Answered step by step

Verified Expert Solution

Question

1 Approved Answer

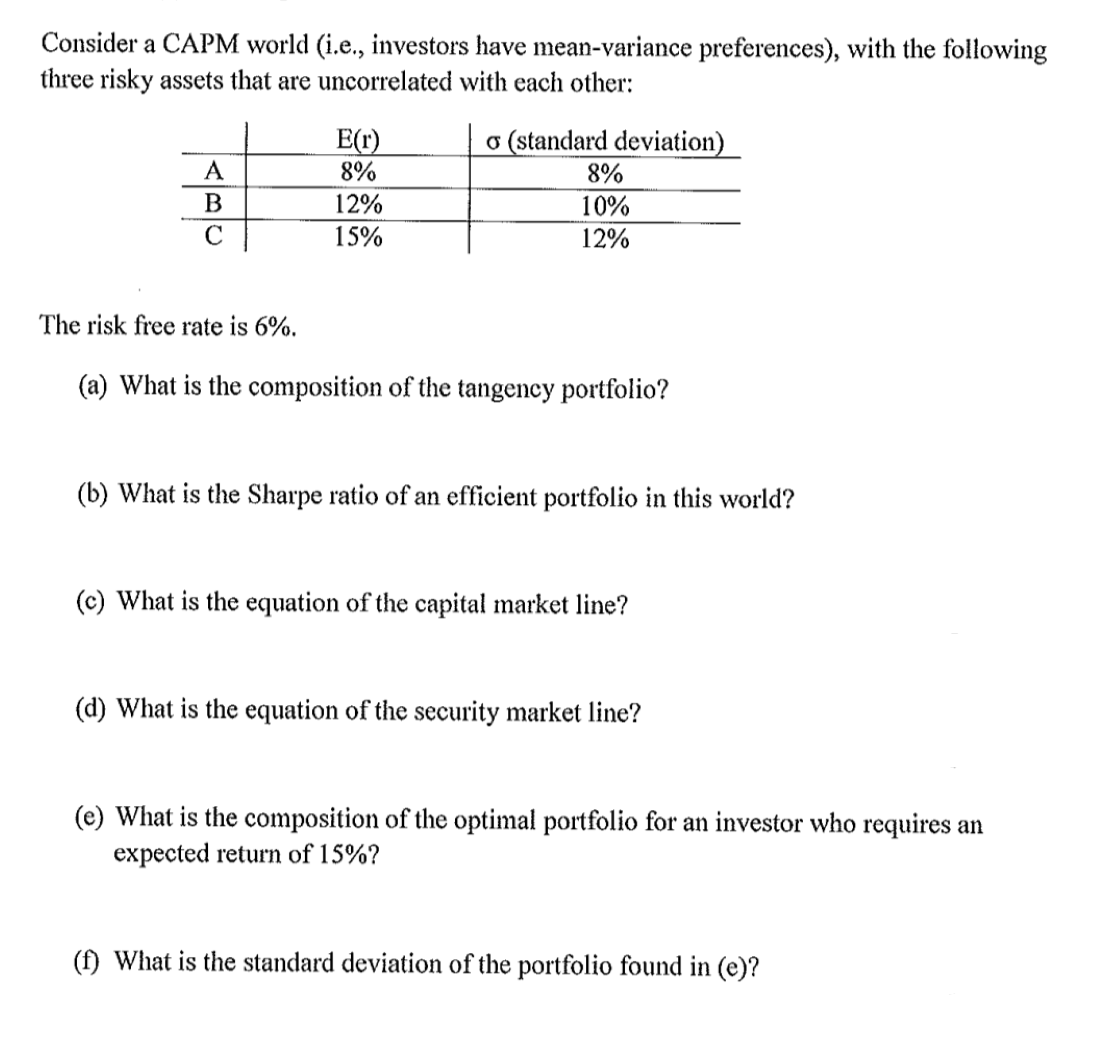

Please answer all question with details. Consider a CAPM world ( i . e . , investors have mean - variance preferences ) , with

Please answer all question with details.

Consider a CAPM world ie investors have meanvariance preferences with the following

three risky assets that are uncorrelated with each other:

The risk free rate is

a What is the composition of the tangency portfolio?

b What is the Sharpe ratio of an efficient portfolio in this world?

c What is the equation of the capital market line?

d What is the equation of the security market line?

e What is the composition of the optimal portfolio for an investor who requires an

expected return of

f What is the standard deviation of the portfolio found in e

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Democracy Towards A Sustainable Financial System

Authors: Alessandro Vercelli

1st Edition

3030279111, 978-3030279110