Answered step by step

Verified Expert Solution

Question

1 Approved Answer

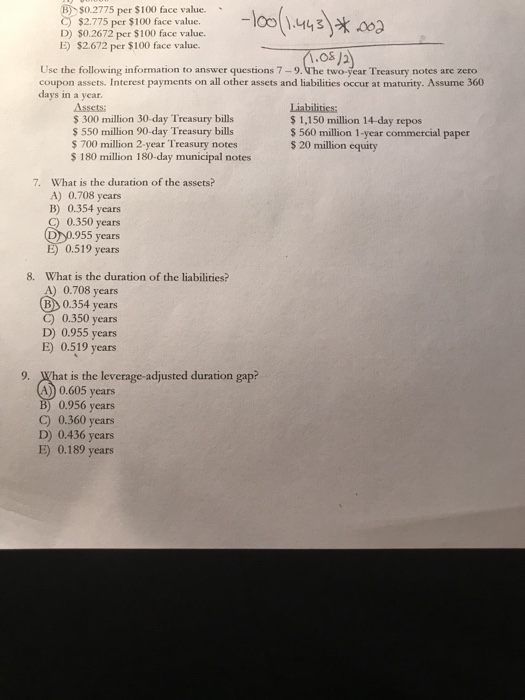

please anser the following questions and show all work, thanks! B)$0.2775 per $100 face value. C) $2.775 per $100 face value. D) 50.2672 per $100

please anser the following questions and show all work, thanks!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Asymptotic Chaos Expansions In Finance Theory And Practice

Authors: David Nicolay

2014 Edition

1447165055, 9781447165057