PLEASE ANSWER ALL 8 Questions

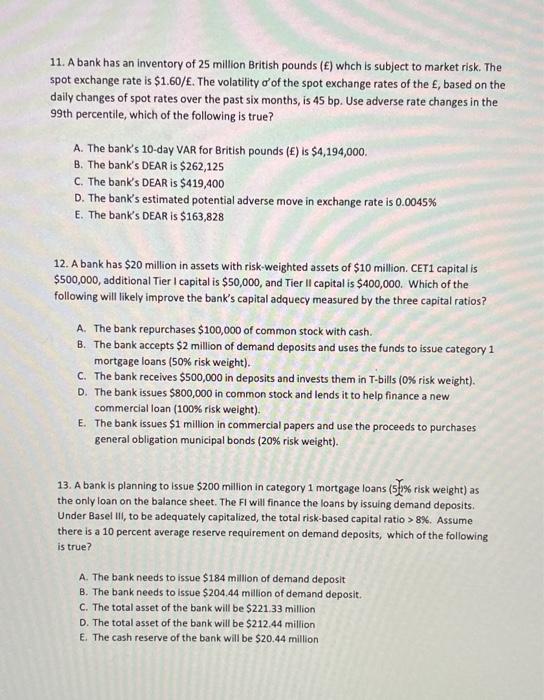

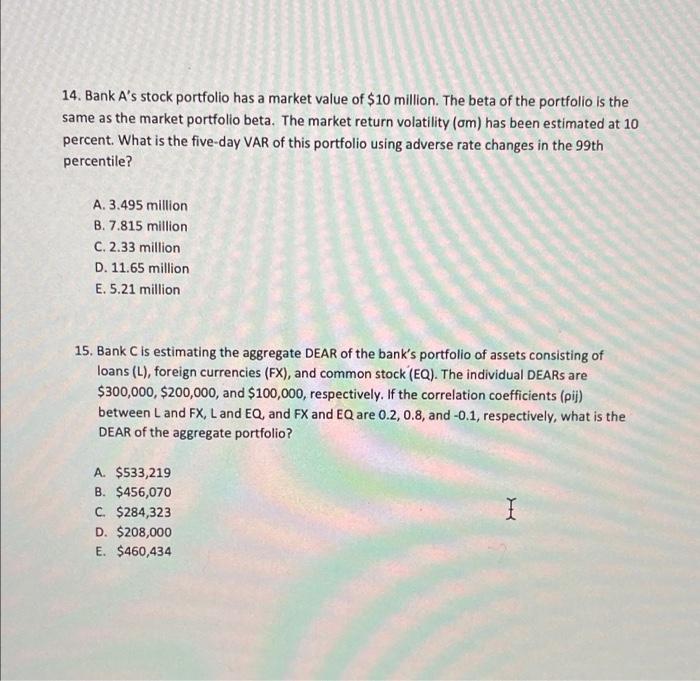

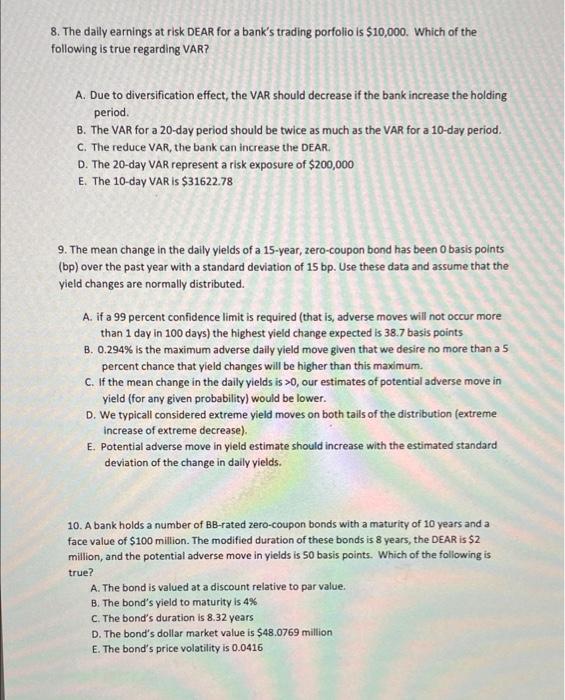

8. The daily earnings at risk DEAR for a bank's trading porfolio is $10,000. Which of the following is true regarding VAR? A. Due to diversification effect, the VAR should decrease if the bank increase the holding period B. The VAR for a 20-day period should be twice as much as the VAR for a 10-day period. C. The reduce VAR, the bank can increase the DEAR. D. The 20-day VAR represent a risk exposure of $200,000 E. The 10-day VAR is $31622.78 9. The mean change in the daily yields of a 15-year, zero-coupon bond has been 0 basis points (bp) over the past year with a standard deviation of 15 bp. Use these data and assume that the yield changes are normally distributed. A. if a 99 percent confidence limit is required (that is, adverse moves will not occur more than 1 day in 100 days) the highest yield change expected is 38.7 basis points B. 0.294% is the maximum adverse daily yield move given that we desire no more than a 5 percent chance that yield changes will be higher than this maximum. C. If the mean change in the daily yields is >0, our estimates of potential adverse move in yield (for any given probability) would be lower. D. We typicall considered extreme yield moves on both tails of the distribution (extreme increase of extreme decrease). E. Potential adverse move in yleld estimate should increase with the estimated standard deviation of the change in daily yields. 10. A bank holds a number of BB-rated zero-coupon bonds with a maturity of 10 years and a face value of $100 million. The modified duration of these bonds is 8 years, the DEAR is $2 million, and the potential adverse move in yields is 50 basis points. Which of the following is true? A. The bond is valued at a discount relative to par value. B. The bond's yield to maturity is 4% C. The bond's duration is 8.32 years D. The bond's dollar market value is $48.0769 million E. The bond's price volatility is 0.0416 11. A bank has an inventory of 25 million British pounds () whch is subject to market risk. The spot exchange rate is $1.60/. The volatility o' of the spot exchange rates of the , based on the daily changes of spot rates over the past six months, is 45 bp. Use adverse rate changes in the 99th percentile, which of the following is true? A. The bank's 10-day VaR for British pounds () is $4,194,000. B. The bank's DEAR is $262,125 C. The bank's DEAR is $419,400 D. The bank's estimated potential adverse move in exchange rate is 0.0045% E. The bank's DEAR is $163,828 12. A bank has $20 million in assets with risk-weighted assets of $10 million CET1 capital is $500,000, additional Tier I capital is $50,000, and Tier II capital is $400,000. Which of the following will likely improve the bank's capital adquecy measured by the three capital ratios? A. The bank repurchases $100,000 of common stock with cash. B. The bank accepts $2 million of demand deposits and uses the funds to issue category 1 mortgage loans (50% risk weight). C. The bank receives $500,000 in deposits and invests them in T-bills (0% risk weight). D. The bank issues $800,000 in common stock and lends it to help finance a new commercial loan (100% risk weight) E. The bank issues $1 million in commercial papers and use the proceeds to purchases general obligation municipal bonds (20% risk weight). 