P&G Facelle division a. Highlight potential decisions required in the case & which factors should P&G consider before making thesedecisions b. How are their own

P&G Facelle division

a. Highlight potential decisions required in the case & which factors should P&G consider before making thesedecisions

b. How are their own brands performing? Analyze in detail and explain the reason for their performance

c. How do consumers behave in this category?

d. How are different brands positioned in the market?

e.What will be your marketing strategy for Royale and Florelle

pg1

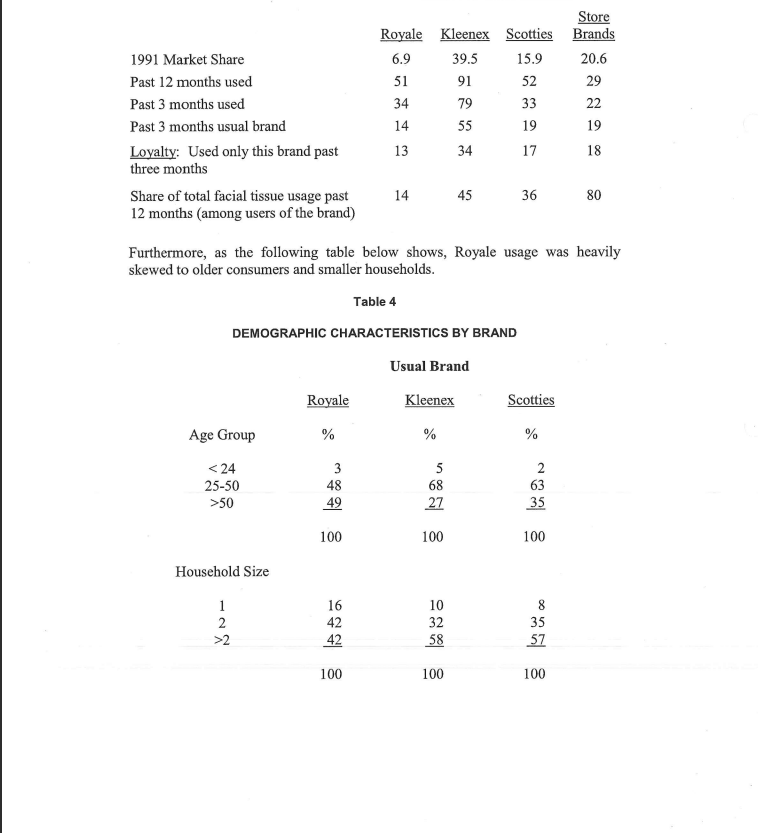

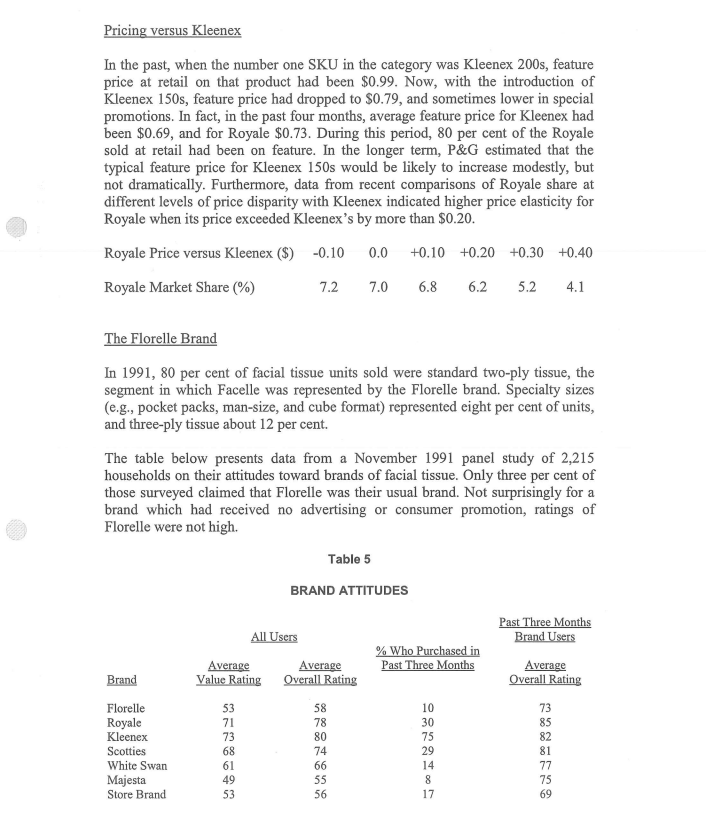

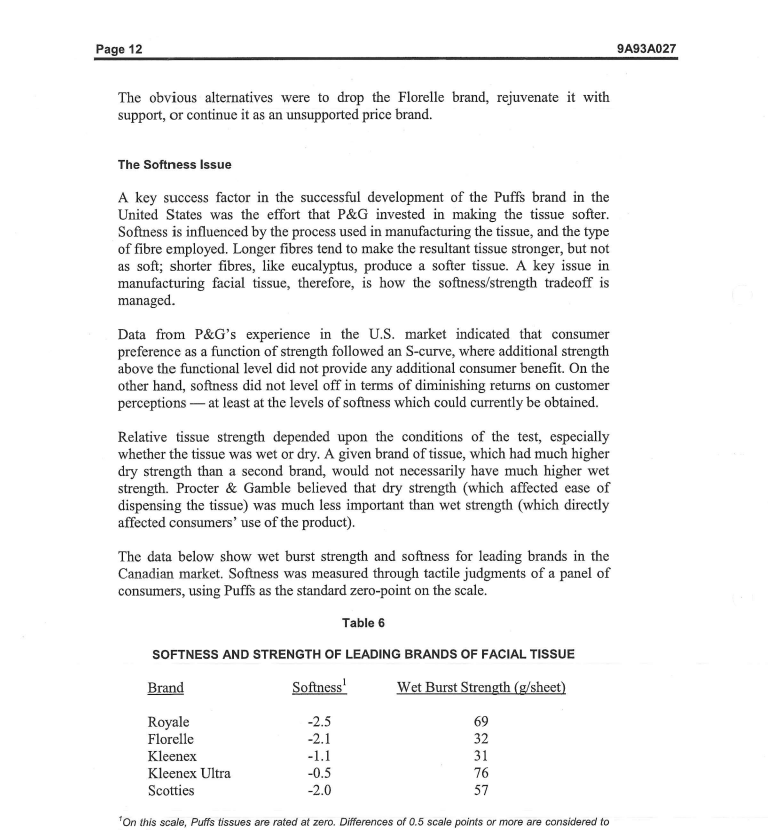

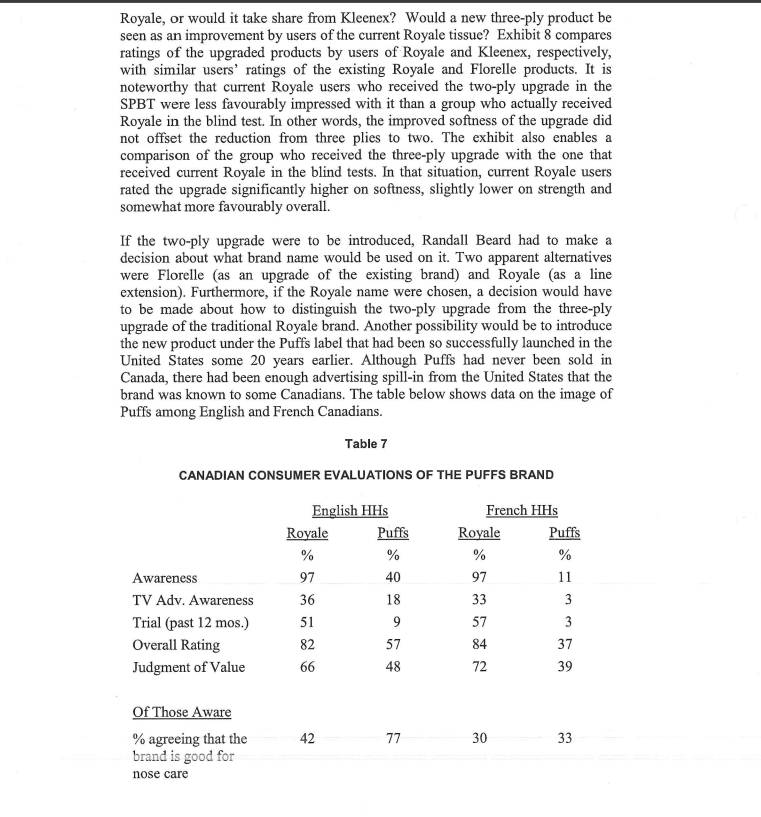

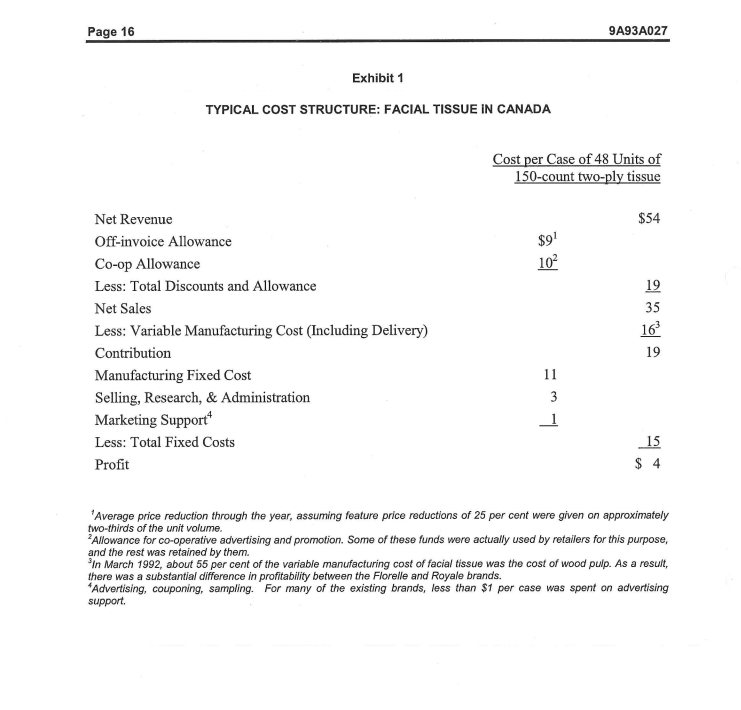

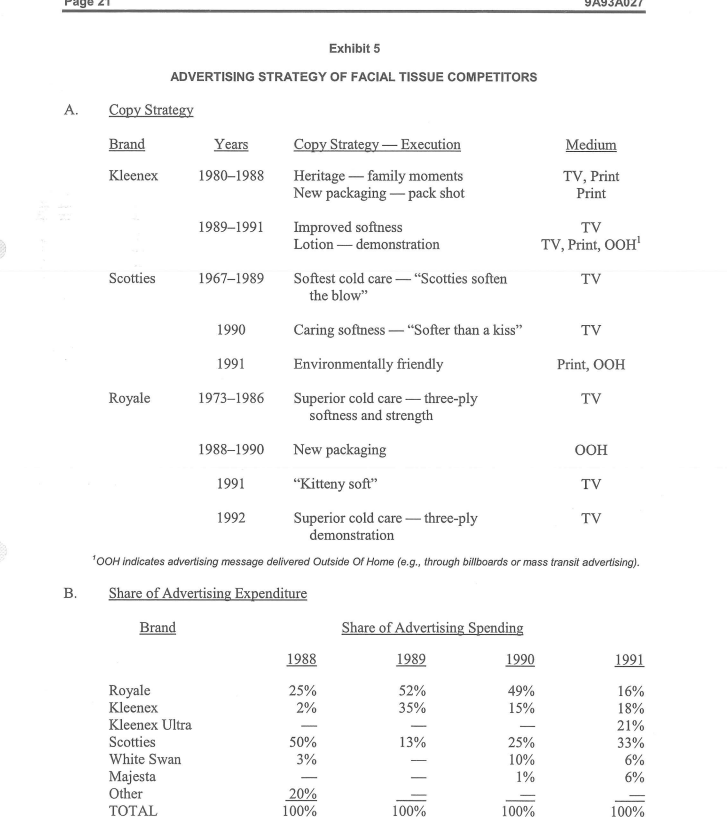

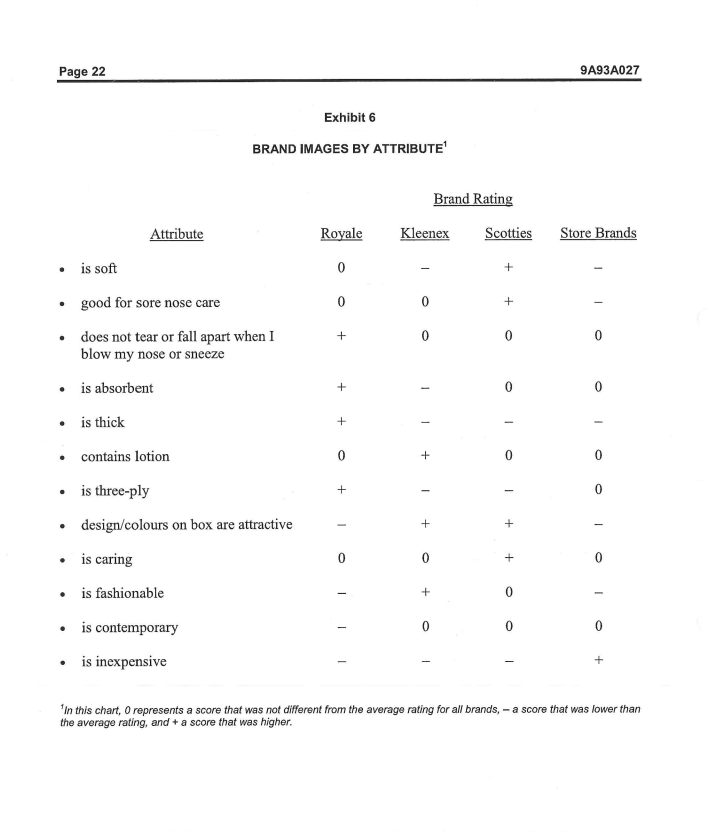

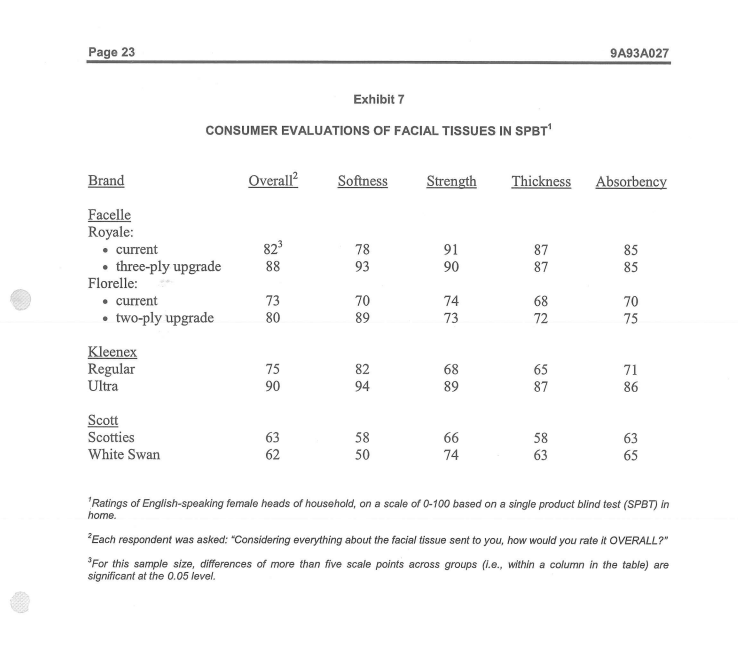

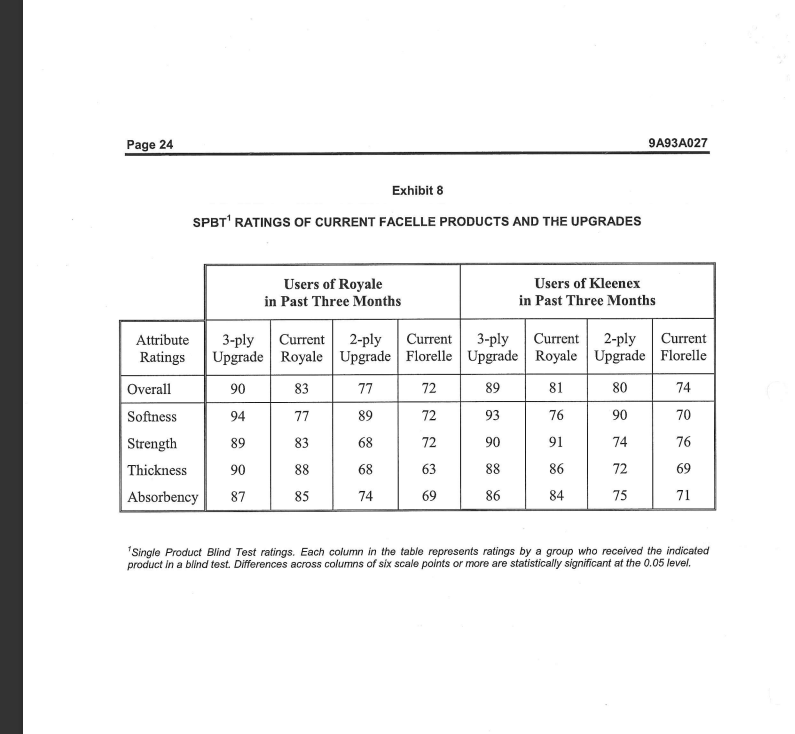

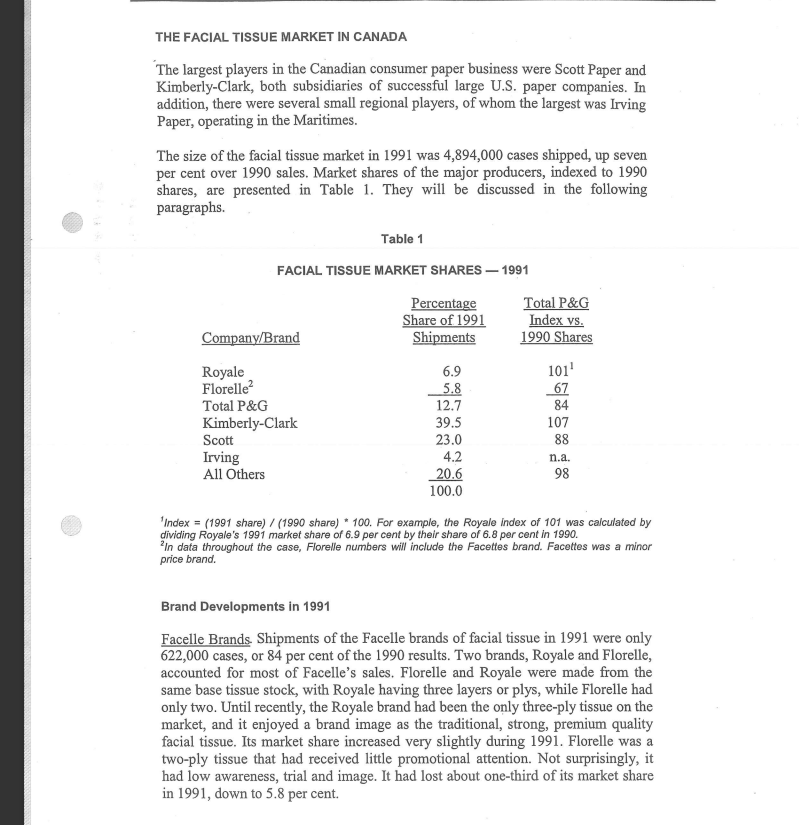

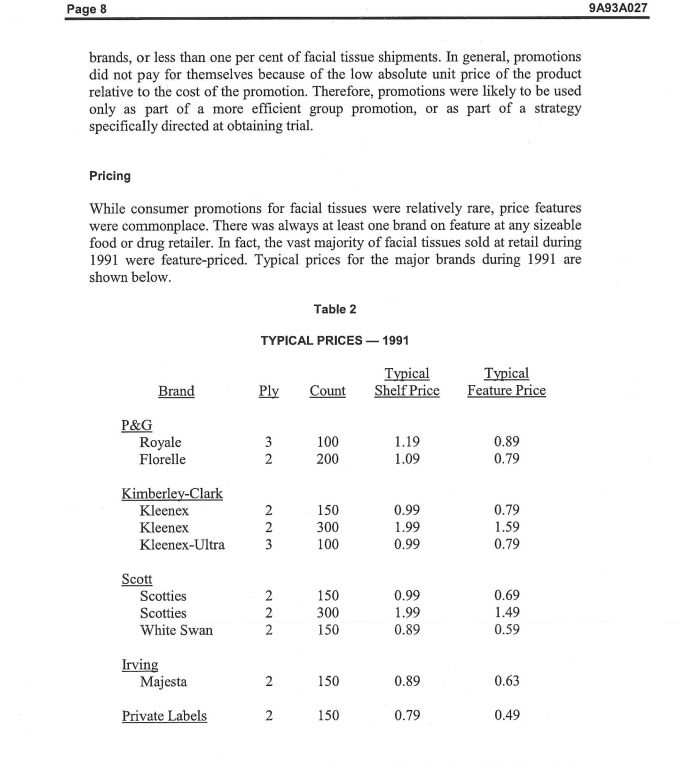

PROCTER 8: GAMBLE: FACELLE DIVISION FACIAL TISSUE Early in March 1992, Randall Beard was reviewing performance of the brands of facial tissue that Procter & Gamble had acquired in August 1991. \"Now that we have had a few months to understand the tissue business in Canada," he thought, \"it's time to build our plan for the future of the business. P850 hasn't spent $135 million in acquiring the Facellc division in order to stand still in the marketplace.\" Although Procter & Gamble had global brands in some categories of paper products (eg, Pampers, the leading disposable diaper), the Facelle acquisition was P&G's rst step outside the United States in the tissuer'towel business. For that reason, senior management would be closely watching the progress of the Facelle brands of facial tissue, paper towels, and bathroom tissue. In particular, the facial tissue market was especially challenging, as 1991 had seen more competitive product initiatives than the previous several years put together. As associate advertising manager for Tissue, Towel and Facial Products, Randall Beard reported directly to Barbara FraSer, vice president and general manager of the Paper Products business in Canada. Together, the two would be responsible for several major decisions about the facial tissue brands. including positioning, product formulations, and promotion. For his forthcoming meeting with Fraser, Beard wanted to have a set of denite recommendations on the lture of the brands, Store Royale Kleenex Scotties Brands 1991 Market Share 6.9 39.5 15.9 20.6 Past 12 months used 51 91 52 29 Past 3 months used 34 79 33 22 Past 3 months usual brand 14 55 19 19 Loyalty: Used only this brand past 13 34 17 18 three months Share of total facial tissue usage past 14 45 36 80 12 months (among users of the brand) Furthermore, as the following table below shows, Royale usage was heavily skewed to older consumers and smaller households. Table 4 DEMOGRAPHIC CHARACTERISTICS BY BRAND Usual Brand Royale Kleenex Scotties Age Group 50 49 27 35 100 100 100 Household Size 16 10 8 42 32 35 42 58 57 100 100 100Pricing versus Kleenex In the past, when the number one SKU in the category was Kleenex 200s, feature price at retail on that product had been $0.99. Now, with the introduction of Kleenex 150s, feature price had dropped to $0.79, and sometimes lower in special promotions. In fact, in the past four months, average feature price for Kleenex had been $0.69, and for Royale $0.73. During this period, 80 per cent of the Royale sold at retail had been on feature. In the longer term, P&G estimated that the typical feature price for Kleenex 150s would be likely to increase modestly, but not dramatically. Furthermore, data from recent comparisons of Royale share at different levels of price disparity with Kleenex indicated higher price elasticity for Royale when its price exceeded Kleenex's by more than $0.20. Royale Price versus Kleenex ($) -0.10 0.0 +0.10 +0.20 +0.30 +0.40 Royale Market Share (%) 7.2 7.0 6.8 6.2 5.2 4.1 The Florelle Brand In 1991, 80 per cent of facial tissue units sold were standard two-ply tissue, the segment in which Facelle was represented by the Florelle brand. Specialty sizes (e.g., pocket packs, man-size, and cube format) represented eight per cent of units, and three-ply tissue about 12 per cent. The table below presents data from a November 1991 panel study of 2,215 households on their attitudes toward brands of facial tissue. Only three per cent of those surveyed claimed that Florelle was their usual brand. Not surprisingly for a brand which had received no advertising or consumer promotion, ratings of Florelle were