Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer 1, 3, & 4 1. The Wall Street Journal reports that the rate on three-year Treasury securities is 7.15 percent and the rate

Please answer 1, 3, & 4

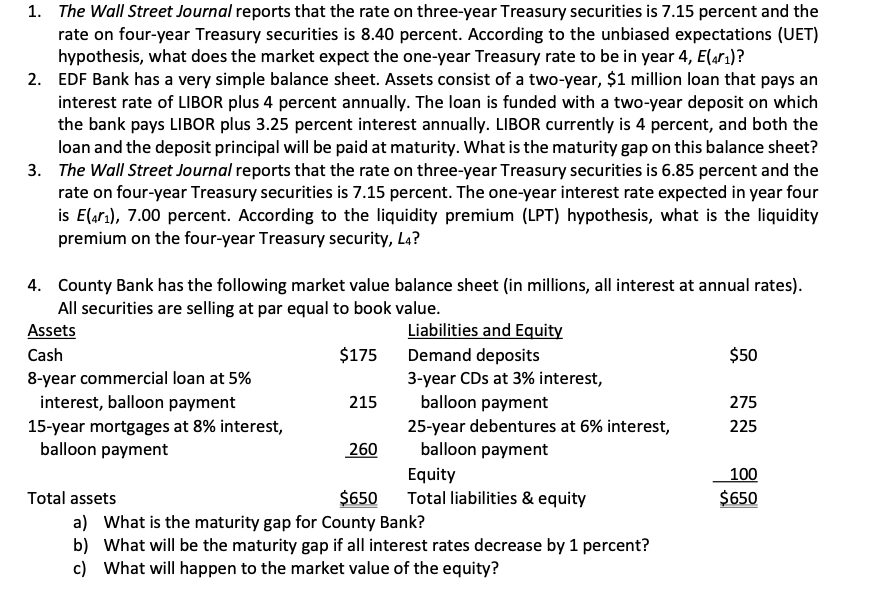

1. The Wall Street Journal reports that the rate on three-year Treasury securities is 7.15 percent and the rate on four-year Treasury securities is 8.40 percent. According to the unbiased expectations (UET) hypothesis, what does the market expect the one-year Treasury rate to be in year 4,E(4r1) ? 2. EDF Bank has a very simple balance sheet. Assets consist of a two-year, \$1 million loan that pays an interest rate of LIBOR plus 4 percent annually. The loan is funded with a two-year deposit on which the bank pays LIBOR plus 3.25 percent interest annually. LIBOR currently is 4 percent, and both the loan and the deposit principal will be paid at maturity. What is the maturity gap on this balance sheet? 3. The Wall Street Journal reports that the rate on three-year Treasury securities is 6.85 percent and the rate on four-year Treasury securities is 7.15 percent. The one-year interest rate expected in year four is E(4r1),7.00 percent. According to the liquidity premium (LPT) hypothesis, what is the liquidity premium on the four-year Treasury security, L4 ? 4. County Bank has the following market value balance sheet (in millions, all interest at annual rates). All securities are selling at par equal to book value. b) What will be the maturity gap if all interest rates decrease by 1 percent? c) What will happen to the market value of the equity? 1. The Wall Street Journal reports that the rate on three-year Treasury securities is 7.15 percent and the rate on four-year Treasury securities is 8.40 percent. According to the unbiased expectations (UET) hypothesis, what does the market expect the one-year Treasury rate to be in year 4,E(4r1) ? 2. EDF Bank has a very simple balance sheet. Assets consist of a two-year, \$1 million loan that pays an interest rate of LIBOR plus 4 percent annually. The loan is funded with a two-year deposit on which the bank pays LIBOR plus 3.25 percent interest annually. LIBOR currently is 4 percent, and both the loan and the deposit principal will be paid at maturity. What is the maturity gap on this balance sheet? 3. The Wall Street Journal reports that the rate on three-year Treasury securities is 6.85 percent and the rate on four-year Treasury securities is 7.15 percent. The one-year interest rate expected in year four is E(4r1),7.00 percent. According to the liquidity premium (LPT) hypothesis, what is the liquidity premium on the four-year Treasury security, L4 ? 4. County Bank has the following market value balance sheet (in millions, all interest at annual rates). All securities are selling at par equal to book value. b) What will be the maturity gap if all interest rates decrease by 1 percent? c) What will happen to the market value of the equityStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Pillars Of Finance The Misalignment Of Finance Theory And Investment Practice

Authors: G. Fraser-Sampson

2014th Edition

1137264055, 978-1137264053