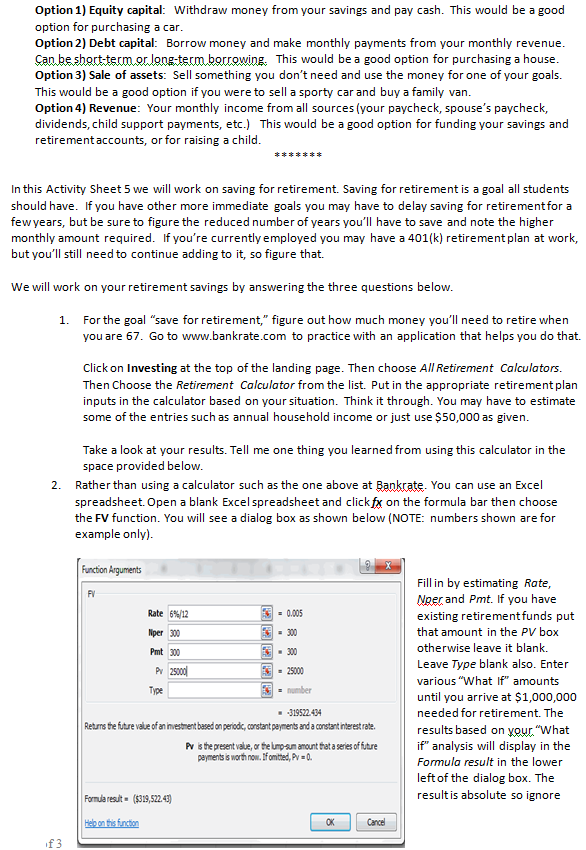

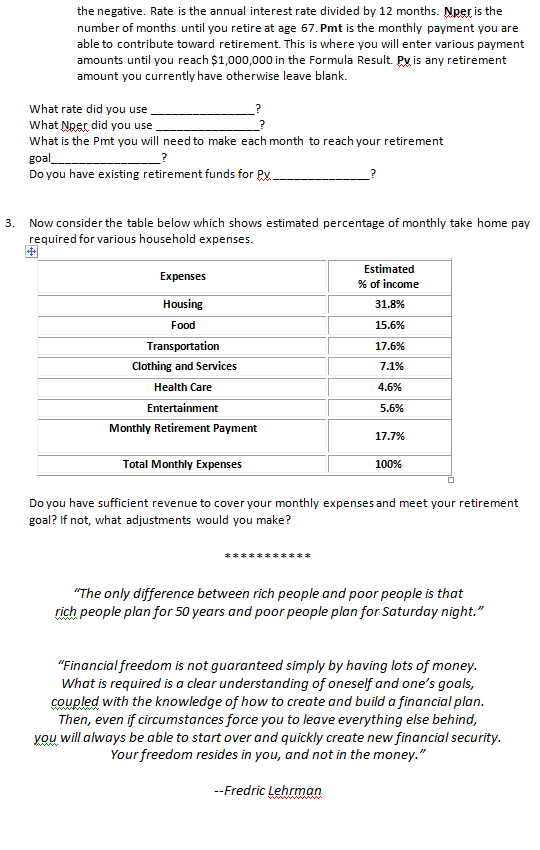

Personal Financial Planning Your derivable for this Activity 5 is to answer the 3 questions given at the end of this information sheet. A little background first. Financial management involves preparing a plan for obtaining and using the money needed to accomplish a firm's goals and objectives. Individuals should also use a financial plan to accomplish their personal goals and objectives. For this activity you will be calculating how much you have to save for retirement. Most people never make goals. They've heard that goal setting is important but this simple act is ignored and avoided. Some have set goals in the past but they've failed to obtain them. Then there's that group that feels that their destination's too far off. And finally, there are those who think that the goal setting process is just too difficult. No matter where you are on your quest for success-if you're just starting or on your way-determining your goals is the most important thing you can do. It doesn't matter whether or not you're in debt, just getting started on well-established goal setting is still important. One of the things you must understand about the goal setting process is that it doesn't have to be complicated but it does have to be specific. In fact, there are four questions that you need to answer when it comes to setting a goal. The first question is: What am I trying to accomplish? The next: How much time do I have? Third: How much money do I have to work with now and in the future? And finally: What rate of return am I seeking on my money? The most common financial goals are: getting out of debt, home ownership, college education funding, and financial independence in retirement. Use the list below to think about your goals and objectives Education and Career: What level do you want to reach in your career? Is there additional education you will need in order to achieve your career goals? Will you need to move to another part of the country to obtain your goal? Do you want to buy a business someday? Financial: How much money do you want to have in your savings, investments and retirement accounts? (These are three separate accounts, but you can choose just savings and retirement to start.) Do you have debt you want to pay off? Family: Do you want to marry? Have children? Create an education fund for your children? Personal: Do you want to buy a house? Buy a new or newer car? Go on vacations? Remodel a house? Get LASIK eye surgery or plastic surgery? Of the four areas listed above, Financial is the most important because you will need money to achieve all of your other goals. The second step is "Budget the amount of money needed to accomplish the goals and objectives" but before you can do that you need to know what your goals will cost. The last step "Identify the sources of funds." You have four options: Option 1) Equity capital: Withdraw money from your savings and pay cash. This would be a good option for purchasing a car. Option 2) Debt capital: Borrow money and make monthly payments from your monthly revenue. Can be short-term or long-term borrowing. This would be a good option for purchasing a house. Option 3) Sale of assets: Sell something you don't need and use the money for one of your goals. This would be a good option if you were to sell a sporty car and buy a family van. Option 4) Revenue: Your monthly income from all sources (your paycheck, spouse's paycheck, dividends, child support payments, etc.) This would be a good option for funding your savings and retirement accounts, or for raising a child. In this Activity Sheet 5 we will work on saving for retirement. Saving for retirement is a goal all students should have. If you have other more immediate goals you may have to delay saving for retirement for a few years, but be sure to figure the reduced number of years you'll have to save and note the higher monthly amount required. If you're currently employed you may have a 401(k) retirement plan at work, but you'll still need to continue adding to it, so figure that. We will work on your retirement savings by answering the three questions below. 1. For the goal "save for retirement," figure out how much money you'll need to retire when you are 67. Go to www.bankrate.com to practice with an application that helps you do that. Click on Investing at the top of the landing page. Then choose All Retirement Calculators. Then Choose the Retirement Calculator from the list. Put in the appropriate retirement plan inputs in the calculator based on your situation. Think it through. You may have to estimate some of the entries such as annual household income or just use $50,000 as given. Take a look at your results. Tell me one thing you learned from using this calculator in the space provided below. Rather than using a calculator such as the one above at Bankrate. You can use an Excel spreadsheet. Open