Answered step by step

Verified Expert Solution

Question

1 Approved Answer

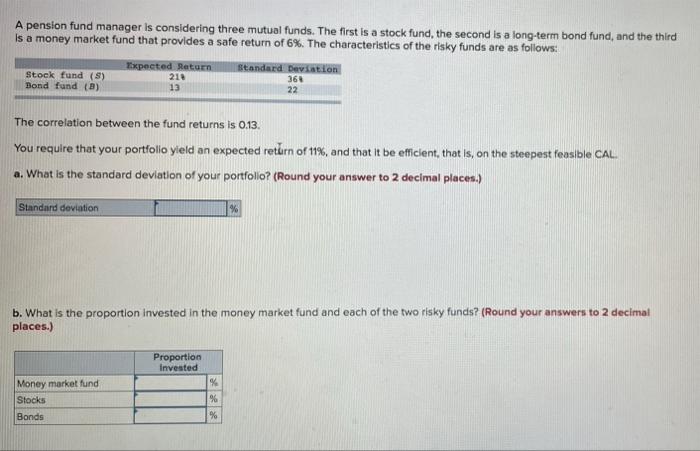

please answer all parts correctly A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term

please answer all parts correctly

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term bond fund, and the third is a money market fund that provides a safe return of 6%. The characteristics of the risky funds are as follows: Stock fund (S) Bond fund (B) Standard deviation Expected Return 219 13 The correlation between the fund returns is 0.13. You require that your portfolio yield an expected return of 11%, and that it be efficient, that is, on the steepest feasible CAL. a. What is the standard deviation of your portfolio? (Round your answer to 2 decimal places.) Money market fund Stocks Bonds b. What is the proportion invested in the money market fund and each of the two risky funds? (Round your answers to 2 decimal places.) Standard Deviation 36% 22 Proportion Invested % % % Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Municipal Budget Crunch A Handbook For Professionals

Authors: Roger L. Kemp

1st Edition

0786463740, 978-0786463749