13. A bank is planning to issue $200 million in category 1 mortgage loans (${1% risk weight) as the only loan on the balance sheet. The Fl will finance the loans by issuing demand deposits. Under Basel II, to be adequately capitalized, the total risk-based capital ratio > 8%. Assume there is a 10 percent average reserve requirement on demand deposits, which of the following is true? A. The bank needs to issue $184 million of demand deposit 8. The bank needs to issue $204.44 million of demand deposit. C. The total asset of the bank will be $221.33 million D. The total asset of the bank will be $212.44 million E. The cash reserve of the bank will be $20.44 million 14. Bank A's stock portfolio has a market value of $10 million. The beta of the portfolio is the same as the market portfolio beta. The market return volatility (am) has been estimated at 10 percent. What is the five-day VAR of this portfolio using adverse rate changes in the 99th percentile? A. 3.495 million B. 7.815 million C. 2.33 million D. 11.65 million E. 5.21 million 15. Bank C is estimating the aggregate DEAR of the bank's portfolio of assets consisting of loans (L), foreign currencies (FX), and common stock (EQ). The individual DEARs are $300,000, $200,000, and $100,000, respectively. If the correlation coefficients (pij) between Land FX, L and EQ, and FX and EQ are 0.2, 0.8, and -0.1, respectively, what is the DEAR of the aggregate portfolio? A. $533,219 B. $456,070 C. $284,323 D. $208,000 E. $460,434 I 8. The daily earnings at risk DEAR for a bank's trading porfolio is $10,000. Which of the following is true regarding VAR? A. Due to diversification effect, the VAR should decrease if the bank increase the holding period B. The VAR for a 20-day period should be twice as much as the VAR for a 10-day period. C. The reduce VAR, the bank can increase the DEAR. D. The 20-day VAR represent a risk exposure of $200,000 E. The 10-day VAR is $31622.78 9. The mean change in the daily yields of a 15-year, zero-coupon bond has been 0 basis points (bp) over the past year with a standard deviation of 15 bp. Use these data and assume that the yield changes are normally distributed. A. if a 99 percent confidence limit is required (that is, adverse moves will not occur more than 1 day in 100 days) the highest yield change expected is 38.7 basis points B. 0.294% is the maximum adverse daily yield move given that we desire no more than a 5 percent chance that yield changes will be higher than this maximum. C. If the mean change in the daily yields is >0, our estimates of potential adverse move in yield (for any given probability) would be lower. D. We typicall considered extreme yield moves on both tails of the distribution (extreme increase of extreme decrease). E. Potential adverse move in yleld estimate should increase with the estimated standard deviation of the change in daily yields. 10. A bank holds a number of BB-rated zero-coupon bonds with a maturity of 10 years and a face value of $100 million. The modified duration of these bonds is 8 years, the DEAR is $2 million, and the potential adverse move in yields is 50 basis points. Which of the following is true? A. The bond is valued at a discount relative to par value. B. The bond's yield to maturity is 4% C. The bond's duration is 8.32 years D. The bond's dollar market value is $48.0769 million E. The bond's price volatility is 0.0416 11. A bank has an inventory of 25 million British pounds () whch is subject to market risk. The spot exchange rate is $1.60/. The volatility o' of the spot exchange rates of the , based on the daily changes of spot rates over the past six months, is 45 bp. Use adverse rate changes in the 99th percentile, which of the following is true? A. The bank's 10-day VaR for British pounds () is $4,194,000. B. The bank's DEAR is $262,125 C. The bank's DEAR is $419,400 D. The bank's estimated potential adverse move in exchange rate is 0.0045% E. The bank's DEAR is $163,828 12. A bank has $20 million in assets with risk-weighted assets of $10 million CET1 capital is $500,000, additional Tier I capital is $50,000, and Tier II capital is $400,000. Which of the following will likely improve the bank's capital adquecy measured by the three capital ratios? A. The bank repurchases $100,000 of common stock with cash. B. The bank accepts $2 million of demand deposits and uses the funds to issue category 1 mortgage loans (50% risk weight). C. The bank receives $500,000 in deposits and invests them in T-bills (0% risk weight). D. The bank issues $800,000 in common stock and lends it to help finance a new commercial loan (100% risk weight) E. The bank issues $1 million in commercial papers and use the proceeds to purchases general obligation municipal bonds (20% risk weight). 13. A bank is planning to issue $200 million in category 1 mortgage loans (${1% risk weight) as the only loan on the balance sheet. The Fl will finance the loans by issuing demand deposits. Under Basel II, to be adequately capitalized, the total risk-based capital ratio > 8%. Assume there is a 10 percent average reserve requirement on demand deposits, which of the following is true? A. The bank needs to issue $184 million of demand deposit 8. The bank needs to issue $204.44 million of demand deposit. C. The total asset of the bank will be $221.33 million D. The total asset of the bank will be $212.44 million E. The cash reserve of the bank will be $20.44 million 14. Bank A's stock portfolio has a market value of $10 million. The beta of the portfolio is the same as the market portfolio beta. The market return volatility (am) has been estimated at 10 percent. What is the five-day VAR of this portfolio using adverse rate changes in the 99th percentile? A. 3.495 million B. 7.815 million C. 2.33 million D. 11.65 million E. 5.21 million 15. Bank C is estimating the aggregate DEAR of the bank's portfolio of assets consisting of loans (L), foreign currencies (FX), and common stock (EQ). The individual DEARs are $300,000, $200,000, and $100,000, respectively. If the correlation coefficients (pij) between Land FX, L and EQ, and FX and EQ are 0.2, 0.8, and -0.1, respectively, what is the DEAR of the aggregate portfolio? A. $533,219 B. $456,070 C. $284,323 D. $208,000 E. $460,434