Question

Please answer all questions to receive full credit. Assignment: This assignment has two parts. Review the Case Study Applying the Discounted Cash Flow Method of

Please answer all questions to receive full credit.

Assignment:

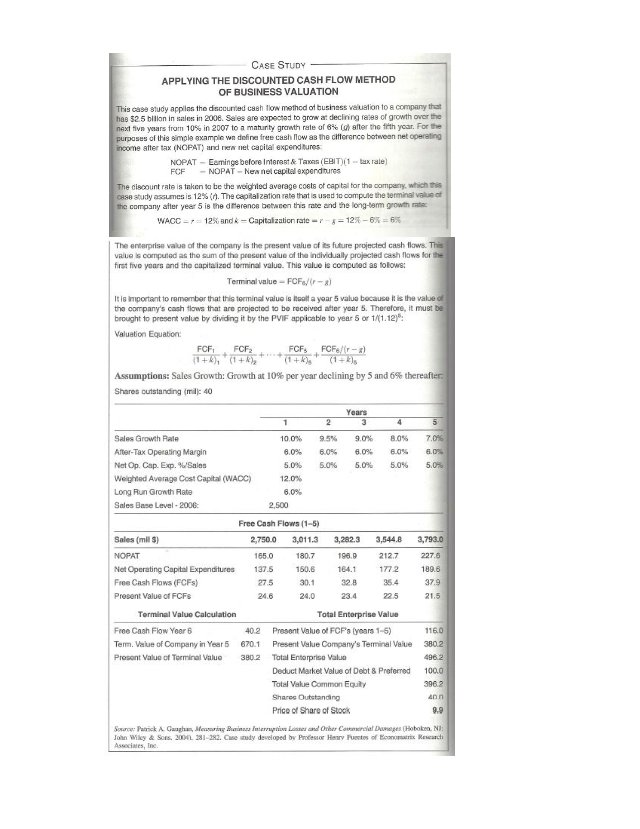

This assignment has two parts. Review the Case Study Applying the Discounted Cash Flow Method of Business Valuation on page 565 and 566 of the text. (see attached image)

Part 1: Make two simple assumption changes:

Base year revenue is $2.0 billion in 2006 (as compared to $2.5 billion in the Book and Lecture).

The maturity growth rate is 7%, rather than 6%.

Please recreate the Free Cash Flow, Terminal Value and Total Enterprise Value tables and fill in numbers based on these assumption changes.

You should use Excel for the calculations. Then copy and paste that to Word. Please Paste Special and select Microsoft Excel Worksheet Object.

Part 2: Discuss some of the benefits and disadvantages of using the Discounted Cash Flow valuation method.

Please keep the text for Part 2 to less than 200 words.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investing Made Simple And Easy The 49 Essential Personal Finance Wealth Management And Trading Tips That Pros Should Share

Authors: WallStreet Smart, Franck Normandeau

1st Edition

B0B2TPPPG3, 979-8827503538