Answered step by step

Verified Expert Solution

Question

1 Approved Answer

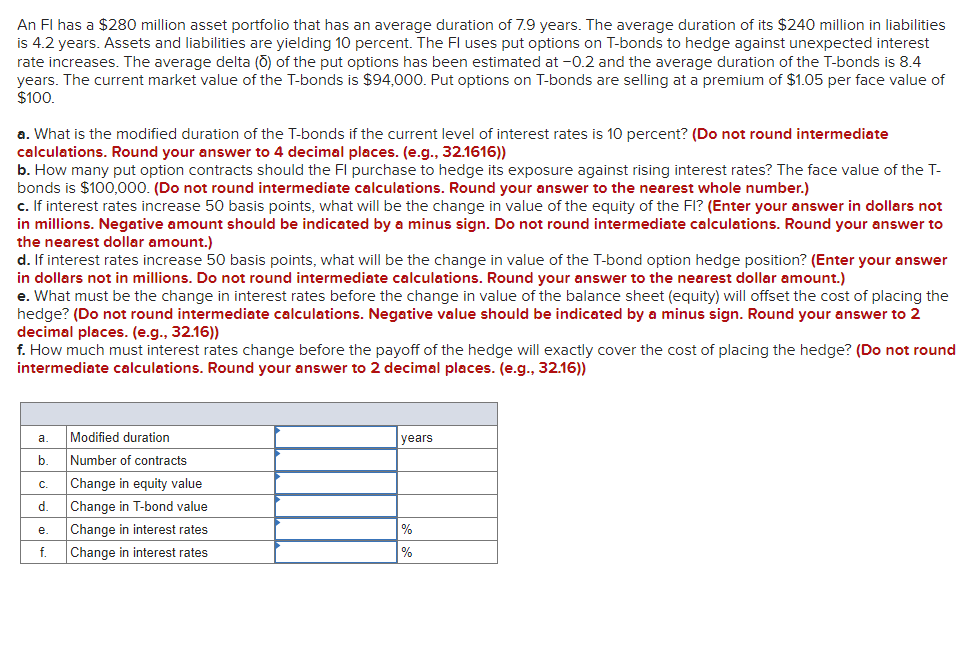

Please answer all parts. An FI has a $280 million asset portfolio that has an average duration of 7.9 years. The average duration of its

Please answer all parts.

An FI has a $280 million asset portfolio that has an average duration of 7.9 years. The average duration of its $240 million in liabilities is 4.2 years. Assets and liabilities are yielding 10 percent. The Fl uses put options on T-bonds to hedge against unexpected interest rate increases. The average delta (0) of the put options has been estimated at -0.2 and the average duration of the T-bonds is 8.4 years. The current market value of the T-bonds is $94,000. Put options on T-bonds are selling at a premium of $1.05 per face value of $100. a. What is the modified duration of the T-bonds if the current level of interest rates is 10 percent? (Do not round intermediate calculations. Round your answer to 4 decimal places. (e.g., 32.1616)) b. How many put option contracts should the FI purchase to hedge its exposure against rising interest rates? The face value of the Tbonds is $100,000. (Do not round intermediate calculations. Round your answer to the nearest whole number.) c. If interest rates increase 50 basis points, what will be the change in value of the equity of the FI? (Enter your answer in dollars not in millions. Negative amount should be indicated by a minus sign. Do not round intermediate calculations. Round your answer to the nearest dollar amount.) d. If interest rates increase 50 basis points, what will be the change in value of the T-bond option hedge position? (Enter your answer in dollars not in millions. Do not round intermediate calculations. Round your answer to the nearest dollar amount.) e. What must be the change in interest rates before the change in value of the balance sheet (equity) will offset the cost of placing the hedge? (Do not round intermediate calculations. Negative value should be indicated by a minus sign. Round your answer to 2 decimal places. (e.g., 32.16)) f. How much must interest rates change before the payoff of the hedge will exactly cover the cost of placing the hedge? (Do not round intermediate calculations. Round your answer to 2 decimal places. (e.g., 32.16))Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Forex Trading

Authors: Paul Millis

1st Edition

979-8699265442