please answer all of these question by using word or excel thank you!

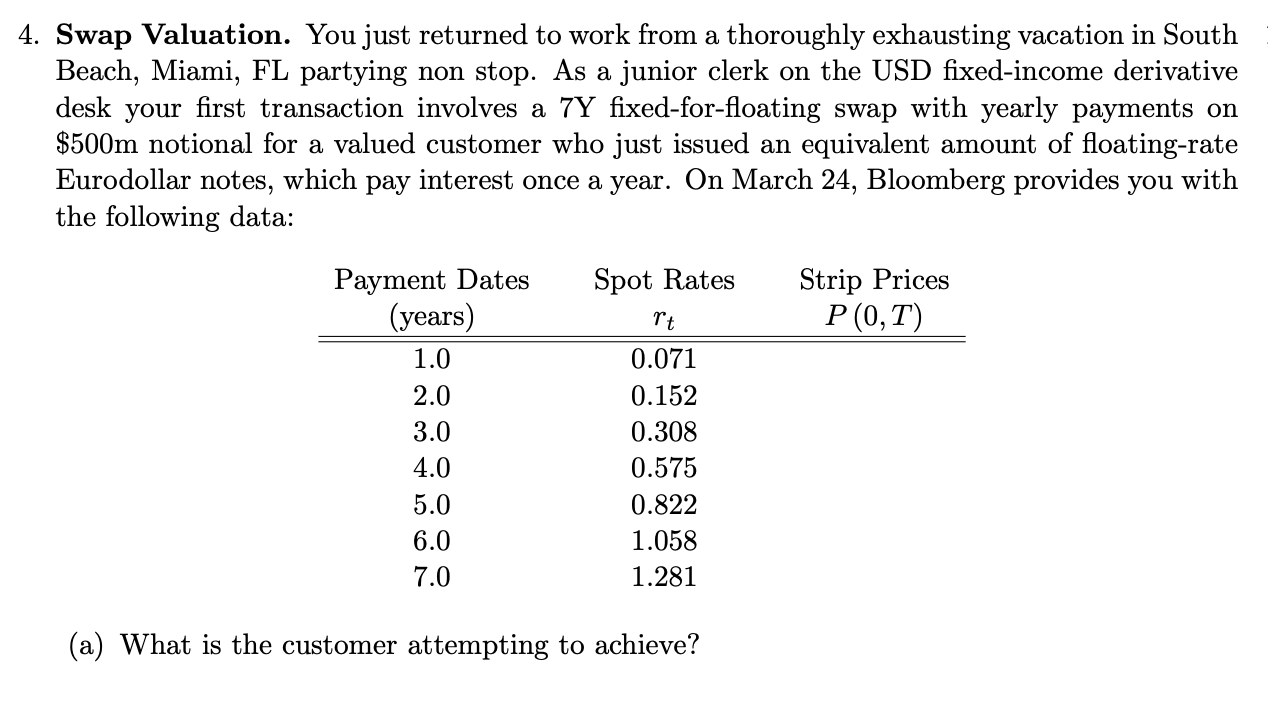

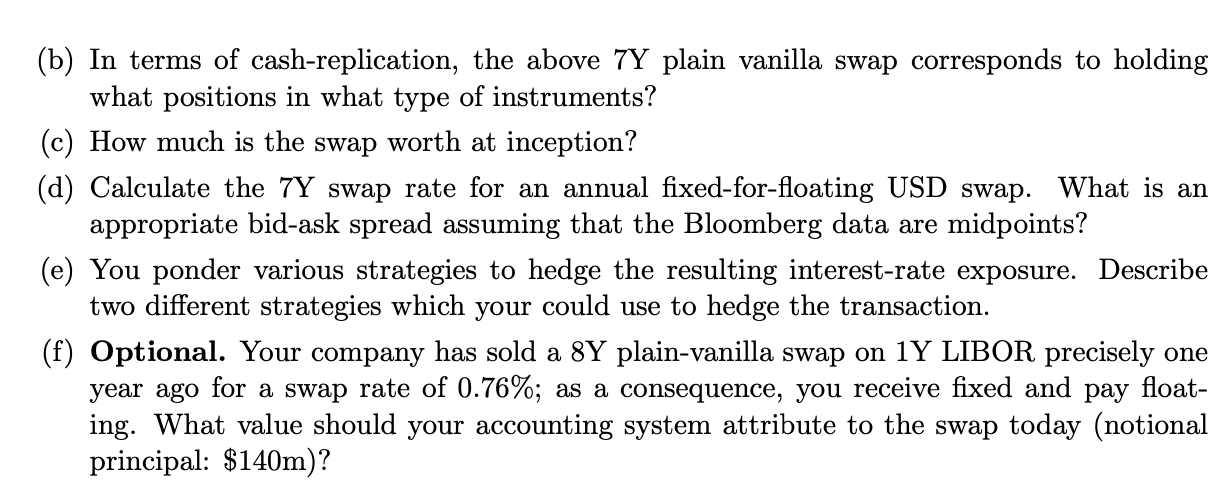

4. Swap Valuation. You just returned to work from a thoroughly exhausting vacation in South Beach, Miami, FL partying non stop. As a junior clerk on the USD fixed-income derivative desk your first transaction involves a 7Y fixed-for-floating swap with yearly payments on $500m notional for a valued customer who just issued an equivalent amount of floating-rate Eurodollar notes, which pay interest once a year. On March 24, Bloomberg provides you with the following data: Strip Prices P(0,T) Payment Dates (years) 1.0 2.0 3.0 4.0 5.0 Spot Rates rt 0.071 0.152 0.308 0.575 0.822 1.058 1.281 6.0 7.0 (a) What is the customer attempting to achieve? (b) In terms of cash-replication, the above 7Y plain vanilla swap corresponds to holding what positions in what type of instruments? (c) How much is the swap worth at inception? (d) Calculate the 7Y swap rate for an annual fixed-for-floating USD swap. What is an appropriate bid-ask spread assuming that the Bloomberg data are midpoints? (e) You ponder various strategies to hedge the resulting interest-rate exposure. Describe two different strategies which your could use to hedge the transaction. (f) Optional. Your company has sold a 8Y plain-vanilla swap on 1Y LIBOR precisely one year ago for a swap rate of 0.76%; as a consequence, you receive fixed and pay float- ing. What value should your accounting system attribute to the swap today (notional principal: $140m)? 