Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer 2-3-4-5.questions. thanks TIME VALUE OF MONEY: A HOME INVESTMENT DECISION DILEMMA In early 2016, Naresh Jain, a tax consultant based out of North

Please answer 2-3-4-5.questions. thanks

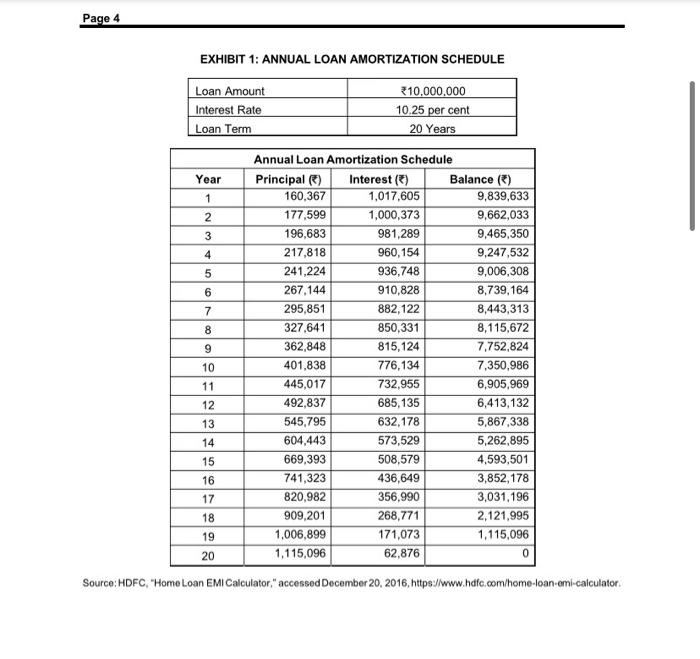

TIME VALUE OF MONEY: A HOME INVESTMENT DECISION DILEMMA In early 2016, Naresh Jain, a tax consultant based out of North West Delhi, India, was hurriedly looking at rental properties on a popular real estate listing website. His rental agreement with his landlord had ended the day before, leaving him 30 days to prepare to vacate the apartment and look for a new one. Jain had lived in the spacious, two-bedroom apartment in North West Delhi for the past five years as it was within a reasonable commuting distance to his workplace. However, because of a sudden downturn in business conditions and an immediate need for money, his landlord wanted to sell the property and therefore had asked Jain to vacate the premises. After a busy day looking online at various rental properties, Jain had come across a furnished apartment next door that was identical to his. Like his apartment, it had two bedrooms, two bathrooms, a spacious hall, and a state-of-the-art kitchen. Jain's initial enquiries to the property broker revealed that it would likely be rented at around 30,000 per month, including parking facilities. This was well in line with the rent he was currently paying, and Jain decided to go ahead and meet the broker. During his meeting with the broker, Jain learned that an identical apartment in an adjoining locality was for sale for 12.5 million. The flat was very well furnished and had all the amenities that Jain was looking for. Jain had a lot of quantitative thinking to do as he considered the alternatives of renting versus buying an apartment. How would he finance the home in the case that he decided to buy? What would the monthly mortgage payments be in the case that he took out a loan to buy the home) to buy the apartment, compared to renting it? How would he incorporate the opportunity cost and taxation aspect in his calculations? Most importantly, given the state of the real estate market in India, what kind of capital gains or losses could he expect over time in the case that he chose to buy the apartment? Jain realized that he had to make a quantitative finance decision of buy versus rent in order to arrive at the right option given his current financial conditions and the potential future benefits Page 2 9B17N016 REAL ESTATE PRICES IN INDIA Given the backdrop of the country's increasing population levels, accelerating economic growth, and rising urbanization, real estate prices in India had witnessed stellar growth, especially in the residential housing segment. As per the residential property price index compiled by the Reserve Bank of India at an all-India level, housing prices in India had risen by almost 72 per cent between 2010-2011 and 2014-2015. While the highest growth was recorded in the City of Lucknow, at around 115 per cent, cities such as Delhi and Greater Mumbai recorded impressive increases of 64 per cent and 82 per cent,' respectively. According to Knight Frank, a leading international property consultancy, price growth in the residential market had generally been a function of employment generation and infrastructure development. Consequently, factors such as a property's proximity to premium office markets, its connectivity with important locations, and the social and physical infrastructure facilities available would determine future price growth in the residential property market. FINANCIAL DETAILS Jain collected all of the necessary information for conducting a financial analysis with regard to buying versus renting an apartment. In the case that Jain decided to buy the apartment, he needed to take care of the following home ownership costs: Down Payment: Jain was required to make a down payment of 20 per cent of the purchase price. He decided he would finance the down payment by monetizing his fixed deposits and savings with several banks, which were currently earning around 7 per cent per year, on average, on a pre-tax basis. Jain decided he would use this annual rate of 7 per cent as his opportunity cost of the down payment. To finance the remaining 80 per cent, Jain decided he would opt for a full tenor fixed-interest rate loan at 10.25 per cent per year (based on