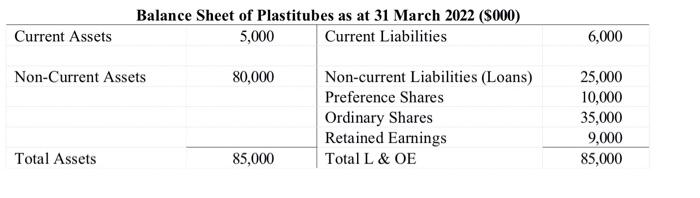

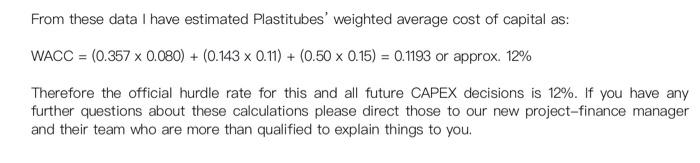

Plastitubes is a medium sized company listed on the NZX and has 35 million shares on issue the current share price is $2.50. In addition, Plastitubes issued 10 million preference shares 5 years ago. These preference shares have a $1 face value and a fixed dividend of 11%p.a. The preference shares are currently trading at $1.75 each. The company's equity beta (B) is 1.30, the New Zealand market risk premium is estimated at 6.0% p.a., the yield on 10-year New Zealand government bonds is 2.30% p.a., and the company tax rate is 28%. The company's long-term debt consists entirely of 25,000 10-year bonds issued exactly 4 years ago (these are listed on NZDX). Each bond has a face value of $1,000 and an annual coupon rate of 8% (paid annually). The bonds are currently trading at a yield to maturity of 6% p.a. Extracts from Plastitubes' latest financial statements show the following: Balance Sheet of Plastitubes as at 31 March 2022 (S000) 5,000 Current Liabilities 80,000 Non-current Liabilities (Loans) Preference Shares Ordinary Shares Retained Earnings 85,000 Total L & OE Current Assets Non-Current Assets Total Assets 6,000 25,000 10,000 35,000 9,000 85,000 Your project-finance team has just received a memo (see following page) from the company's Chief Executive Officer, Freddy May, and you have decided you all need to prepare thoroughly for any questions that might arise from your colleagues in the meeting mentioned in the memo. On first glance you are a little concerned with some of the CEO's calculations and feel you might have to talk briefly with Mr May before the meeting as well. TASKS: a) Prepare and submit your own detailed calculation of Plastitubes' WACC. (Round your final answer up to the nearest %). (20 marks) b) Clearly identify all parts of your calculations that differ from Mr. May's and thoroughly explain/justify your assumptions and calculations. (10 marks) Memo To: All Finance Staff From: Freddy May - CEO Date: 9 May 2022 Re: Capital Expenditure As you know, Plastitubes evaluates Capital Expenditure decisions using discounted cash-flows. The discount, or hurdle, rate is our company's weighted average cost of capital. This memo is to clarify our company's long-standing policy regarding hurdle rates for these investment decisions. Plastitubes is considering an investment in a new FRP Filament Winder that will improve the quality and reliability of our manufacturing processes, simultaneously eliminating a significant proportion of our variable costs. In case you're unaware, filament winding is the process of winding resin- impregnated fibre on a mandrel surface in a precise geometric pattern. This is accomplished by rotating the mandrel while a delivery head, under computer control, precisely positions continuous strands of fibres on the mandrel surface. Compared to our existing, labour intensive, manufacturing process this investment should provide us with significant advantages however, it does also significantly increases the company's operating leverage. Our target rate of return on equity has been 15% for many years. I realise that many new employees feel that this target is too high but I feel we need to aim for the highest profitability we can in order to keep our shareholders as happy as possible. The following table summarises the composition of Plastitubes' financing: Bonds Preference Shares Ordinary Shares Amount ($000) 25,000 10,000 35,000 % of total 35.7% 14.3% 50.0% Rate 8.00% 11.0% 15.0% From these data I have estimated Plastitubes' weighted average cost of capital as: WACC = (0.357 x 0.080) + (0.143 x 0.11)+ (0.50 x 0.15)= 0.1193 or approx. 12% Therefore the official hurdle rate for this and all future CAPEX decisions is 12%. If you have any further questions about these calculations please direct those to our new project-finance manager and their team who are more than qualified to explain things to you. Plastitubes is a medium sized company listed on the NZX and has 35 million shares on issue the current share price is $2.50. In addition, Plastitubes issued 10 million preference shares 5 years ago. These preference shares have a $1 face value and a fixed dividend of 11%p.a. The preference shares are currently trading at $1.75 each. The company's equity beta (B) is 1.30, the New Zealand market risk premium is estimated at 6.0% p.a., the yield on 10-year New Zealand government bonds is 2.30% p.a., and the company tax rate is 28%. The company's long-term debt consists entirely of 25,000 10-year bonds issued exactly 4 years ago (these are listed on NZDX). Each bond has a face value of $1,000 and an annual coupon rate of 8% (paid annually). The bonds are currently trading at a yield to maturity of 6% p.a. Extracts from Plastitubes' latest financial statements show the following: Balance Sheet of Plastitubes as at 31 March 2022 (S000) 5,000 Current Liabilities 80,000 Non-current Liabilities (Loans) Preference Shares Ordinary Shares Retained Earnings 85,000 Total L & OE Current Assets Non-Current Assets Total Assets 6,000 25,000 10,000 35,000 9,000 85,000 Your project-finance team has just received a memo (see following page) from the company's Chief Executive Officer, Freddy May, and you have decided you all need to prepare thoroughly for any questions that might arise from your colleagues in the meeting mentioned in the memo. On first glance you are a little concerned with some of the CEO's calculations and feel you might have to talk briefly with Mr May before the meeting as well. TASKS: a) Prepare and submit your own detailed calculation of Plastitubes' WACC. (Round your final answer up to the nearest %). (20 marks) b) Clearly identify all parts of your calculations that differ from Mr. May's and thoroughly explain/justify your assumptions and calculations. (10 marks) Memo To: All Finance Staff From: Freddy May - CEO Date: 9 May 2022 Re: Capital Expenditure As you know, Plastitubes evaluates Capital Expenditure decisions using discounted cash-flows. The discount, or hurdle, rate is our company's weighted average cost of capital. This memo is to clarify our company's long-standing policy regarding hurdle rates for these investment decisions. Plastitubes is considering an investment in a new FRP Filament Winder that will improve the quality and reliability of our manufacturing processes, simultaneously eliminating a significant proportion of our variable costs. In case you're unaware, filament winding is the process of winding resin- impregnated fibre on a mandrel surface in a precise geometric pattern. This is accomplished by rotating the mandrel while a delivery head, under computer control, precisely positions continuous strands of fibres on the mandrel surface. Compared to our existing, labour intensive, manufacturing process this investment should provide us with significant advantages however, it does also significantly increases the company's operating leverage. Our target rate of return on equity has been 15% for many years. I realise that many new employees feel that this target is too high but I feel we need to aim for the highest profitability we can in order to keep our shareholders as happy as possible. The following table summarises the composition of Plastitubes' financing: Bonds Preference Shares Ordinary Shares Amount ($000) 25,000 10,000 35,000 % of total 35.7% 14.3% 50.0% Rate 8.00% 11.0% 15.0% From these data I have estimated Plastitubes' weighted average cost of capital as: WACC = (0.357 x 0.080) + (0.143 x 0.11)+ (0.50 x 0.15)= 0.1193 or approx. 12% Therefore the official hurdle rate for this and all future CAPEX decisions is 12%. If you have any further questions about these calculations please direct those to our new project-finance manager and their team who are more than qualified to explain things to you