Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer all Questions and provide working out The price of an asset at close of trading yesterday was $100 and its volatility was estimated

Please answer all Questions and provide working out

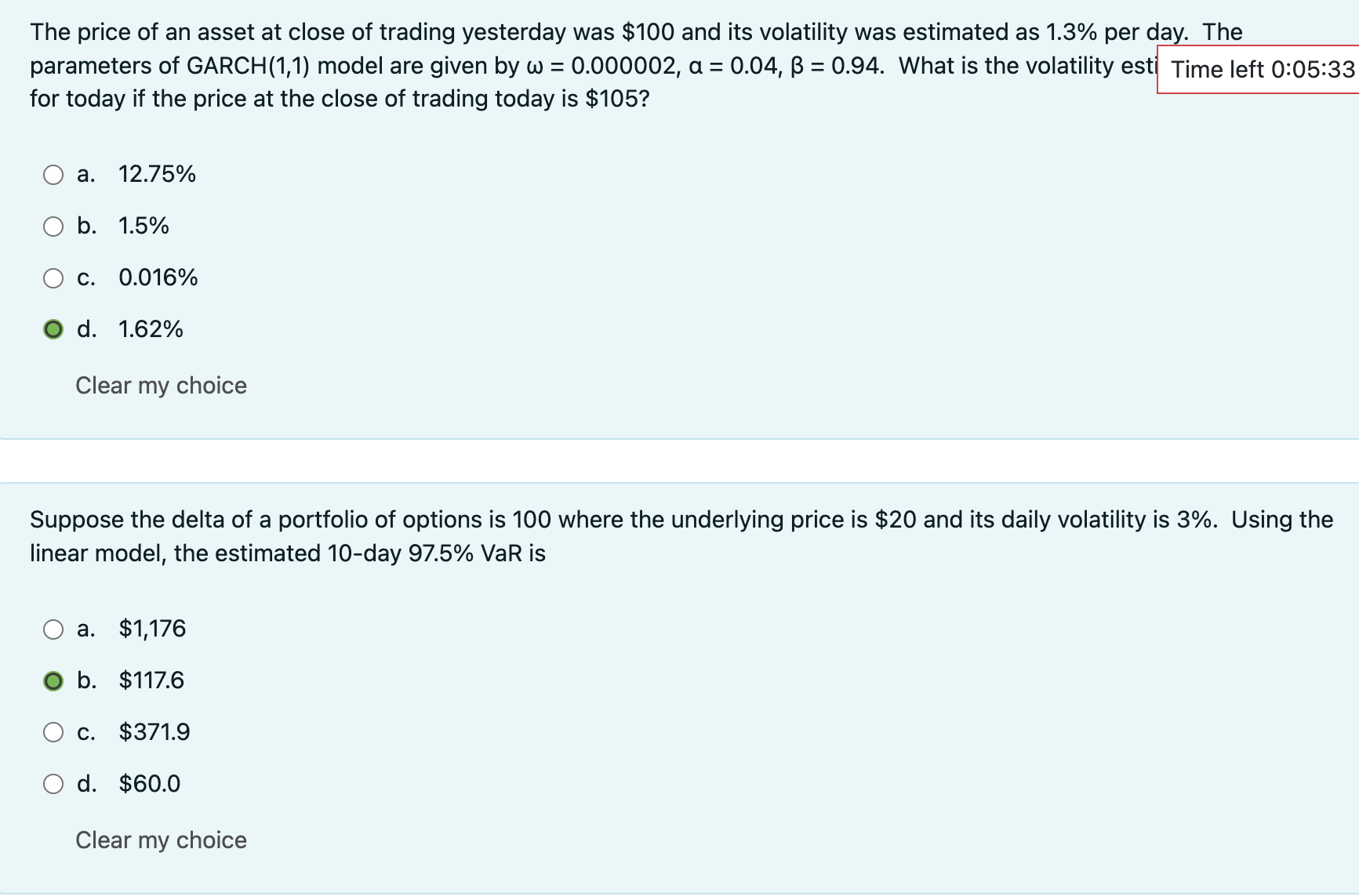

The price of an asset at close of trading yesterday was $100 and its volatility was estimated as 1.3% per day. The parameters of GARCH(1,1) model are given by =0.000002,a=0.04,=0.94. What is the volatility est for today if the price at the close of trading today is $105 ? a. 12.75% b. 1.5% c. 0.016% d. 1.62% Clear my choice Suppose the delta of a portfolio of options is 100 where the underlying price is $20 and its daily volatility is 3%. Using the linear model, the estimated 10 -day 97.5% VaR is a. $1,176 b. $117.6 c. $371.9 d. $60.0 Clear my choice

The price of an asset at close of trading yesterday was $100 and its volatility was estimated as 1.3% per day. The parameters of GARCH(1,1) model are given by =0.000002,a=0.04,=0.94. What is the volatility est for today if the price at the close of trading today is $105 ? a. 12.75% b. 1.5% c. 0.016% d. 1.62% Clear my choice Suppose the delta of a portfolio of options is 100 where the underlying price is $20 and its daily volatility is 3%. Using the linear model, the estimated 10 -day 97.5% VaR is a. $1,176 b. $117.6 c. $371.9 d. $60.0 Clear my choice Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Regulation Of Securities Markets And Transactions

Authors: Patrick S. Collins

1st Edition

0470601965, 978-0470601969