monthly compounding) for a period of 20 years (see Exhibit 1). Stamp Duty and Other Charges: Jain estimated that purchasing the property would involve paying a stamp duty and transfer duty at 6 per cent and registration fees at 1 per cent of the sale deed's total value. Property Taxes: Jain estimated that he would have to pay property taxes of R10,000 on the purchased property on an annual basis. Other Charges: Jain would be required to pay brokerage expenses at I per cent of the value of the property for the arranging and executing of the purchase of the property by his broker. Further, the homeowner would incur a recurring society charge of about 1,000 per month (including the use of parking facilities). In the case Jain decided to rent the apartment, the initial option he had considered, he would incur additional expenses related to society charges-about 1,000 per month. In that case, he would also have to pay expenses amounting to 325,000 to his broker for arranging the rental and executing the 11-month rental agreement Page 3 9B17N016 TAX CONSIDERATIONS Besides the above considerations, Jain also took into account the tax benefits on a home loan provided under India's Income Tax Act. Under Section 24 of the Act, a deduction of up to 3200,000 for the payment of interest on a housing loan was allowed in a financial year. Similarly, under Section 80C, a tax deduction of up to 2150,000 was allowed in a financial year for principal repayment on a housing loan. This would have entailed substantial benefits for Jain, given his marginal tax rate bracket of 30 per cent a FINANCIAL INVESTMENT DECISION With the above information in hand, Jain conducted a quantitative analysis using time value techniques, and compared the monthly payments required to buy the apartment with those required to rent the apartment, taking into account taxation and opportunity cost considerations. For opportunity costs, Jain assumed a rate of 7 per cent per year (as previously discussed) on his existing fixed deposit as a proxy. Jain also wanted to determine the future capital gains and losses in the case that he decided to sell his house 20 years into the future (after completing his loan payments). For this, he needed to model the selling price of the house at a future date. Given his understanding of the real estate market in India and past data on prices in the residential housing market, Jain decided to model a conservative 7 per cent per year appreciation in housing prices over the next 20 years in his base case scenario. Page 4 EXHIBIT 1: ANNUAL LOAN AMORTIZATION SCHEDULE Loan Amount Interest Rate Loan Term 310,000,000 10.25 per cent 20 Years Year 1 2 3 4 5 6 7 8 9 Annual Loan Amortization Schedule Principal ) Interest () Balance () 160,367 1,017,605 9,839,633 177.599 1,000,373 9,662,033 196,683 981,289 9,465,350 217,818 960,154 9,247,532 241,224 936,748 9,006,308 267,144 910,828 8,739,164 295,851 882,122 8,443,313 327,641 850,331 8,115,672 362,848 815,124 7.752,824 401,838 776,134 7,350,986 445,017 732,955 6,905,969 492,837 685,135 6,413,132 545,795 632,178 5,867,338 604.443 573,529 5,262,895 669,393 508,579 4,593,501 741,323 436,649 3,852,178 820,982 356,990 3,031,196 909,201 268,771 2,121,995 1,006,899 171,073 1,115,096 1,115,096 62,876 10 11 12 13 14 15 16 17 18 19 20 Source: HDFC, "Home Loan EMI Calculator, "accessed December 20, 2016, https://www.hdfc.com/home-loan-eml-calculator ASSIGNMENT QUESTIONS 1. Discuss the rationale and significance of the time value of money 2. Using the time value of money framework, determine the equated monthly instalments (PMT) in the case that Jain opts to buy the apartment 3. Using the time value of money framework, determine the total monthly payments for the proposed alternative to buy (taking into account opportunity costs and taxes). 4. Using the time value of money framework, determine the total monthly payments for the proposed alternative to rent 5. Determine the future capital gain/loss incurred after modelling the selling price of the apartment, using a conservative 7 per cent annual appreciation in housing prices. Determine the present value of such capital gain/loss after taking into account the time value of money. 6. Based on your analysis, as Jain, would you decide to buy or to rent Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Jack Kapoor, Les Dlabay, Robert J. Hughes

11th edition

9781259278617, 77861647, 1259278611, 978-0077861643