4. Swap Valuation. You just returned to work from a thoroughly exhausting vacation in South Beach, Miami, FL partying non stop. As a junior clerk on the USD fixed-income derivative desk your first transaction involves a 7Y fixed-for-floating swap with yearly payments on $500m notional for a valued customer who just issued an equivalent amount of floating-rate Eurodollar notes, which pay interest once a year. On March 24, Bloomberg provides you with the following data: Strip Prices P(0,T) Payment Dates (years) 1.0 2.0 3.0 4.0 5.0 Spot Rates rt 0.071 0.152 0.308 0.575 0.822 1.058 1.281 6.0 7.0 (a) What is the customer attempting to achieve? (b) In terms of cash-replication, the above 7Y plain vanilla swap corresponds to holding what positions in what type of instruments? (c) How much is the swap worth at inception? (d) Calculate the 7Y swap rate for an annual fixed-for-floating USD swap. What is an appropriate bid-ask spread assuming that the Bloomberg data are midpoints? (e) You ponder various strategies to hedge the resulting interest-rate exposure. Describe two different strategies which your could use to hedge the transaction. (f) Optional. Your company has sold a 8Y plain-vanilla swap on 1Y LIBOR precisely one year ago for a swap rate of 0.76%; as a consequence, you receive fixed and pay float- ing. What value should your accounting system attribute to the swap today (notional principal: $140m)