a blank Excel spreadsheet and click fx on the formula bar then choose the FV function. You will see a dialog box as shown below (NOTE: numbers shown are for example only). Function Arguments 3 -0.005 3 - 25000 = number Fill in by estimating Rate, Nger and Pmt. If you have existing retirement funds put that amount in the PV box otherwise leave it blank. Leave Type blank also. Enter various "What if" amounts until you arrive at $1,000,000 needed for retirement. The results based on your."What if" analysis will display in the Formula result in the lower left of the dialog box. The result is absolute so ignore 319522.434 Returns the future value of an investment based on periodic, constant payments and a constant interest rate Pr is the present value, or the umpsun amount that a series of future payments is worth now. If omitted, P = 0. Formularesult - $319,522.43) Heb on this function the negative. Rate is the annual interest rate divided by 12 months. Nper is the nber of months until you retire at age 67. Pmt is the monthly payment you are able to contribute toward retirement. This is where you will enter various payment amounts until you reach $1,000,000 in the Formula Result. Py is any retirement amount you currently have otherwise leave blank. What rate did you use What Noer did you use What is the Pmt you will need to make each month to reach your retirement goal Do you have existing retirement funds for Px. - ____________? 3. Now consider the table below which shows estimated percentage of monthly take home pay required for various household expenses. Expenses Estimated % of income 31.8% 15.6% Housing Food Transportation Clothing and Services Health Care 17.6% 7.1% 4.6% Entertainment 5.6% Monthly Retirement Payment 17.7% Total Monthly Expenses 100% Do you have sufficient revenue to cover your monthly expenses and meet your retirement goal? If not, what adjustments would you make? "The only difference between rich people and poor people is that rich people plan for 50 years and poor people plan for Saturday night." "Financial freedom is not guaranteed simply by having lots of money. What is required is a clear understanding of oneself and one's goals, coupled with the knowledge of how to create and build a financial plan. Then, even if circumstances force you to leave everything else behind, you will always be able to start over and quickly create new financial security. Your freedom resides in you, and not in the money." --Fredric Lehrman Personal Financial Planning Your derivable for this Activity 5 is to answer the 3 questions given at the end of this information sheet. A little background first. Financial management involves preparing a plan for obtaining and using the money needed to accomplish a firm's goals and objectives. Individuals should also use a financial plan to accomplish their personal goals and objectives. For this activity you will be calculating how much you have to save for retirement. Most people never make goals. They've heard that goal setting is important but this simple act is ignored and avoided. Some have set goals in the past but they've failed to obtain them. Then there's that group that feels that their destination's too far off. And finally, there are those who think that the goal setting process is just too difficult. No matter where you are on your quest for success-if you're just starting or on your way-determining your goals is the most important thing you can do. It doesn't matter whether or not you're in debt, just getting started on well-established goal setting is still important. One of the things you must understand about the goal setting process is that it doesn't have to be complicated but it does have to be specific. In fact, there are four questions that you need to answer when it comes to setting a goal. The first question is: What am I trying to accomplish? The next: How much time do I have? Third: How much money do I have to work with now and in the future? And finally: What rate of return am I seeking on my money? The most common financial goals are: getting out of debt, home ownership, college education funding, and financial independence in retirement. Use the list below to think about your goals and objectives Education and Career: What level do you want to reach in your career? Is there additional education you will need in order to achieve your career goals? Will you need to move to another part of the country to obtain your goal? Do you want to buy a business someday? Financial: How much money do you want to have in your savings, investments and retirement accounts? (These are three separate accounts, but you can choose just savings and retirement to start.) Do you have debt you want to pay off? Family: Do you want to marry? Have children? Create an education fund for your children? Personal: Do you want to buy a house? Buy a new or newer car? Go on vacations? Remodel a house? Get LASIK eye surgery or plastic surgery? Of the four areas listed above, Financial is the most important because you will need money to achieve all of your other goals. The second step is "Budget the amount of money needed to accomplish the goals and objectives" but before you can do that you need to know what your goals will cost. The last step "Identify the sources of funds." You have four options: Option 1) Equity capital: Withdraw money from your savings and pay cash. This would be a good option for purchasing a car. Option 2) Debt capital: Borrow money and make monthly payments from your monthly revenue. Can be short-term or long-term borrowing. This would be a good option for purchasing a house. Option 3) Sale of assets: Sell something you don't need and use the money for one of your goals. This would be a good option if you were to sell a sporty car and buy a family van. Option 4) Revenue: Your monthly income from all sources (your paycheck, spouse's paycheck, dividends, child support payments, etc.) This would be a good option for funding your savings and retirement accounts, or for raising a child. In this Activity Sheet 5 we will work on saving for retirement. Saving for retirement is a goal all students should have. If you have other more immediate goals you may have to delay saving for retirement for a few years, but be sure to figure the reduced number of years you'll have to save and note the higher monthly amount required. If you're currently employed you may have a 401(k) retirement plan at work, but you'll still need to continue adding to it, so figure that. We will work on your retirement savings by answering the three questions below. 1. For the goal "save for retirement," figure out how much money you'll need to retire when you are 67. Go to www.bankrate.com to practice with an application that helps you do that. Click on Investing at the top of the landing page. Then choose All Retirement Calculators. Then Choose the Retirement Calculator from the list. Put in the appropriate retirement plan inputs in the calculator based on your situation. Think it through. You may have to estimate some of the entries such as annual household income or just use $50,000 as given. Take a look at your results. Tell me one thing you learned from using this calculator in the space provided below. Rather than using a calculator such as the one above at Bankrate. You can use an Excel spreadsheet. Open a blank Excel spreadsheet and click fx on the formula bar then choose the FV function. You will see a dialog box as shown below (NOTE: numbers shown are for example only). Function Arguments 3 -0.005 3 - 25000 = number Fill in by estimating Rate, Nger and Pmt. If you have existing retirement funds put that amount in the PV box otherwise leave it blank. Leave Type blank also. Enter various "What if" amounts until you arrive at $1,000,000 needed for retirement. The results based on your."What if" analysis will display in the Formula result in the lower left of the dialog box. The result is absolute so ignore 319522.434 Returns the future value of an investment based on periodic, constant payments and a constant interest rate Pr is the present value, or the umpsun amount that a series of future payments is worth now. If omitted, P = 0. Formularesult - $319,522.43) Heb on this function the negative. Rate is the annual interest rate divided by 12 months. Nper is the nber of months until you retire at age 67. Pmt is the monthly payment you are able to contribute toward retirement. This is where you will enter various payment amounts until you reach $1,000,000 in the Formula Result. Py is any retirement amount you currently have otherwise leave blank. What rate did you use What Noer did you use What is the Pmt you will need to make each month to reach your retirement goal Do you have existing retirement funds for Px. - ____________? 3. Now consider the table below which shows estimated percentage of monthly take home pay required for various household expenses. Expenses Estimated % of income 31.8% 15.6% Housing Food Transportation Clothing and Services Health Care 17.6% 7.1% 4.6% Entertainment 5.6% Monthly Retirement Payment 17.7% Total Monthly Expenses 100% Do you have sufficient revenue to cover your monthly expenses and meet your retirement goal? If not, what adjustments would you make? "The only difference between rich people and poor people is that rich people plan for 50 years and poor people plan for Saturday night." "Financial freedom is not guaranteed simply by having lots of money. What is required is a clear understanding of oneself and one's goals, coupled with the knowledge of how to create and build a financial plan. Then, even if circumstances force you to leave everything else behind, you will always be able to start over and quickly create new financial security. Your freedom resides in you, and not in the money." --Fredric Lehrman

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts