Answered step by step

Verified Expert Solution

Question

1 Approved Answer

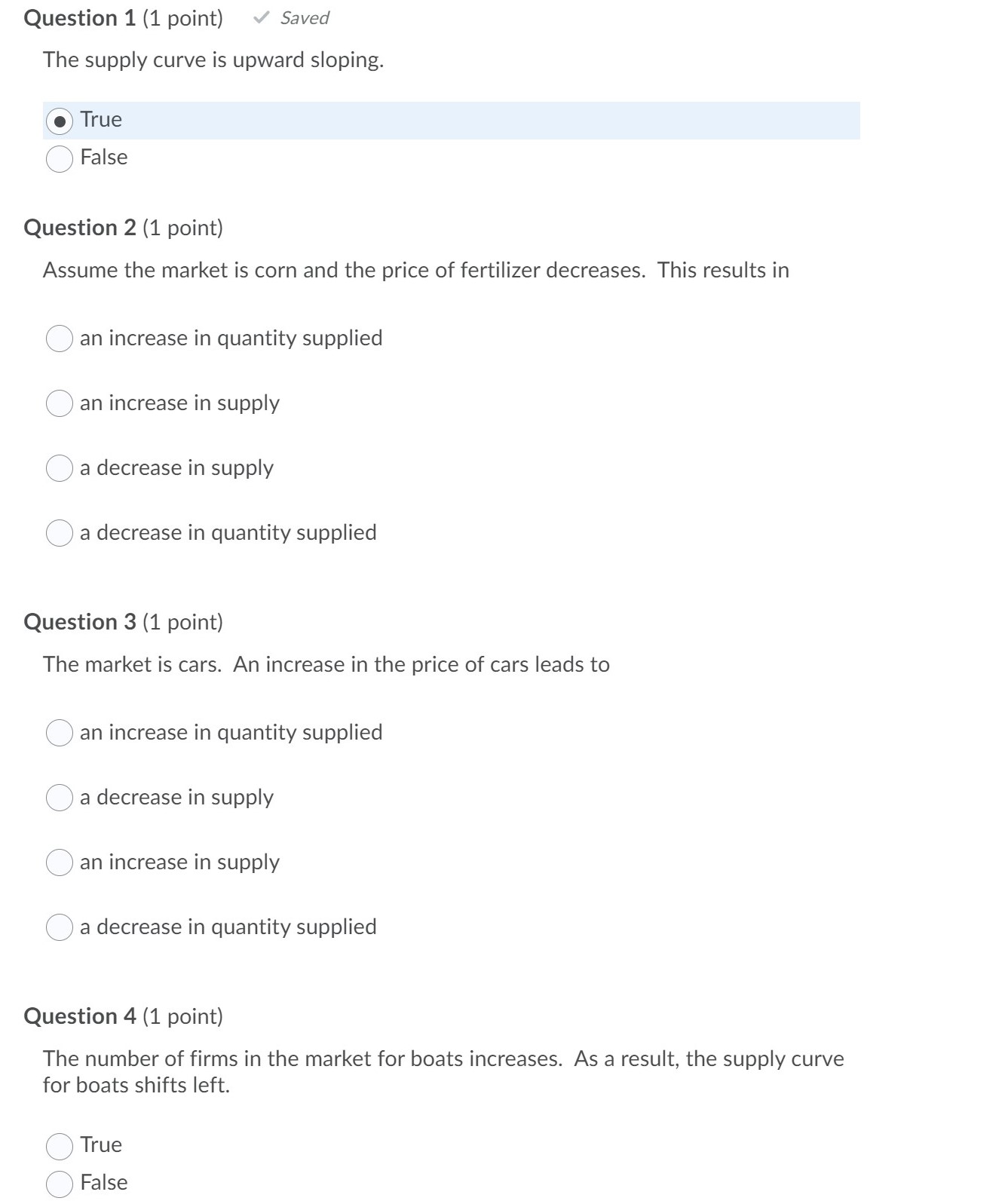

Please Ans All questions Correctly Question 1 (1 point) ~/ Saved The supply curve is upward sloping. Question 2 (1 point) Assume the market is

Please Ans All questions Correctly

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Worldly Philosophers The Lives, Times And Ideas Of The Great Economic Thinkers

Authors: Robert L Heilbroner

7th Edition

068486214X, 9780684862149