not high. Table 5 BRAND ATTITUDES Past Three Months All Users Brand Users % Who Purchased in Average Average Past Three Months Average Brand Value Rating Overall Rating Overall Rating Florelle 53 58 10 73 Royale 71 78 30 85 Kleenex 73 80 75 82 Scotties 68 74 29 81 White Swan 61 66 14 77 Majesta 49 55 8 75 Store Brand 53 56 17 69Page 12 9A93A027 The obvious alternatives were to drop the Florelle brand, rejuvenate it with support, or continue it as an unsupported price brand. The Softness Issue A key success factor in the successful development of the Puffs brand in the United States was the effort that P&G invested in making the tissue softer. Softness is influenced by the process used in manufacturing the tissue, and the type of fibre employed. Longer fibres tend to make the resultant tissue stronger, but not as soft; shorter fibres, like eucalyptus, produce a softer tissue. A key issue in manufacturing facial tissue, therefore, is how the softness/strength tradeoff is managed. Data from P&G's experience in the U.S. market indicated that consumer preference as a function of strength followed an S-curve, where additional strength above the functional level did not provide any additional consumer benefit. On the other hand, softness did not level off in terms of diminishing returns on customer perceptions - at least at the levels of softness which could currently be obtained. Relative tissue strength depended upon the conditions of the test, especially whether the tissue was wet or dry. A given brand of tissue, which had much higher dry strength than a second brand, would not necessarily have much higher wet strength. Procter & Gamble believed that dry strength (which affected ease of dispensing the tissue) was much less important than wet strength (which directly affected consumers' use of the product). The data below show wet burst strength and softness for leading brands in the Canadian market. Softness was measured through tactile judgments of a panel of consumers, using Puffs as the standard zero-point on the scale. Table 6 SOFTNESS AND STRENGTH OF LEADING BRANDS OF FACIAL TISSUE Brand Softness' Wet Burst Strength (g/sheet) Royale 2.5 69 Florelle -2.1 32 Kleenex -1.1 31 Kleenex Ultra -0.5 76 Scotties -2.0 57 On this scale, Puffs tissues are rated at zero. Differences of 0.5 scale points or more are considered toCommenting on this data, Randall Beard said: This just reinforces what I have been told about Facelle's strategy prior to the acquisition. They chose to maximize strength particularly dry strength - but that approach cost them severely on the softness dimension. A study of customer dissatisfaction asked participants whether, in the past three months, they had experienced a problem with tissue breaking. Only one per cent of Royale users had experienced a problem, versus seven per cent of Kleenex users. In mid-1991, a blind paired comparison test was conducted with Royale and Kleenex Ultra. Attribute ratings on strength were the same for the two brands (8.5 on a 10-point scale), but Kleenex Ultra was rated significantly better on softness (9.1 versus 7.4). When asked which brand they preferred overall, only 27 per cent of participants chose Royale. Beard was convinced that P&G needed to upgrade the softness of the Facelle products. By adding eucalyptus fibre and sacrificing some tissue strength, their softness could be significantly improved without the need for a major capital expenditure. In the long run, investments in process improvement could produce further softness enhancements, but the so-called "Eucalyptus Upgrade" could be done in a few months for a modest investment. Accordingly, P&G carried out a pilot project to produce enough of the upgraded products for consumer acceptance testing. Early in 1992, "Single Product Blind Tests" (SPBT) were completed on the upgraded product, in both two-ply and three-ply form, as well as the current Royale, Florelle, Kleenex (Regular and Ultra), Scotties, and White Swan. In a SPBT, a sample of facial tissue with no identifying features is sent to a participant, who then uses the product for several weeks and answers a questionnaire about it. Participants in Facelle's SPBT were female heads of households whose first language was English. There were eight groups of participants, one for each brand. Group sizes ranged from 259 to 280 individuals. Results of this study are presented in Exhibit 7. Overall ratings of the brands were found to be a function of consumer impressions of a tissue's softness and its thickness. A multiple regression with these two independent variables explained more than 95 per cent of the variation in overall rating scores. The resultant equation is presented below: OVERALL RATING = 19.51 + (0.424 * SOFTNESS RATING) + (0.359 * THICKNESS RATING) One issue in introducing an upgraded tissue was its perception by current Royale and Kleenex users. Would a new two-ply product cannibalize sales of three-plyRoyale, or would it take share from Kleenex? Would a new three-ply product be seen as an improvement by users of the current Royale tissue? Exhibit 8 compares ratings of the upgraded products by users of Royale and Kleenex, respectively, with similar users' ratings of the existing Royale and Florelle products. It is noteworthy that current Royale users who received the two-ply upgrade in the SPBT were less favourably impressed with it than a group who actually received Royale in the blind test. In other words, the improved softness of the upgrade did not offset the reduction from three plies to two. The exhibit also enables a comparison of the group who received the three-ply upgrade with the one that received current Royale in the blind tests. In that situation, current Royale users rated the upgrade significantly higher on softness, slightly lower on strength and somewhat more favourably overall. If the two-ply upgrade were to be introduced, Randall Beard had to make a decision about what brand name would be used on it. Two apparent alternatives were Florelle (as an upgrade of the existing brand) and Royale (as a line extension). Furthermore, if the Royale name were chosen, a decision would have to be made about how to distinguish the two-ply upgrade from the three-ply upgrade of the traditional Royale brand. Another possibility would be to introduce the new product under the Puffs label that had been so successfully launched in the United States some 20 years earlier. Although Puffs had never been sold in Canada, there had been enough advertising spill-in from the United States that the brand was known to some Canadians. The table below shows data on the image of Puffs among English and French Canadians. Table 7 CANADIAN CONSUMER EVALUATIONS OF THE PUFFS BRAND English HHs French HHs Royale Puffs Royale Puffs % % Awareness 97 40 97 11 TV Adv. Awareness 36 18 33 3 Trial (past 12 mos.) 51 9 57 3 Overall Rating 82 57 84 37 Judgment of Value 66 48 72 39 Of Those Aware % agreeing that the 42 77 30 33 brand is good for nose carePage 15 9A93A027 CONCLUSION Using the Puffs label in Canada would be a step toward making Puffs a North American brand, an alternative which would certainly have the blessing of the U.S. parent. However, the primary responsibility for the decision rested with Randall Beard and Barbara Fraser, and the choice had to be made soon if product, packaging and advertising and merchandising programs were to be ready for the fall cold season. "This is the year that we have to begin our move to make Facelle a major player in the market," said Randall Beard to himself, "and there are a number of issues we must face. Our long-term goal is a profitable leading share of the market, which is a long way from where we are now. To get there, it is essential that we establish a winning strategy for the Facelle Division brands." To do so, Beard felt, several inter-related questions had to be answered. What should be done about the Florelle brand? Should available technology from P&G be employed to increase the softness of Royale? What should be the position of the Facelle brand in the two- ply segment? In fact, what brand should Facelle employ in that segment - and Puffs, or an altogether new brand?Page 16 9A93A027 Exhibit 1 TYPICAL COST STRUCTURE: FACIAL TISSUE IN CANADA Cost per Case of 48 Units of 150-count two-ply tissue Net Revenue $54 Off-invoice Allowance $91 Co-op Allowance 102 Less: Total Discounts and Allowance 19 Net Sales 35 Less: Variable Manufacturing Cost (Including Delivery) 16 Contribution 19 Manufacturing Fixed Cost 11 Selling, Research, & Administration Marketing Support* Less: Total Fixed Costs 15 Profit $ 4 "Average price reduction through the year, assuming feature price reductions of 25 per cent were given on approximately two-thirds of the unit volume. "Allowance for co-operative advertising and promotion. Some of these funds were actually used by retailers for this purpose, and the rest was retained by them. 'In March 1992, about 55 per cent of the variable manufacturing cost of facial tissue was the cost of wood pulp. As a result, here was a substantial difference in profitability between the Florelle and Royale brands. "Advertising, couponing, sampling. For many of the existing brands, less than $1 per case was spent on advertising support.Page 17 9A93A027 Exhibit 2 EXAMPLE OF KLEENEX 150s AD KLEENEX TISSUES Feb 17/91 523-03 CBUT 30 seconds Vancouver Kleenex Softer Than Ever! (Music throughout) think of new softer Kleenex BABY 1: I been waitin', ANNCR(VO) : What do the Tissues. waitin' so long... experts BABY 2 6 3: Bee-doo- BABY 4: ...for you to BABY 2 6 3: ...bee-doo- bee-doo. . . come along. bec-doo. . . BABY 5: Softer. ANNCR(VO) : New Kleenex are even softer now. Tissues Made with soft natural They're baby soft. BABY 3:...bee-doo-bee. ..Page 18 9A93A027 Exhibit 2 (continued) KLEENEX TISSUES Feb 17/91 523-03 CBUT 30 seconds Vancouver Softer Than Ever! BABY 3: ...come softly... BABY 4: .. .darling. SINGERS: Softer than ever . BABY 5: Softer. BABY 2 6 3: Da-bee-doo.. . . (Fades out)Page 19 9A93A027 Exhibit 3 EXAMPLE OF KLEENEX ULTRA AD Kleenex Ultra Tissues : Lotion Bottle 30 seconds WITH LOTNI Wha Anner (VO) : Kleenex Ultra So it feels soft and soothing tissues with lotion. WITH LOTION Ulta on even the sorest nose. Kleenex Ultra Softer, because it has lotion.THE PROCTER & GAMBLE COMPANY Procter & Gamble originated in 1837, when William Procter and James Gamble, two immigrant soap and candle makers, formed a partnership in Cincinnati, Ohio. The partnership rapidly flourished, gaining a name as a principled manufacturer of high quality consumer goods sold at competitive prices. The Procter & Gamble Company was incorporated in 1890, and in every decade since incorporation, sales more than doubled. By 1992, P&G was a multinational company with annual sales of almost US$30 billion, profits exceeding US$1.8 billion, and a long-standing reputation for quality products, high integrity, strong marketing, and conservative management. As Procter & Gamble grew, it increasingly focused on international markets. In 1992, P&G's brands were sold in more than 140 countries around the world. Major areas and representative brands included laundry and cleaning products (e.g., Tide, Cheer, Mr. Clean), paper products (Pampers, Luvs, Always, Bounty, Charmin), health care (Pepto-Bismol, Metamucil), oral care (Crest, Scope), food and beverage (Jif, Crisco), bar soaps (Ivory, Zest) and cosmetics (Oil Of Olay, Max Factor, Cover Girl). Many of these brands were leaders in their categories. In Canada, P&G operated as Procter & Gamble Inc., with 1992 sales expected to exceed $1.7 billion, and earnings before taxes of over $100 million. P&G Inc. operated as four divisions, of which Paper Products was one, organized on a category basis within each division (e.g., Tissue/Towel/Facial within Paper Products). Procter & Gamble in Paper Products Procter & Gamble first entered the consumer paper market in 1957 with its acquisition of Charmin Paper Company, a regional company with a strong presence in the north central United States. In the early 1960s, P&G developed proprietary papermaking technologies which allowed it to deliver softness, strength and absorbency that were superior to conventionally manufactured products. This technology was used to strengthen the Charmin toilet tissue brand, leading to national expansion in the mid-1960s. Simultaneously, P&G launched Bounty towels, also employing the new technology, and subsequently expanded the brand to national distribution in 1972. Finally, P&G entered the facial tissue market in the early 1970s by launching the Puffs brand, which was initially sold as a regional brand, then expanded to the national market in 1990. P&G built Charmin, Bounty and Puffs with similar strategies. First, proprietary technology was used to deliver products with superior performance at a competitive price. As well, consumers were offered "value-added" products which delivered additional benefits (e.g., Puffs Plus with lotion, Charmin Free with noPage 20 9A93A027 Exhibit 4 EXAMPLE OF SCOTTIES AD That may responded with Scotties Recycled. It still has sound like a far- that famous Scotties softness you've come to fetched notion. depend on. only now it's made from more than but in reality it could two thirds recycled paper. happen. That's because consumers like you Which makes Scotties Scotties wanted a facial tissue safe for the environment. Recycled the natural ver soft enough for their skin. Scott Paper choice for softness RECYCLED The Same Tissue That's Pampering Your Cold This Year, Just Might Have Been A Get Well Card Last Year.Exhibit 5 ADVERTISING STRATEGY OF FACIAL TISSUE COMPETITORS A. Copy Strategy Brand Years Copy Strategy - Execution Medium Kleenex 1980-1988 Heritage - family moments TV, Print New packaging - pack shot Print 1989-1991 Improved softness TV Lotion - demonstration TV, Print, OOH' Scotties 1967-1989 Softest cold care - "Scotties soften TV the blow" 1990 Caring softness - "Softer than a kiss" TV 1991 Environmentally friendly Print, OOH Royale 1973-1986 Superior cold care - three-ply TV softness and strength 1988-1990 New packaging OOH 1991 "Kitteny soft" TV 1992 Superior cold care - three-ply TV demonstration 'OOH indicates advertising message delivered Outside Of Home (e.g., through billboards or mass transit advertising). B. Share of Advertising Expenditure Brand Share of Advertising Spending 1988 1989 1990 1991 Royale 25% 52% 49% 16% Kleenex 2% 35% 15% 18% Kleenex Ultra 21% Scotties 50% 13% 25% 33% White Swan 3% 10% 6% Majesta 1% 6% Other 20% TOTAL 100% 100% 100% 100%Page 22 9A93A027 Exhibit 6 BRAND IMAGES BY ATTRIBUTE Brand Rating Attribute Royale Kleenex Scotties Store Brands . is soft C good for sore nose care I O does not tear or fall apart when I + O O blow my nose or sneeze . is absorbent + - O is thick + - I contains lotion 0 + . is three-ply + . design/colours on box are attractive + + I O is caring O O is fashionable - + - O O . is contemporary O is inexpensive + "In this chart, 0 represents a score that was not different from the average rating for all brands, - a score that was lower than the average rating, and + a score that was higher.Page 23 9A93A027 Exhibit 7 CONSUMER EVALUATIONS OF FACIAL TISSUES IN SPBT' Brand Overall' Softness Strength Thickness Absorbency Facelle Royale: . current 823 78 91 87 85 . three-ply upgrade 88 93 90 87 85 Florelle: . current 73 70 74 68 70 . two-ply upgrade 80 89 73 72 75 Kleenex Regular 75 82 68 65 71 Ultra 90 94 89 87 86 Scott Scotties 63 58 66 58 63 White Swan 62 50 74 63 65 'Ratings of English-speaking female heads of household, on a scale of 0-100 based on a single product blind test (SPBT) in home. Each respondent was asked: "Considering everything about the facial tissue sent to you, how would you rate it OVERALL?" "For this sample size, differences of more than five scale points across groups (Le., within a column in the table) are significant at the 0.05 level9A93A027 Page 24 Exhibit 8 SPBT' RATINGS OF CURRENT FACELLE PRODUCTS AND THE UPGRADES Users of Royale Users of Kleenex in Past Three Months in Past Three Months Attribute 3-ply Current 2-ply Current 3-ply Current 2-ply Current Ratings Upgrade Royale Upgrade Florelle Upgrade Royale Upgrade | Florelle 83 77 72 89 81 80 74 Overall 90 Softness 94 77 89 72 93 76 90 70 76 Strength 89 83 68 72 90 91 74 88 68 63 88 86 72 69 Thickness 90 Absorbency 87 85 74 69 86 84 75 71 "Single Product Blind Test ratings. Each column in the table represents ratings by a group who received the indicated product in a blind test. Differences across columns of six scale points or more are statistically significant at the 0.05 level.inks, dyes or perfumes). Third, the brands were supported with successful advertising themes and consistently high media weights. Finally, P&G achieved competitive costs among premium brands by using Total Quality Methods to improve the papermaking process. Together, these strategies were extremely successful. Charmin and Bounty established clear market share leadership in their categories, with Puffs a close second (to Kimberly-Clark's Kleenex brand) in the facial tissue category. The Facelle Acquisition By 1991, P&G was sufficiently satisfied with its U.S. successes on Charmin, Bounty and Puffs that it was ready to take its first step in expanding the business. Canada was the logical first choice for that step, given its proximity to the United States, the advent of free trade between Canada and the United States, and the attendant opportunities for North American supply sourcing. At the time, P&G had only one paper plant in Canada, which manufactured diapers in Belleville, Ontario. Early in 1991, an attractive acquisition opportunity developed for P&G. Canadian Pacific Forest Product Company, a large diversified paper company, was prepared to sell Facelle Paper Products, its tissue division. Facelle was a medium-sized manufacturer and marketer of tissue, towel and sanitary products, headquartered in Toronto. In 1990, Facelle reported an operating profit of $13.4 million on sales of $170.5 million. The deal was concluded in August 1991; for $185 million, P&G bought the Facelle Co., its plant in Toronto, and its franchise for facial tissue, paper towels and bathroom tissue, including the Royale, Florelle, Pronto, Dove, Facettes, and Festival brands. THE CONSUMER PAPER BUSINESS IN CANADA The Canadian consumer paper market in 1992 was about 25 million cases, where a case represented a shipping unit of approximately equivalent size for the three principal types of tissue. In the facial tissue category, a case contained the equivalent of 48 boxes of 150 two-ply tissues. Of the 25 million cases, bathroom tissue accounted for 13 million, paper towels seven million, and facial tissue five million. Tissue products were inexpensive (usually less than $2.00 per package), they were widely used (in more than 95 per cent of Canadian households), and they were frequently purchased (on average, once every two weeks). Brand switching was high, as there were many acceptable substitutes and the risk associated with product failure was low. The challenge for manufacturers was to differentiate their products enough on performance to build loyalty.m Retailing Not surprisingly, retailers viewed paper as a low-prot, low-loyalty category, and they used it primarily to draw consumers into their stores. Traditional food stores typically canied a full line of paper products and featured them frequently. in recent years, however, mass merchandiser and drug chains had expanded their paper business substantially, focusing almost exclusively on price deals to attract customers to their stores. Recently, \"club stores,\" with their emphasis on everyday low pricing, further squeezed retail and manufacturer margins. The vigorous retail competition had led to heavy featuring, where some brand was on sale virtually every week of the year, with resultant low prot margins. The challenge for manufacturers was to convince retailers to use their brands as the key feature items while trying to nd ways to help retailers build prot. Furthermore, many retailers had moved to a \"bidding\" process that allocated featut't-'d promotions to the. manufacturer with the most lucrative retail spending program. Manufacturing The paper business in Canada had a few very large national manufacturers and a few smaller regional players. This structure was driven, in part, by the sizable scale efficiencies that had been achieved in papermalcing. Therefore, the industry was characterized by high capital and xed costs. A single paper machine cost at least US$100 million, and at capacity it could satisfy about. 10 per cent of the Canadian market. A cost structure that Beard could envision for a national manufacturer competing aggressively in the facial tissue market is presented in Exhibit 1, based on the cost Information presented above. Over half of the variable manufacturing cost of facial tissue was the cost of wood pulp. This cost structure, combined with the consumer and retail customer behaviours described above, strongly encouraged paper manufacturers to run their machines near capacity to maximize their contribution. Thus, most manufacturers marketed broad product lines in an attempt to compete in all segments of the market and utilize as much capacity as possible. Also, they competed intensely for the product features which drove volume at the retail level. It was common in the industry for one manufacturer to market both premium and price brands in all three of the Tissue, Towel and Facial categories, to supply retailers with private label products in the same categories, and to sell to theconuncrcial and_in:stituti_op'al marketsas well "' ' ' - ' THE FACIAL TISSUE MARKET IN CANADA The largest players in the Canadian consumer paper business were Scott Paper and Kimberly-Clark, both subsidiaries of successful large U.S. paper companies. In addition, there were several small regional players, of whom the largest was Irving Paper, operating in the Maritimes. The size of the facial tissue market in 1991 was 4,894,000 cases shipped, up seven per cent over 1990 sales. Market shares of the major producers, indexed to 1990 shares, are presented in Table 1. They will be discussed in the following paragraphs. Table 1 FACIAL TISSUE MARKET SHARES - 1991 Percentage Total P&G Share of 1991 Index vs. Company/Brand Shipments 1990 Shares Royale 6.9 1011 Florelle 5.8 67 Total P&G 12.7 84 Kimberly-Clark 39.5 107 Scott 23.0 88 Irving 4.2 n.a. All Others 20.6 98 100.0 'Index = (1991 share) / (1990 share) * 100. For example, the Royale index of 101 was calculated by dividing Royale's 1991 market share of 6.9 per cent by their share of 6.8 per cent in 1990. "In data throughout the case, Florelle numbers will include the Facettes brand. Facettes was a minor price brand. Brand Developments in 1991 Facelle Brands Shipments of the Facelle brands of facial tissue in 1991 were only 622,000 cases, or 84 per cent of the 1990 results. Two brands, Royale and Florelle, accounted for most of Facelle's sales. Florelle and Royale were made from the same base tissue stock, with Royale having three layers or plys, while Florelle had only two. Until recently, the Royale brand had been the only three-ply tissue on the market, and it enjoyed a brand image as the traditional, strong, premium quality facial tissue. Its market share increased very slightly during 1991. Florelle was a two-ply tissue that had received little promotional attention. Not surprisingly, it had low awareness, trial and image. It had lost about one-third of its market share in 1991, down to 5.8 per cent.Kimberly-Clark. The Kleenex brand had enjoyed a very good year in 1991, gaining 2.5 share points to reach 39.5 per cent of units shipped in the Canadian market. In fact, Kleenex's share reached 41.7 per cent in the second half of the year. For several years in the late 1980s, Kimberly-Clark had made no significant changes in the Kleenex brand. However, there were several Kleenex product initiatives during 1991 which affected the brand's sales results. The new 300-tissue family size (two-ply) package, which had first been introduced in September 1989, had completed its national rollout in 1991; it achieved a share for the year of 8.2 per cent, up from 3.1 per cent in 1990. Also, the rollout of the two-ply Kleenex 150, which replaced Kleenex 200s as the number one stockkeeping unit (SKU) in the facial tissue category, was completed in 1991. Largely in support of this latter introduction, Kimberly-Clark increased merchandising support by 20 per cent in food retailers and 13 per cent in drug retailers. Finally, Kimberly-Clark introduced Kleenex Ultra, a three-ply tissue which contained a silicone-based lotion, in the Ontario market in mid-1991. (Exhibits 2 and 3 show advertisements for Kleenex 150s and Ultra.) Scott. Scott's major brand, Scotties, fell from a share of 18.9 per cent in 1990 to 15.9 per cent in 1991. The main reason for the decline was the loss of trade support relative to Kleenex 150s. Scott relaunched the brand in September 1991, positioning it as a product with high content of recycled material, and supporting it with heavy advertising. (See Exhibit 4 for an example of Scotties' advertising.) As well, a 300-tissue family size of Scotties was launched in December 1991. Early indications were that the brand was recovering. Scott's secondary brand, White Swan (sold only in 150s), maintained a 7.1 per cent share in 1991. Increased merchandising in drug channels led to a share gain there, which compensated for the share loss in food channels in the face of Kleenex 150s with its stronger brand image. Irving. Next to the aggressive developments in the Kleenex brand, the most significant competitive event in the facial tissue business in 1991 was the entry of Irving into the facial tissue market in the Maritime provinces and Quebec with its new Majesta brand. Majesta was packaged in an attractive format, and its feature pricing averaged 15 to 20 per cent below Kleenex. It achieved a 4.2 per cent national share in 1991. All Others. Overall, the other brands in the Canadian marketplace retained 98 per cent of their cumulative market share in 1991. The group suffered some losses in the face of the merchandising support of Kleenex 150s, but these were balanced by gains in private label products in Western Canada.Advertising Advertising expenditures in the facial tissue category had historically been low, and quite inconsistent in "share of voice" and medium by manufacturer. Average industry annual expenditures were nearly $3.0 million over the last five years, with television accounting for 47 per cent of spending, "out-of-home" (i.e., billboards, posters, and mass transit ads) 32 per cent, consumer magazines 17 per cent and daily newspapers four per cent. Exhibit 5 summarizes copy and media strategy for the major brands in recent years, and share of advertising expenditures by brand. Randall Beard believed that Kimberly-Clark had established a contemporary image for the Kleenex brand, but not a strong image for either softness or tissue strength. There had been no brand equity advertising' on the softness theme for the Kleenex brand since 1979, although there had been introductory campaigns for the softness upgrades to the basic product in 1989 and 1991, and the launch of the lotion line extension Kleenex Ultra in 1991. Until the past year, when all Scotties' advertising was focused on the recycled paper relaunch behind an environmentally friendly position, Scotties had consistently advertised softness. This was somewhat ironic, because, according to P&G's tests of softness, the Scotties product was inferior on that dimension. Royale had historically focused on the superior cold care afforded by the softness and strength of the three-ply tissue. In 1991, ads for the product had emphasized softness, followed at year-end by the tactical cold season airing of an existing cold care execution. By Procter & Gamble standards, advertising in the facial tissue category had not been strong. Not only were expenditures low, but only a small proportion of that spending was on brand equity. Furthermore, campaigns in the industry had tended to be of short duration, while P&G's extensive research on consumer advertising indicated that to be effective, advertising had to be sustained. Consumer Promotion Except for the Facelle brands, there was little consumer promotion activity in the category, relative to the norms for other consumer packaged goods. In 1991, the three major facial tissue suppliers ran a total of 35 consumer promotions, with 21 of those for the Facelle brands (13 for Royale and eight for Florelle, respectively). Of the 35 promotions, 19 were coupons, and the other 16 a variety of sweepstakes, mail-in offers, samples, and cross-coupons. Altogether, P&G estimated, the 19 coupon promotions moved an incremental 42,000 cases of product for the threePage 8 9A93A027 brands, or less than one per cent of facial tissue shipments. In general, promotions did not pay for themselves because of the low absolute unit price of the product relative to the cost of the promotion. Therefore, promotions were likely to be used only as part of a more efficient group promotion, or as part of a strategy specifically directed at obtaining trial. Pricing While consumer promotions for facial tissues were relatively rare, price features were commonplace. There was always at least one brand on feature at any sizeable food or drug retailer. In fact, the vast majority of facial tissues sold at retail during 1991 were feature-priced. Typical prices for the major brands during 1991 are shown below. Table 2 TYPICAL PRICES - 1991 Typical Typical Brand Ply Count Shelf Price Feature Price P&G Royale 100 1.19 0.89 Florelle 200 1.09 0.79 Kimberley-Clark Kleenex 150 0.99 0.79 Kleenex WNN 300 1.99 1.59 Kleenex-Ultra 100 0.99 0.79 Scott Scotties 150 0.99 0.69 Scotties NNN 300 1.99 1.49 White Swan 150 0.89 0.59 Irving Majesta 150 0.89 0.63 Private Labels 2 150 0.79 0.49Page 9 BABSADZT ISSUES FOR THE FAUELLE BRAND In planning the future of the Facelle brands, several problems had to be confronted. But rst, Randall Beard reviewed a summary of the research which Per had obtained in the seven months since acquiring the Facelle business. The Royals Brand Brand Imagg Royale's longterm premium positioning, based upon its historically unique three ply product design and its softness claim, had built the leading brand image among its users in the product category. In judgments by a brand's users, Royale received an overall score of 35 on a scale of l. marginally superior to Kleenex [at an average score of 82) and Seotties {E l), and considerably ahead of the store brands (averaging 69]. Exhibit E compares four leading brands on a number of specic attributes of image. Royale enjoyed an image advantage for strength and thickness versus all other competition, but an image weakness for package design. Furthermore, it was seen as less fashionable than Kleenex and Scotties. The image data were particularly interesting to Beard and his product managers; despite low advertising spending in the category, historic campaigns appeared to have had a strong impact on brand image. For example, Scotties had a strong image for softness despite clearly inferior physical characteristics on that dimension relative to Royals and Kleenex. Almost ll} years of advertising using the Little Soie character and the message \"Scotties softens the blow" had evidently produced a strong image for the brand as a soft, gentle tissue that was good for sore nose care. Although Royale enjoyed a very favourable overall brand image, knowledge about the brand was not as high as Beard would have expected. For instance, among those who had used it in the past three months. 4? per cent thought that Royale was a two-ply tissue, and only 43 per cent correctly assessed it as three-ply. Product sa e Although Royale enjoyed a very favourable overall brand image, that image did not translate to market share, as the table below demonstrates. Although half of households had used Royale sometime in the last year, only 14 per cent claimed that it was their usual brand over the past three months. Qualitative research indicated that Royale was used as a part-time brand that was bought on feature or specically for cold care, but seldom for regular usage around the household. This pattern was conrmed by the image data which showed signicantly less agreement with the statement \"is inexpensive" for Royale {32 per cent} than Kleenex {52 per cent}, Scotties [42 per cent}, or store brands [83 per cent}

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance