Answered step by step

Verified Expert Solution

Question

1 Approved Answer

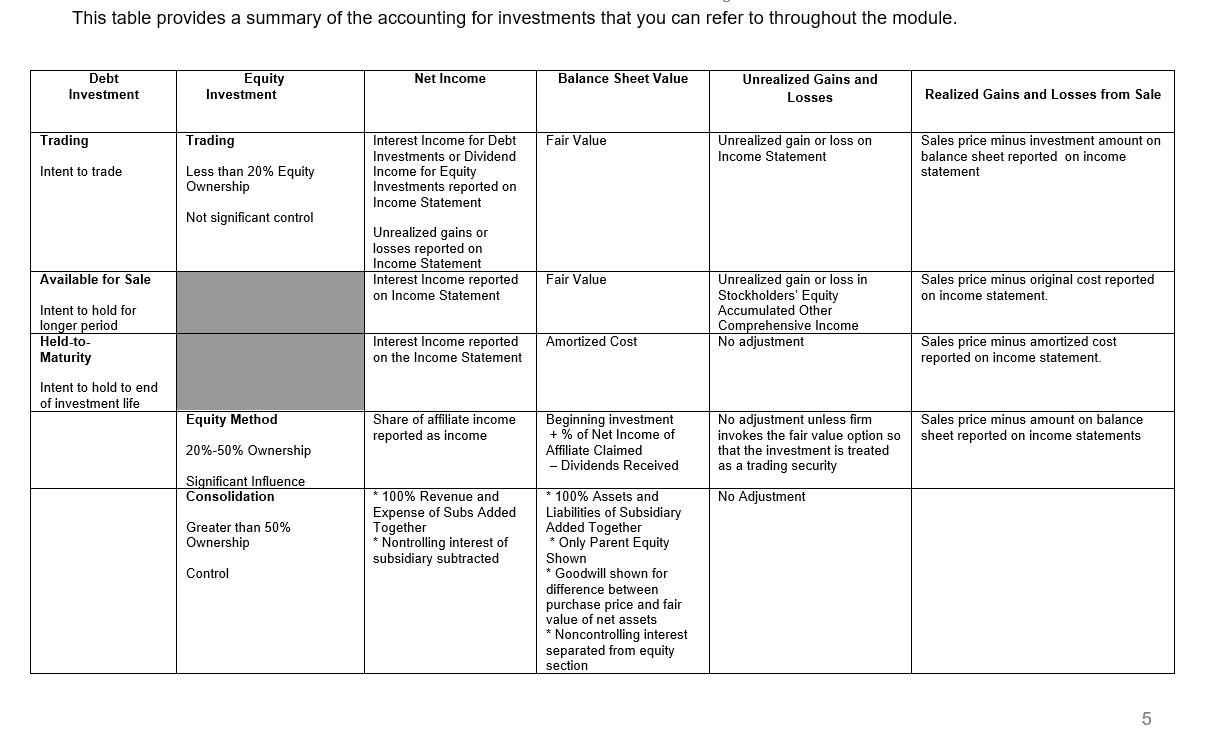

pg. 5 notes: This table provides a summary of the accounting for investments that you can refer to throughout the module. begin{tabular}{|c|c|c|c|c|c|} hline begin{tabular}{c} Debt

pg. 5 notes:

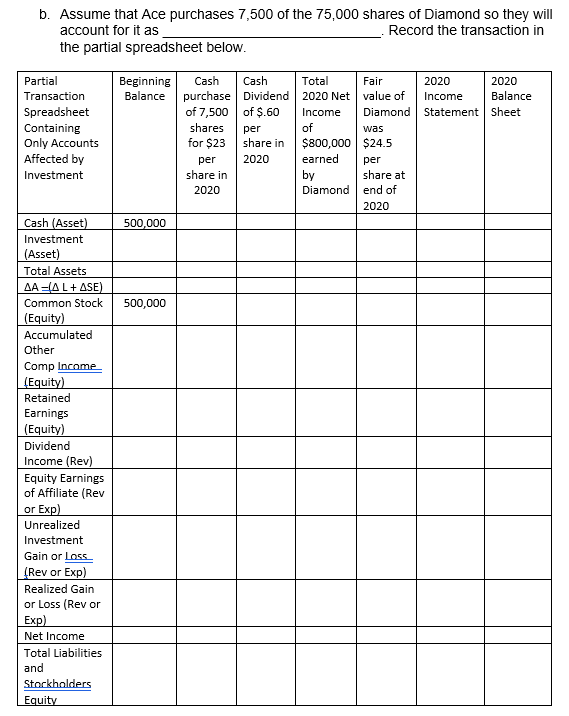

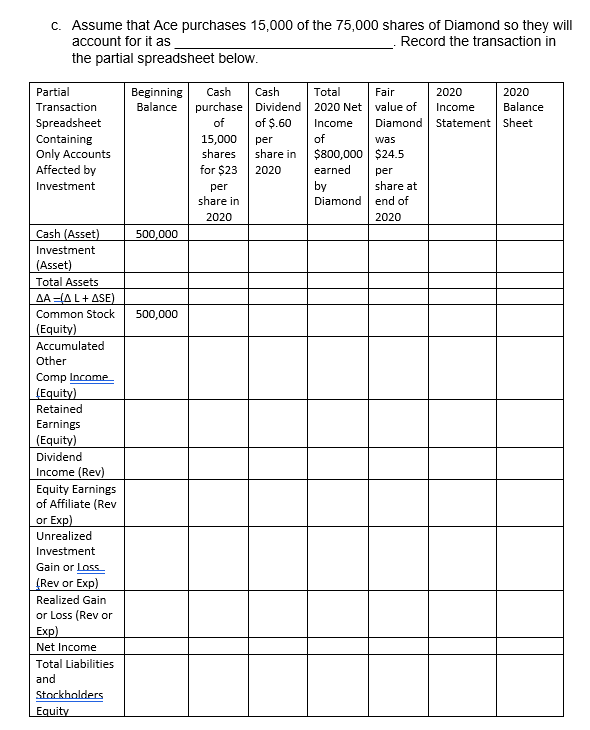

This table provides a summary of the accounting for investments that you can refer to throughout the module. \begin{tabular}{|c|c|c|c|c|c|} \hline \begin{tabular}{c} Debt \\ Investment \end{tabular} & \begin{tabular}{l} Equity \\ Investment \end{tabular} & Net Income & Balance Sheet Value & \begin{tabular}{l} Unrealized Gains and \\ Losses \end{tabular} & Realized Gains and Losses from Sale \\ \hline \begin{tabular}{l} Trading \\ Intent to trade \end{tabular} & \begin{tabular}{l} Trading \\ Less than 20\% Equity \\ Ownership \\ Not significant control \end{tabular} & \begin{tabular}{l} Interest Income for Debt \\ Investments or Dividend \\ Income for Equity \\ Investments reported on \\ Income Statement \\ Unrealized gains or \\ losses reported on \\ Income Statement \end{tabular} & Fair Value & \begin{tabular}{l} Unrealized gain or loss on \\ Income Statement \end{tabular} & \begin{tabular}{l} Sales price minus investment amount on \\ balance sheet reported on income \\ statement \end{tabular} \\ \hline \begin{tabular}{l} Available for Sale \\ Intent to hold for \\ longer period \end{tabular} & & \begin{tabular}{l} Interest Income reported \\ on Income Statement \end{tabular} & Fair Value & \begin{tabular}{l} Unrealized gain or loss in \\ Stockholders' Equity \\ Accumulated Other \\ Comprehensive Income \end{tabular} & \begin{tabular}{l} Sales price minus original cost reported \\ on income statement. \end{tabular} \\ \hline \multirow{3}{*}{\begin{tabular}{l} Held-to- \\ Maturity \\ Intent to hold to end \\ of investment life \end{tabular}} & & \begin{tabular}{l} Interest Income reported \\ on the Income Statement \end{tabular} & Amortized Cost & No adjustment & \begin{tabular}{l} Sales price minus amortized cost \\ reported on income statement. \end{tabular} \\ \hline & \begin{tabular}{l} Equity Method \\ 20%50% Ownership \\ Significant Influence \end{tabular} & \begin{tabular}{l} Share of affiliate income \\ reported as income \end{tabular} & \begin{tabular}{l} Beginning investment \\ +% of Net Income of \\ Affiliate Claimed \\ - Dividends Received \end{tabular} & \begin{tabular}{l} No adjustment unless firm \\ invokes the fair value option so \\ that the investment is treated \\ as a trading security \end{tabular} & \begin{tabular}{l} Sales price minus amount on balance \\ sheet reported on income statements \end{tabular} \\ \hline & \begin{tabular}{l} Consolidation \\ Greater than 50% \\ Ownership \\ Control \end{tabular} & \begin{tabular}{l} 100% Revenue and \\ Expense of Subs Added \\ Together \\ Nontrolling interest of \\ subsidiary subtracted \end{tabular} & \begin{tabular}{l} 100% Assets and \\ Liabilities of Subsidiary \\ Added Together \\ Only Parent Equity \\ Shown \\ Goodwill shown for \\ difference between \\ purchase price and fair \\ value of net assets \\ Noncontrolling interest \\ separated from equity \\ section \end{tabular} & No Adjustment & \\ \hline \end{tabular} 5 C. Assume that Ace purchases 15,000 of the 75,000 shares of Diamond so they will Question 3: Equity Investment Example a. Ace Company purchases shares of stock in Diamond Company. According to the summary table on page 5 of the notes, what determines how Ace's investment in Diamond stock is accounted for under GAAP? d. Assume that Ace purchases all 75,000 shares of Diamond so they will account for it as a Assume that the book value of Diamond's assets was $1,200,000 and the Diamond liabilities assumed was $300,000. The fair value of Diamond's PPE exceeded the book value by $200,000. What is the amount of goodwill that is recognized by Ace? b. Assume that Ace purchases 7,500 of the 75,000 shares of Diamond so they will This table provides a summary of the accounting for investments that you can refer to throughout the module. \begin{tabular}{|c|c|c|c|c|c|} \hline \begin{tabular}{c} Debt \\ Investment \end{tabular} & \begin{tabular}{l} Equity \\ Investment \end{tabular} & Net Income & Balance Sheet Value & \begin{tabular}{l} Unrealized Gains and \\ Losses \end{tabular} & Realized Gains and Losses from Sale \\ \hline \begin{tabular}{l} Trading \\ Intent to trade \end{tabular} & \begin{tabular}{l} Trading \\ Less than 20\% Equity \\ Ownership \\ Not significant control \end{tabular} & \begin{tabular}{l} Interest Income for Debt \\ Investments or Dividend \\ Income for Equity \\ Investments reported on \\ Income Statement \\ Unrealized gains or \\ losses reported on \\ Income Statement \end{tabular} & Fair Value & \begin{tabular}{l} Unrealized gain or loss on \\ Income Statement \end{tabular} & \begin{tabular}{l} Sales price minus investment amount on \\ balance sheet reported on income \\ statement \end{tabular} \\ \hline \begin{tabular}{l} Available for Sale \\ Intent to hold for \\ longer period \end{tabular} & & \begin{tabular}{l} Interest Income reported \\ on Income Statement \end{tabular} & Fair Value & \begin{tabular}{l} Unrealized gain or loss in \\ Stockholders' Equity \\ Accumulated Other \\ Comprehensive Income \end{tabular} & \begin{tabular}{l} Sales price minus original cost reported \\ on income statement. \end{tabular} \\ \hline \multirow{3}{*}{\begin{tabular}{l} Held-to- \\ Maturity \\ Intent to hold to end \\ of investment life \end{tabular}} & & \begin{tabular}{l} Interest Income reported \\ on the Income Statement \end{tabular} & Amortized Cost & No adjustment & \begin{tabular}{l} Sales price minus amortized cost \\ reported on income statement. \end{tabular} \\ \hline & \begin{tabular}{l} Equity Method \\ 20%50% Ownership \\ Significant Influence \end{tabular} & \begin{tabular}{l} Share of affiliate income \\ reported as income \end{tabular} & \begin{tabular}{l} Beginning investment \\ +% of Net Income of \\ Affiliate Claimed \\ - Dividends Received \end{tabular} & \begin{tabular}{l} No adjustment unless firm \\ invokes the fair value option so \\ that the investment is treated \\ as a trading security \end{tabular} & \begin{tabular}{l} Sales price minus amount on balance \\ sheet reported on income statements \end{tabular} \\ \hline & \begin{tabular}{l} Consolidation \\ Greater than 50% \\ Ownership \\ Control \end{tabular} & \begin{tabular}{l} 100% Revenue and \\ Expense of Subs Added \\ Together \\ Nontrolling interest of \\ subsidiary subtracted \end{tabular} & \begin{tabular}{l} 100% Assets and \\ Liabilities of Subsidiary \\ Added Together \\ Only Parent Equity \\ Shown \\ Goodwill shown for \\ difference between \\ purchase price and fair \\ value of net assets \\ Noncontrolling interest \\ separated from equity \\ section \end{tabular} & No Adjustment & \\ \hline \end{tabular} 5 C. Assume that Ace purchases 15,000 of the 75,000 shares of Diamond so they will Question 3: Equity Investment Example a. Ace Company purchases shares of stock in Diamond Company. According to the summary table on page 5 of the notes, what determines how Ace's investment in Diamond stock is accounted for under GAAP? d. Assume that Ace purchases all 75,000 shares of Diamond so they will account for it as a Assume that the book value of Diamond's assets was $1,200,000 and the Diamond liabilities assumed was $300,000. The fair value of Diamond's PPE exceeded the book value by $200,000. What is the amount of goodwill that is recognized by Ace? b. Assume that Ace purchases 7,500 of the 75,000 shares of Diamond so they will

This table provides a summary of the accounting for investments that you can refer to throughout the module. \begin{tabular}{|c|c|c|c|c|c|} \hline \begin{tabular}{c} Debt \\ Investment \end{tabular} & \begin{tabular}{l} Equity \\ Investment \end{tabular} & Net Income & Balance Sheet Value & \begin{tabular}{l} Unrealized Gains and \\ Losses \end{tabular} & Realized Gains and Losses from Sale \\ \hline \begin{tabular}{l} Trading \\ Intent to trade \end{tabular} & \begin{tabular}{l} Trading \\ Less than 20\% Equity \\ Ownership \\ Not significant control \end{tabular} & \begin{tabular}{l} Interest Income for Debt \\ Investments or Dividend \\ Income for Equity \\ Investments reported on \\ Income Statement \\ Unrealized gains or \\ losses reported on \\ Income Statement \end{tabular} & Fair Value & \begin{tabular}{l} Unrealized gain or loss on \\ Income Statement \end{tabular} & \begin{tabular}{l} Sales price minus investment amount on \\ balance sheet reported on income \\ statement \end{tabular} \\ \hline \begin{tabular}{l} Available for Sale \\ Intent to hold for \\ longer period \end{tabular} & & \begin{tabular}{l} Interest Income reported \\ on Income Statement \end{tabular} & Fair Value & \begin{tabular}{l} Unrealized gain or loss in \\ Stockholders' Equity \\ Accumulated Other \\ Comprehensive Income \end{tabular} & \begin{tabular}{l} Sales price minus original cost reported \\ on income statement. \end{tabular} \\ \hline \multirow{3}{*}{\begin{tabular}{l} Held-to- \\ Maturity \\ Intent to hold to end \\ of investment life \end{tabular}} & & \begin{tabular}{l} Interest Income reported \\ on the Income Statement \end{tabular} & Amortized Cost & No adjustment & \begin{tabular}{l} Sales price minus amortized cost \\ reported on income statement. \end{tabular} \\ \hline & \begin{tabular}{l} Equity Method \\ 20%50% Ownership \\ Significant Influence \end{tabular} & \begin{tabular}{l} Share of affiliate income \\ reported as income \end{tabular} & \begin{tabular}{l} Beginning investment \\ +% of Net Income of \\ Affiliate Claimed \\ - Dividends Received \end{tabular} & \begin{tabular}{l} No adjustment unless firm \\ invokes the fair value option so \\ that the investment is treated \\ as a trading security \end{tabular} & \begin{tabular}{l} Sales price minus amount on balance \\ sheet reported on income statements \end{tabular} \\ \hline & \begin{tabular}{l} Consolidation \\ Greater than 50% \\ Ownership \\ Control \end{tabular} & \begin{tabular}{l} 100% Revenue and \\ Expense of Subs Added \\ Together \\ Nontrolling interest of \\ subsidiary subtracted \end{tabular} & \begin{tabular}{l} 100% Assets and \\ Liabilities of Subsidiary \\ Added Together \\ Only Parent Equity \\ Shown \\ Goodwill shown for \\ difference between \\ purchase price and fair \\ value of net assets \\ Noncontrolling interest \\ separated from equity \\ section \end{tabular} & No Adjustment & \\ \hline \end{tabular} 5 C. Assume that Ace purchases 15,000 of the 75,000 shares of Diamond so they will Question 3: Equity Investment Example a. Ace Company purchases shares of stock in Diamond Company. According to the summary table on page 5 of the notes, what determines how Ace's investment in Diamond stock is accounted for under GAAP? d. Assume that Ace purchases all 75,000 shares of Diamond so they will account for it as a Assume that the book value of Diamond's assets was $1,200,000 and the Diamond liabilities assumed was $300,000. The fair value of Diamond's PPE exceeded the book value by $200,000. What is the amount of goodwill that is recognized by Ace? b. Assume that Ace purchases 7,500 of the 75,000 shares of Diamond so they will This table provides a summary of the accounting for investments that you can refer to throughout the module. \begin{tabular}{|c|c|c|c|c|c|} \hline \begin{tabular}{c} Debt \\ Investment \end{tabular} & \begin{tabular}{l} Equity \\ Investment \end{tabular} & Net Income & Balance Sheet Value & \begin{tabular}{l} Unrealized Gains and \\ Losses \end{tabular} & Realized Gains and Losses from Sale \\ \hline \begin{tabular}{l} Trading \\ Intent to trade \end{tabular} & \begin{tabular}{l} Trading \\ Less than 20\% Equity \\ Ownership \\ Not significant control \end{tabular} & \begin{tabular}{l} Interest Income for Debt \\ Investments or Dividend \\ Income for Equity \\ Investments reported on \\ Income Statement \\ Unrealized gains or \\ losses reported on \\ Income Statement \end{tabular} & Fair Value & \begin{tabular}{l} Unrealized gain or loss on \\ Income Statement \end{tabular} & \begin{tabular}{l} Sales price minus investment amount on \\ balance sheet reported on income \\ statement \end{tabular} \\ \hline \begin{tabular}{l} Available for Sale \\ Intent to hold for \\ longer period \end{tabular} & & \begin{tabular}{l} Interest Income reported \\ on Income Statement \end{tabular} & Fair Value & \begin{tabular}{l} Unrealized gain or loss in \\ Stockholders' Equity \\ Accumulated Other \\ Comprehensive Income \end{tabular} & \begin{tabular}{l} Sales price minus original cost reported \\ on income statement. \end{tabular} \\ \hline \multirow{3}{*}{\begin{tabular}{l} Held-to- \\ Maturity \\ Intent to hold to end \\ of investment life \end{tabular}} & & \begin{tabular}{l} Interest Income reported \\ on the Income Statement \end{tabular} & Amortized Cost & No adjustment & \begin{tabular}{l} Sales price minus amortized cost \\ reported on income statement. \end{tabular} \\ \hline & \begin{tabular}{l} Equity Method \\ 20%50% Ownership \\ Significant Influence \end{tabular} & \begin{tabular}{l} Share of affiliate income \\ reported as income \end{tabular} & \begin{tabular}{l} Beginning investment \\ +% of Net Income of \\ Affiliate Claimed \\ - Dividends Received \end{tabular} & \begin{tabular}{l} No adjustment unless firm \\ invokes the fair value option so \\ that the investment is treated \\ as a trading security \end{tabular} & \begin{tabular}{l} Sales price minus amount on balance \\ sheet reported on income statements \end{tabular} \\ \hline & \begin{tabular}{l} Consolidation \\ Greater than 50% \\ Ownership \\ Control \end{tabular} & \begin{tabular}{l} 100% Revenue and \\ Expense of Subs Added \\ Together \\ Nontrolling interest of \\ subsidiary subtracted \end{tabular} & \begin{tabular}{l} 100% Assets and \\ Liabilities of Subsidiary \\ Added Together \\ Only Parent Equity \\ Shown \\ Goodwill shown for \\ difference between \\ purchase price and fair \\ value of net assets \\ Noncontrolling interest \\ separated from equity \\ section \end{tabular} & No Adjustment & \\ \hline \end{tabular} 5 C. Assume that Ace purchases 15,000 of the 75,000 shares of Diamond so they will Question 3: Equity Investment Example a. Ace Company purchases shares of stock in Diamond Company. According to the summary table on page 5 of the notes, what determines how Ace's investment in Diamond stock is accounted for under GAAP? d. Assume that Ace purchases all 75,000 shares of Diamond so they will account for it as a Assume that the book value of Diamond's assets was $1,200,000 and the Diamond liabilities assumed was $300,000. The fair value of Diamond's PPE exceeded the book value by $200,000. What is the amount of goodwill that is recognized by Ace? b. Assume that Ace purchases 7,500 of the 75,000 shares of Diamond so they will Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started