Answered step by step

Verified Expert Solution

Question

1 Approved Answer

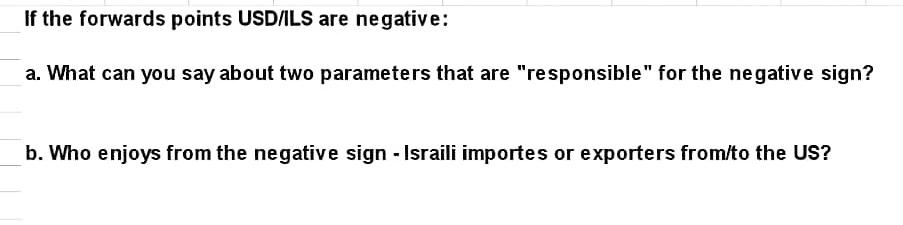

Please answer all Macaulay duration of the bond portfolio is 10 and the modified duration is 5. a. How this difference can be explained? b.

Please answer all

Macaulay duration of the bond portfolio is 10 and the modified duration is 5. a. How this difference can be explained? b. If we add to the portfolio a bond mature d in 15 ye ars, how will its Macaulay duration and the modified duration change? If the forwards points USD/ILS are negative: a. What can you say about two parameters that are "responsible" for the negative sign? b. Who enjoys from the negative sign - Israili importes or exporters from/to the US? Macaulay duration of the bond portfolio is 10 and the modified duration is 5. a. How this difference can be explained? b. If we add to the portfolio a bond mature d in 15 ye ars, how will its Macaulay duration and the modified duration change? If the forwards points USD/ILS are negative: a. What can you say about two parameters that are "responsible" for the negative sign? b. Who enjoys from the negative sign - Israili importes or exporters from/to the USStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Energy And Finance Sustainability In The Energy Industry

Authors: André Dorsman, Özgür Arslan-Ayaydin, Mehmet Baha Karan

1st Edition

3319322664, 978-3319322667