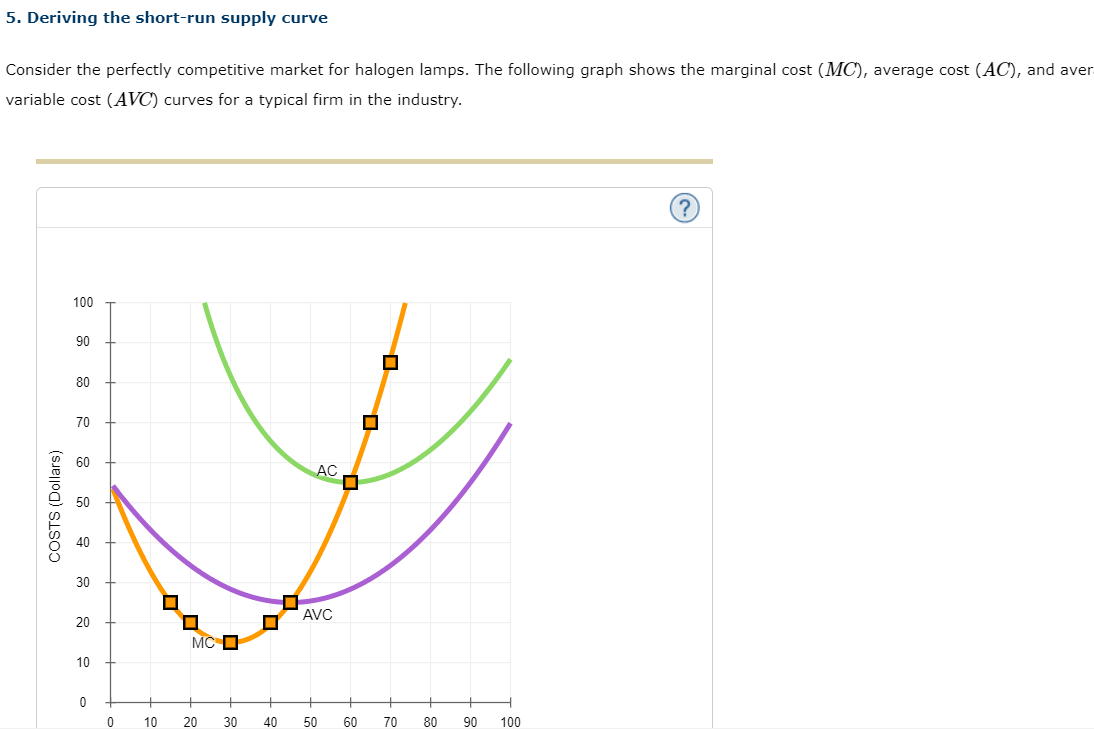

Please answer all the questions 5. Deriving the short-run supply curve Consider the perfectly competitive market for halogen lamps. The following graph shows the marginal

Please answer all the questions

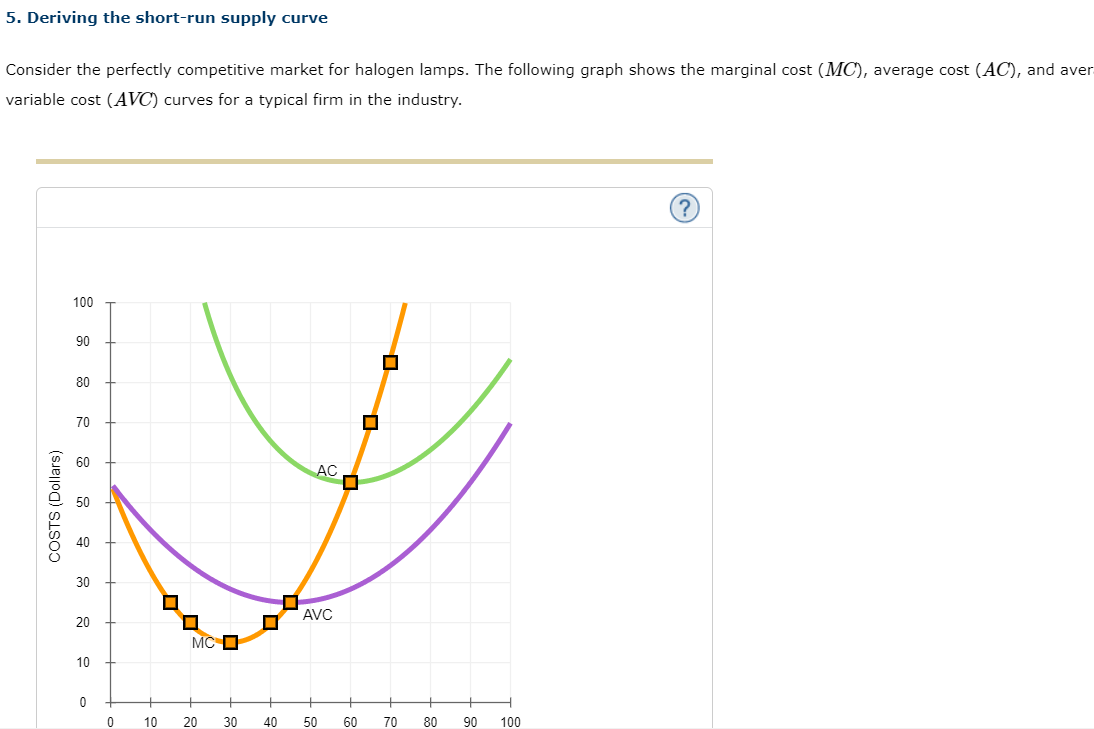

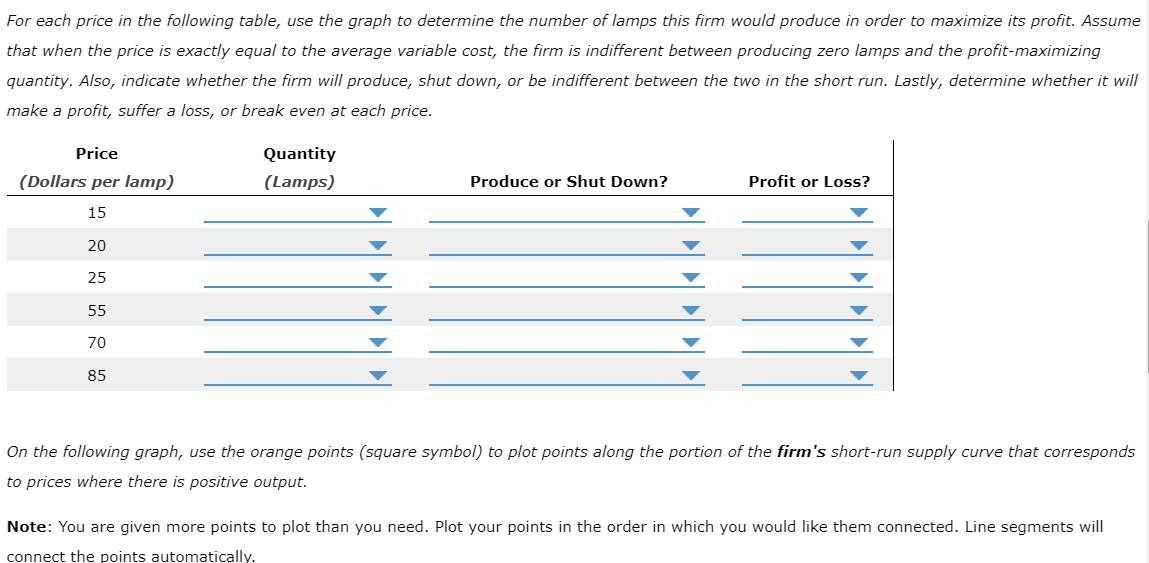

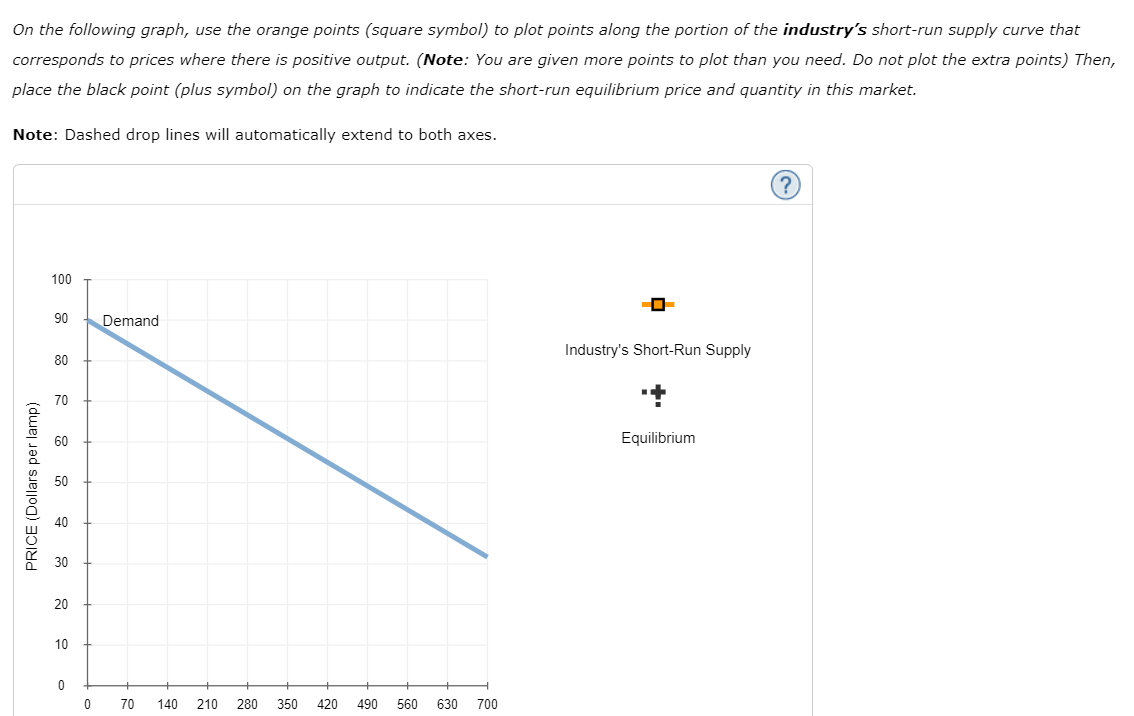

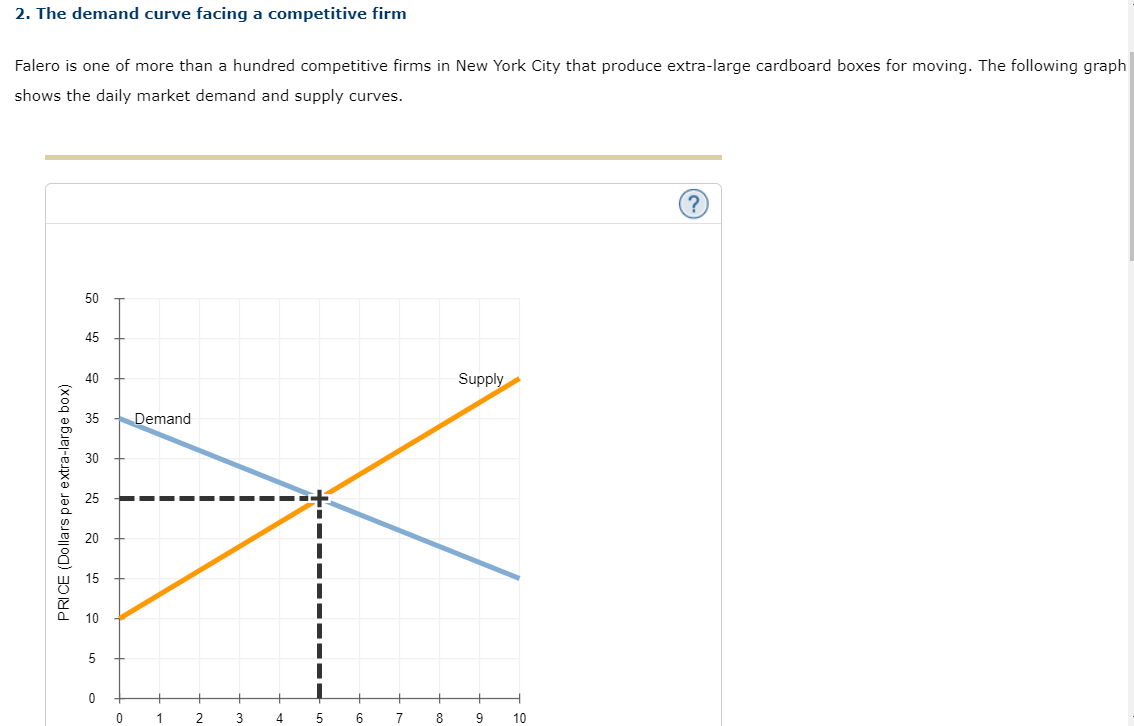

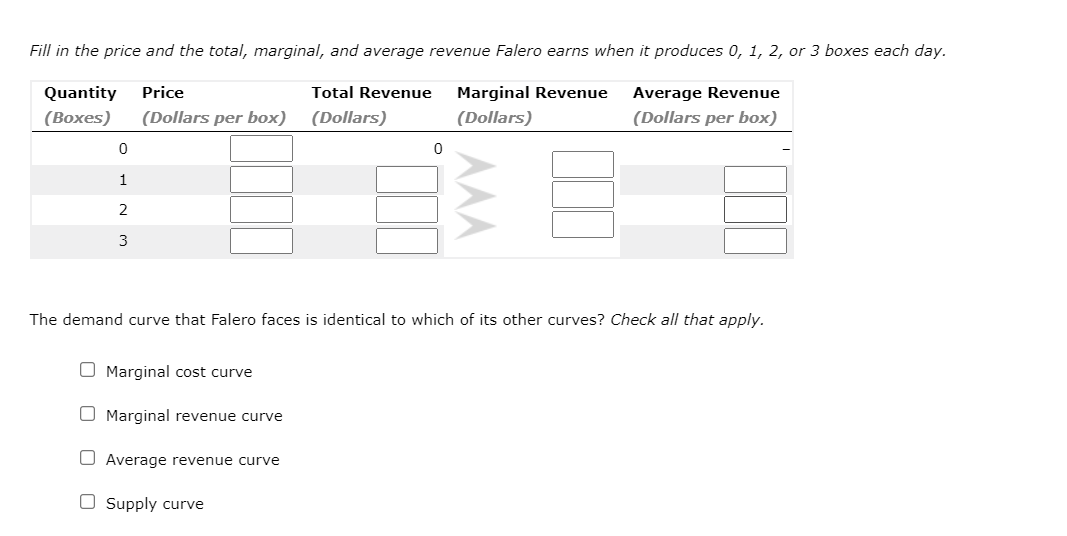

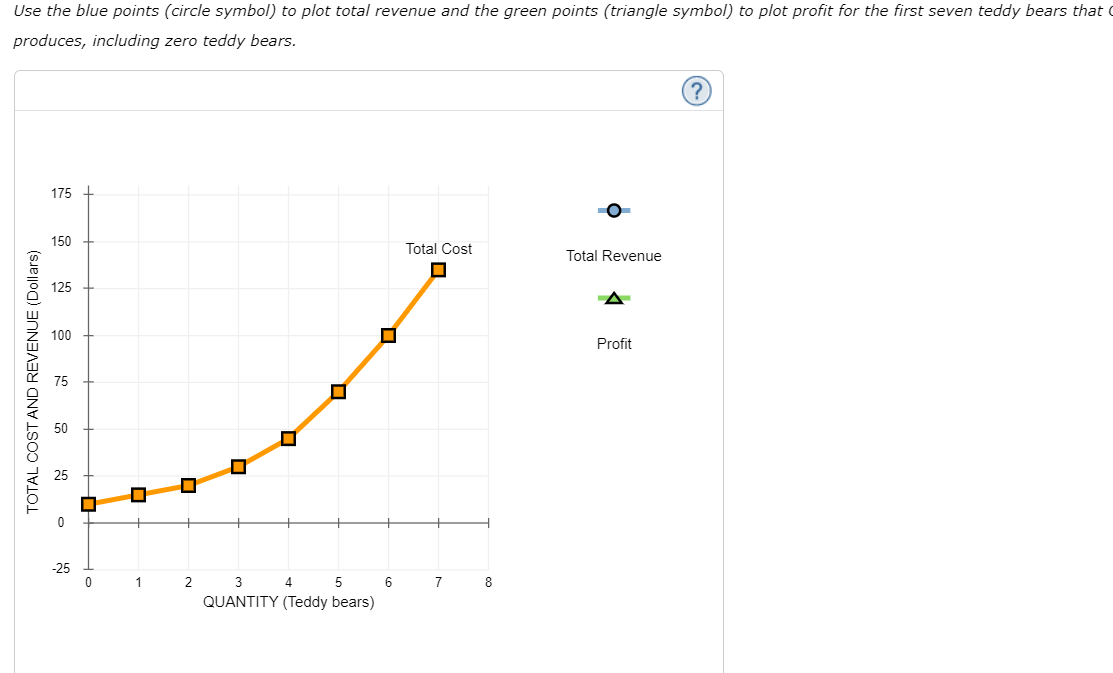

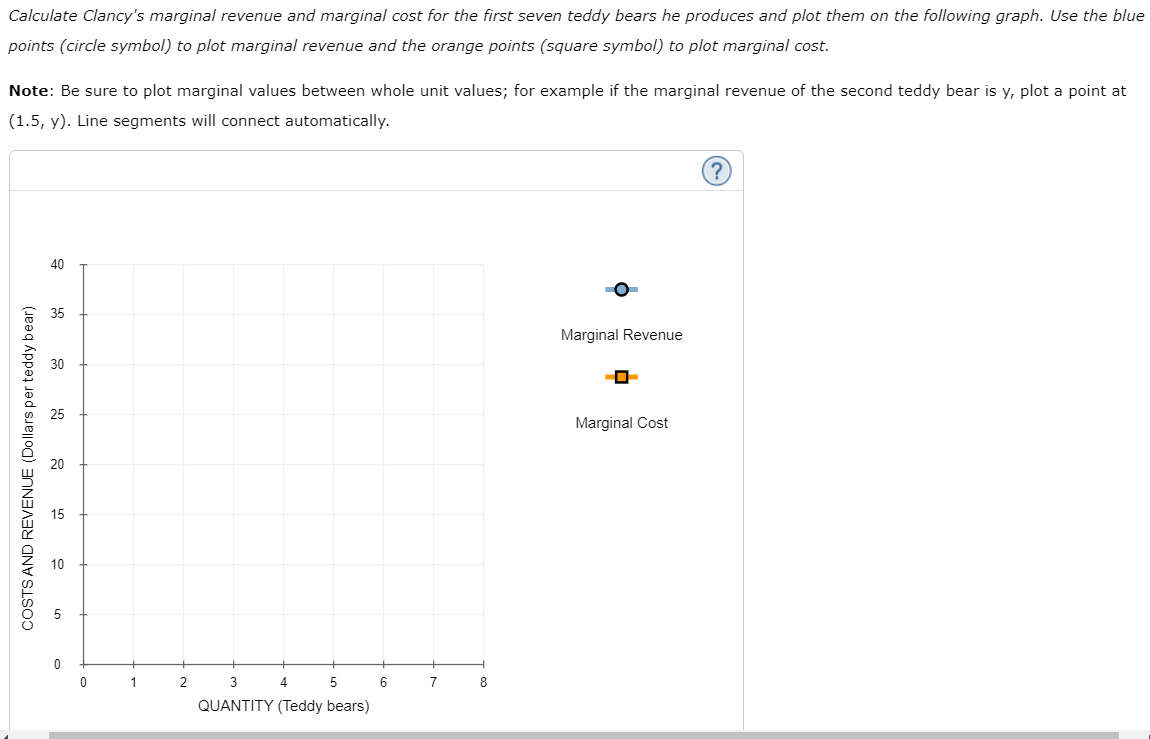

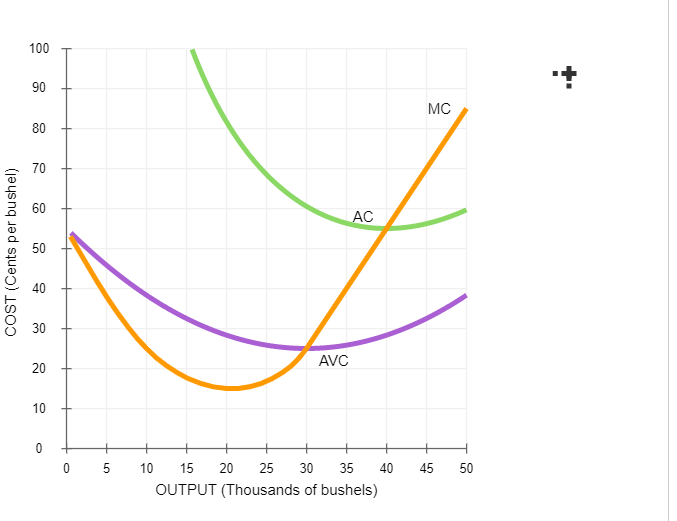

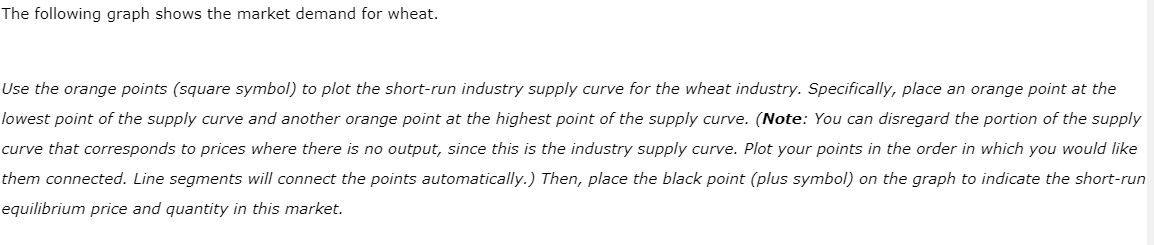

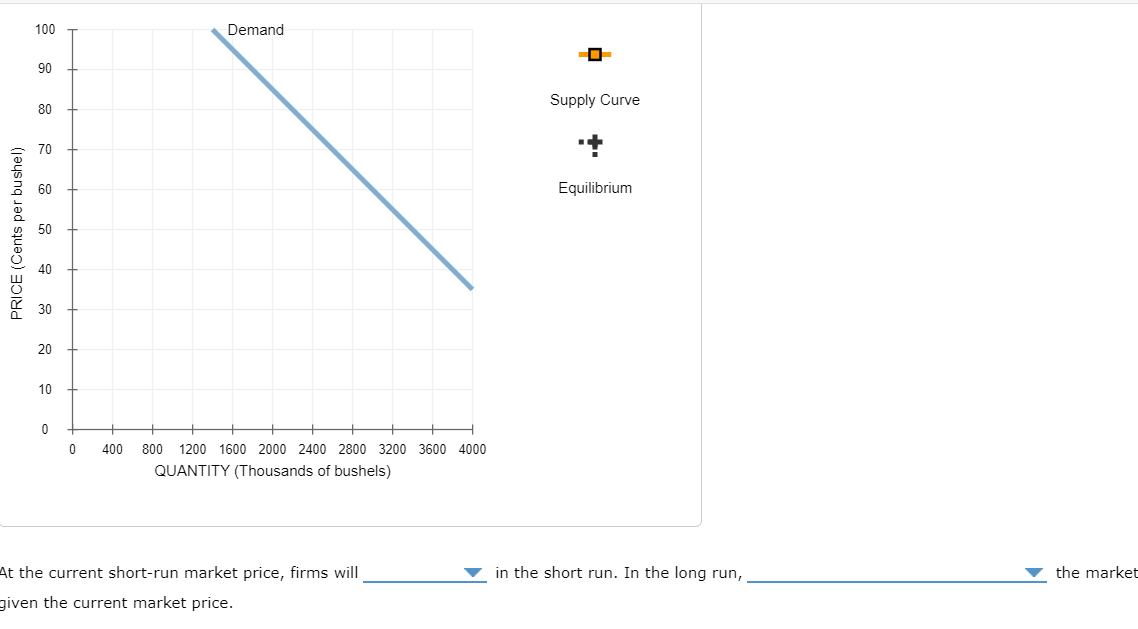

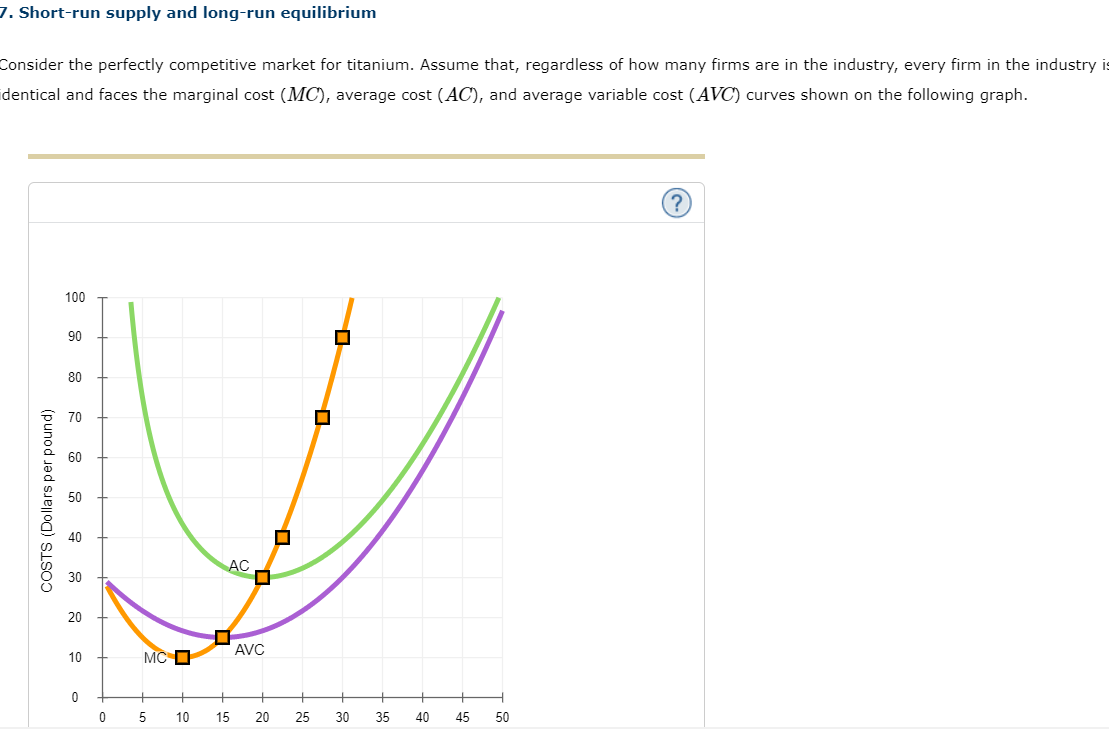

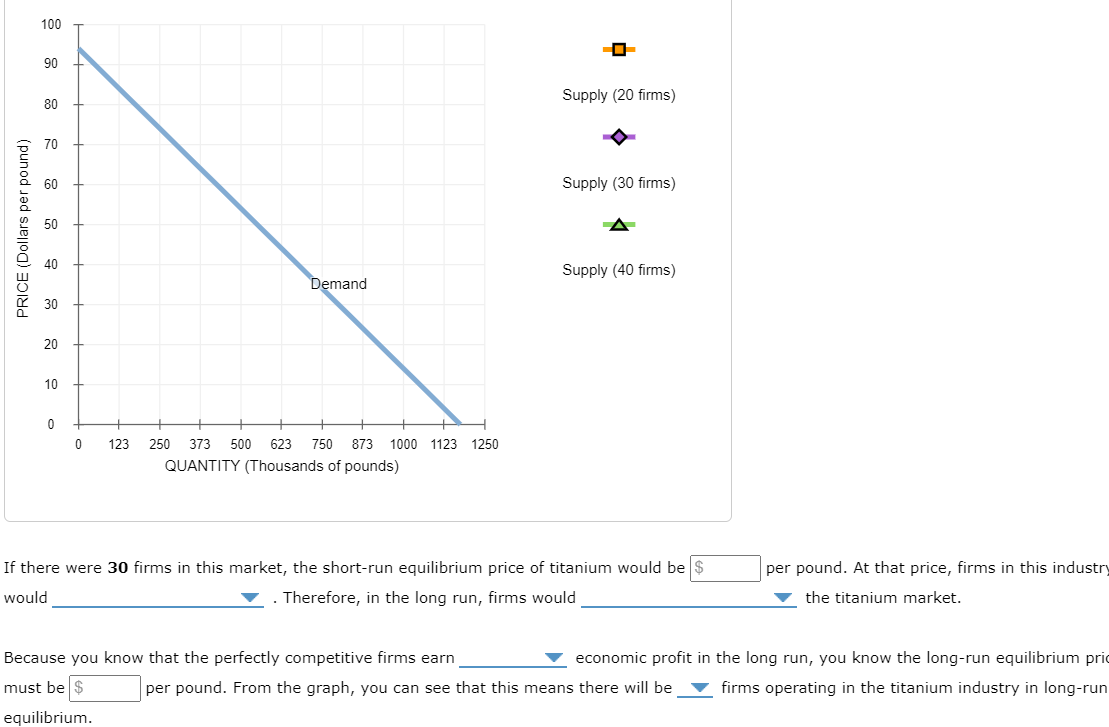

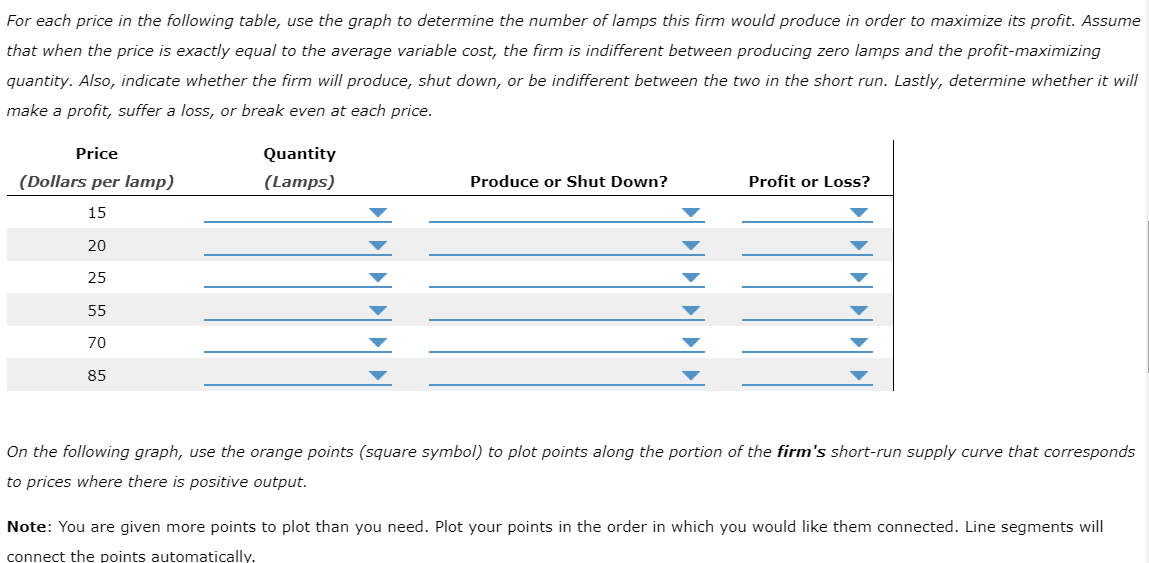

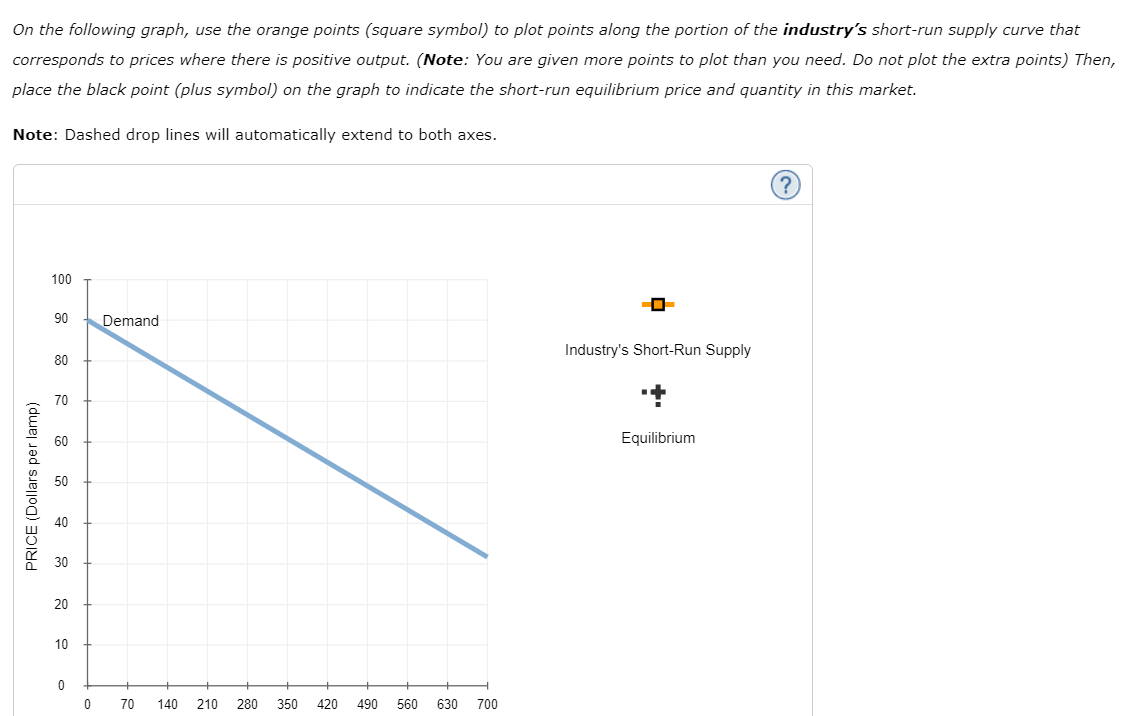

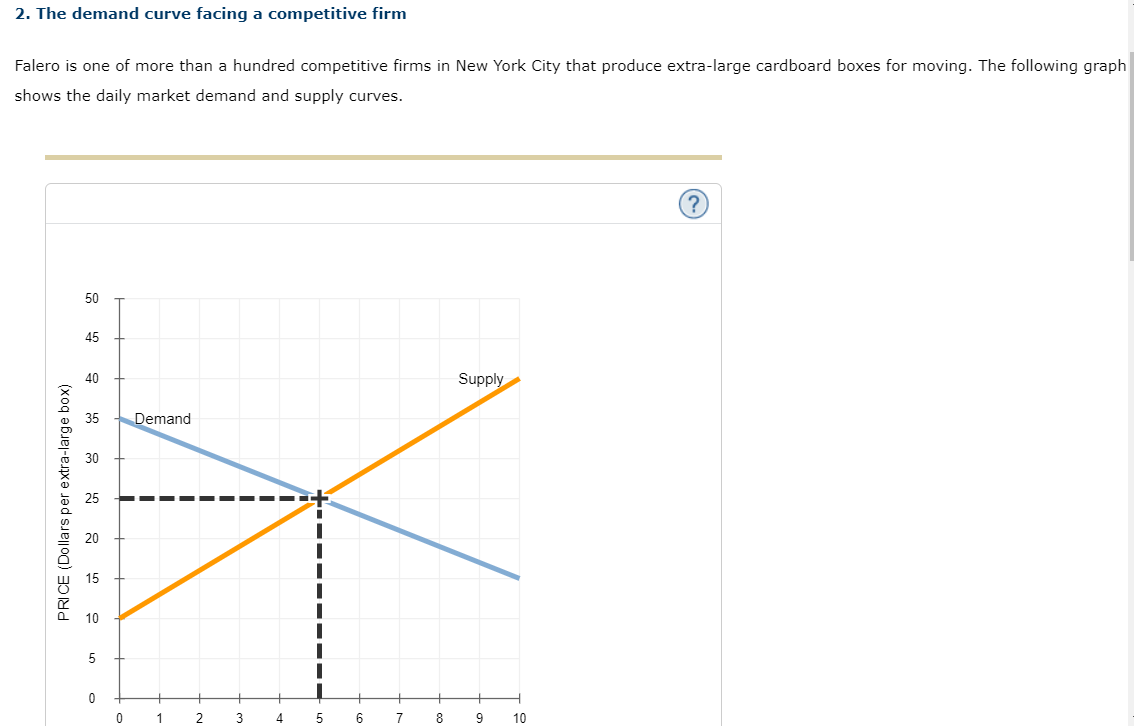

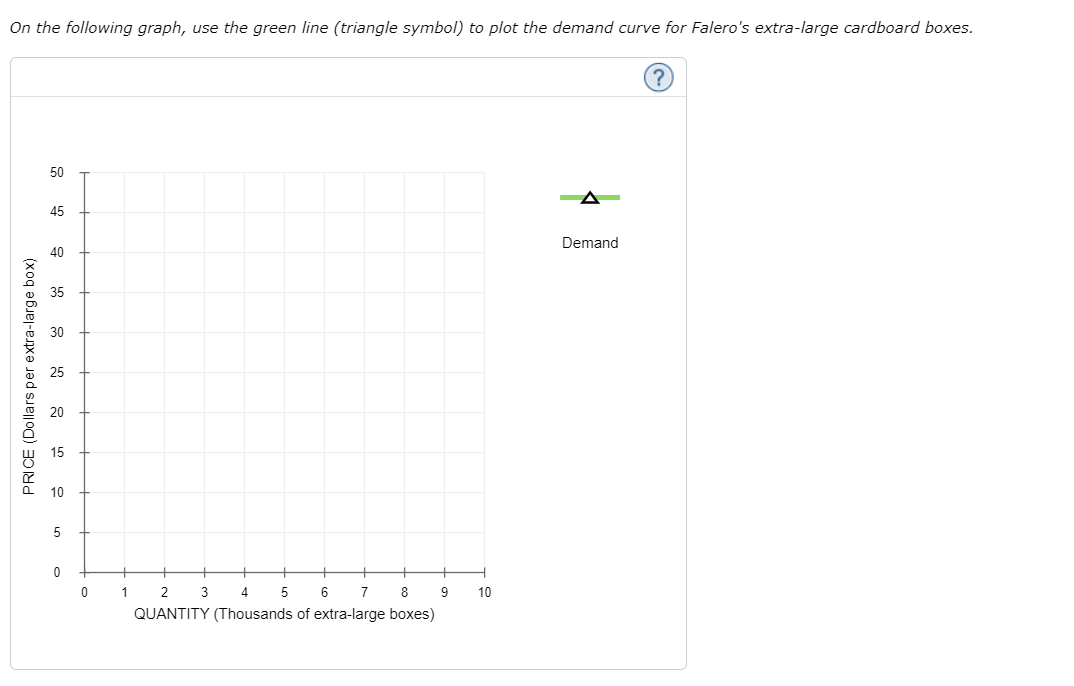

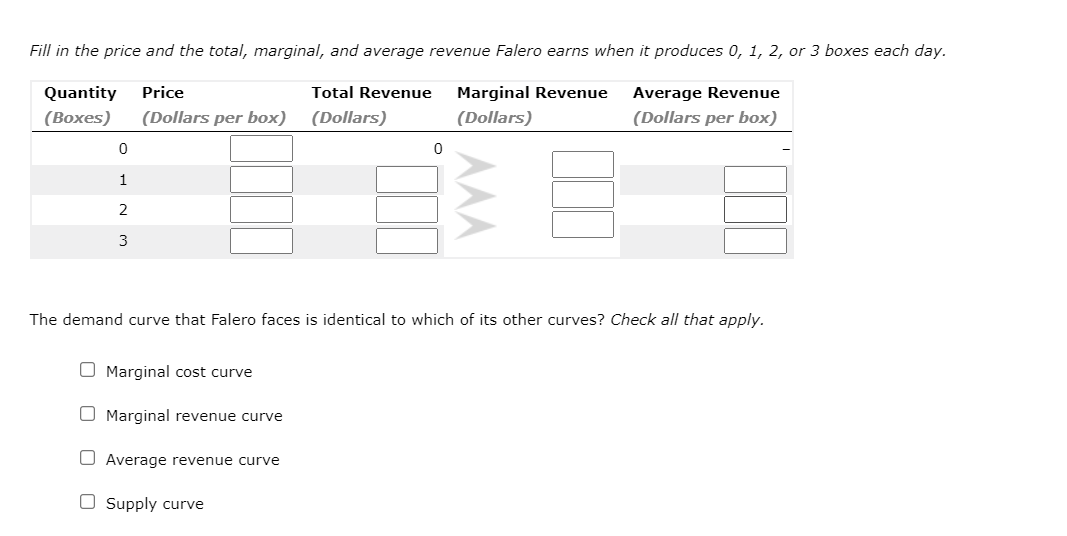

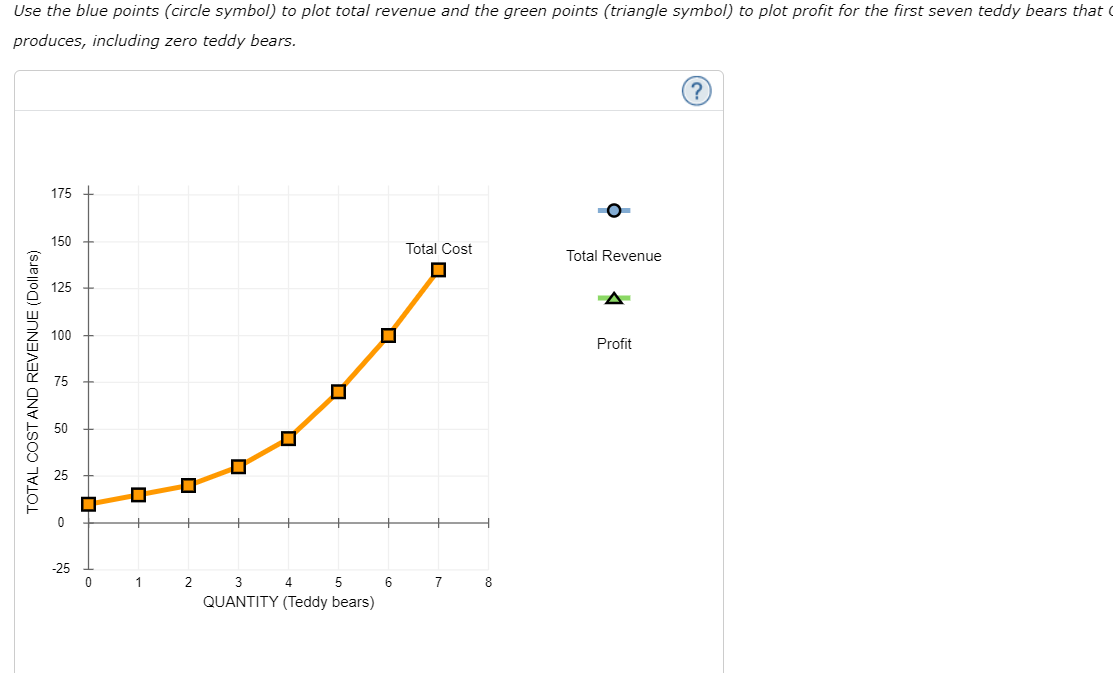

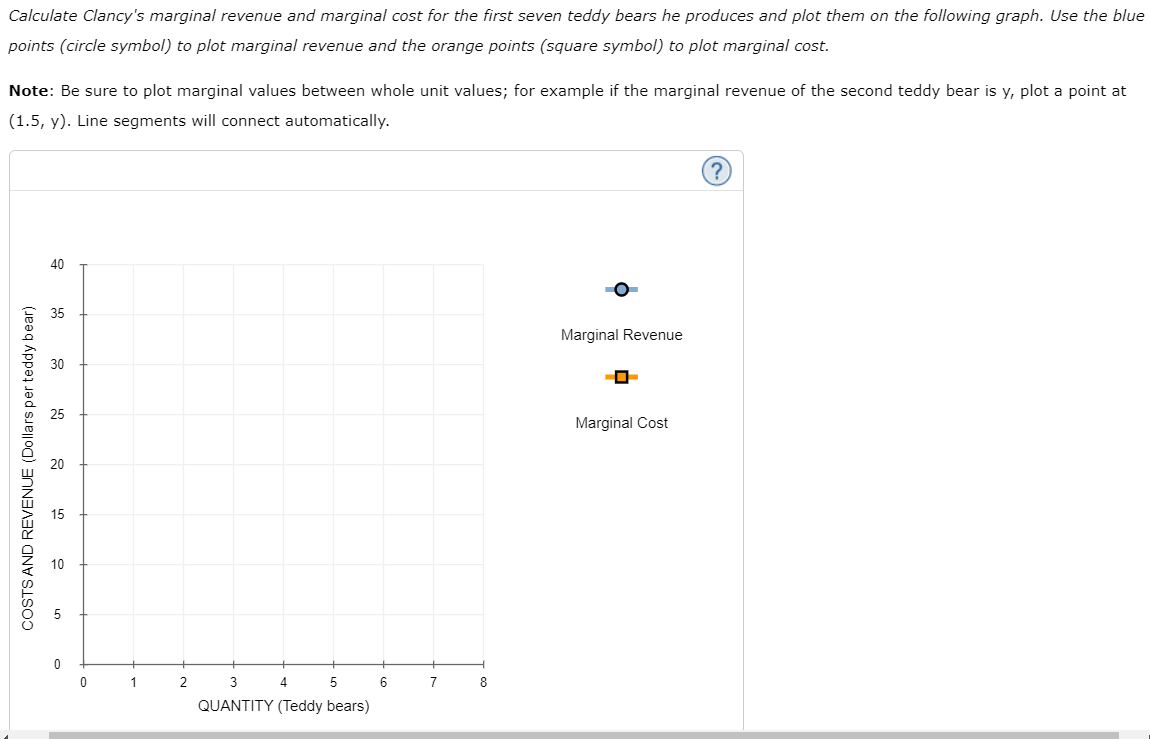

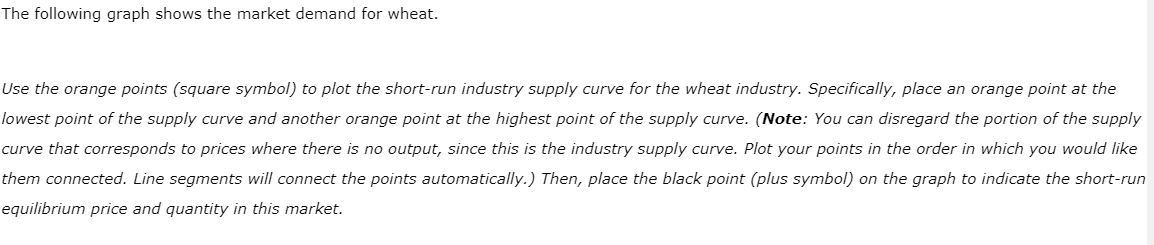

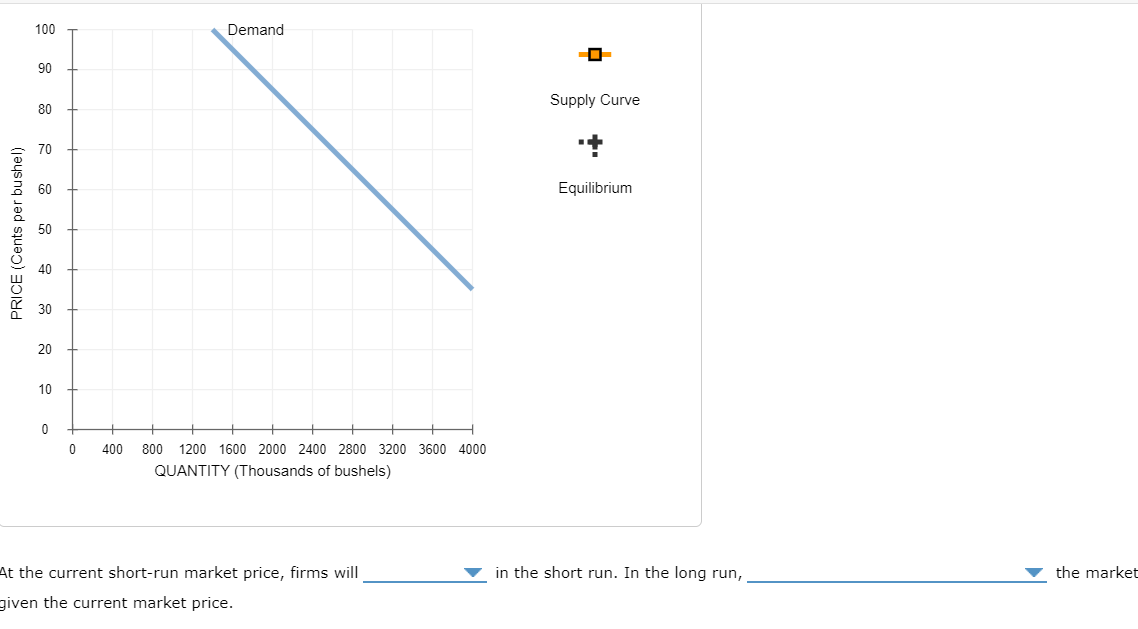

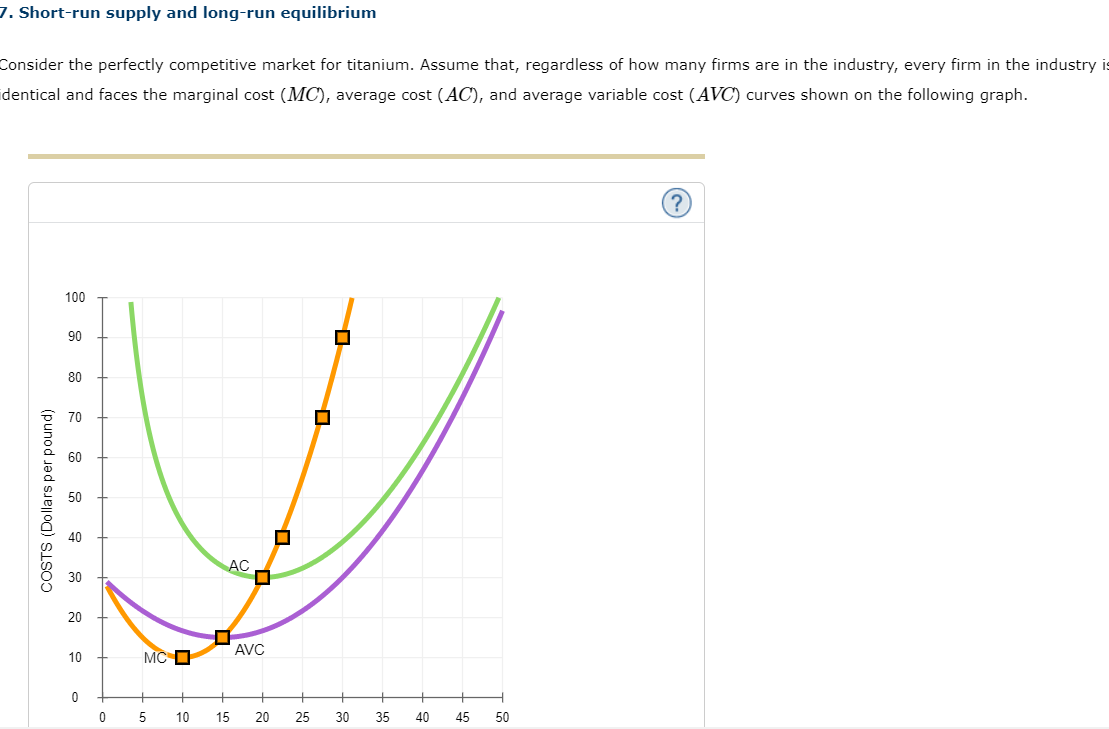

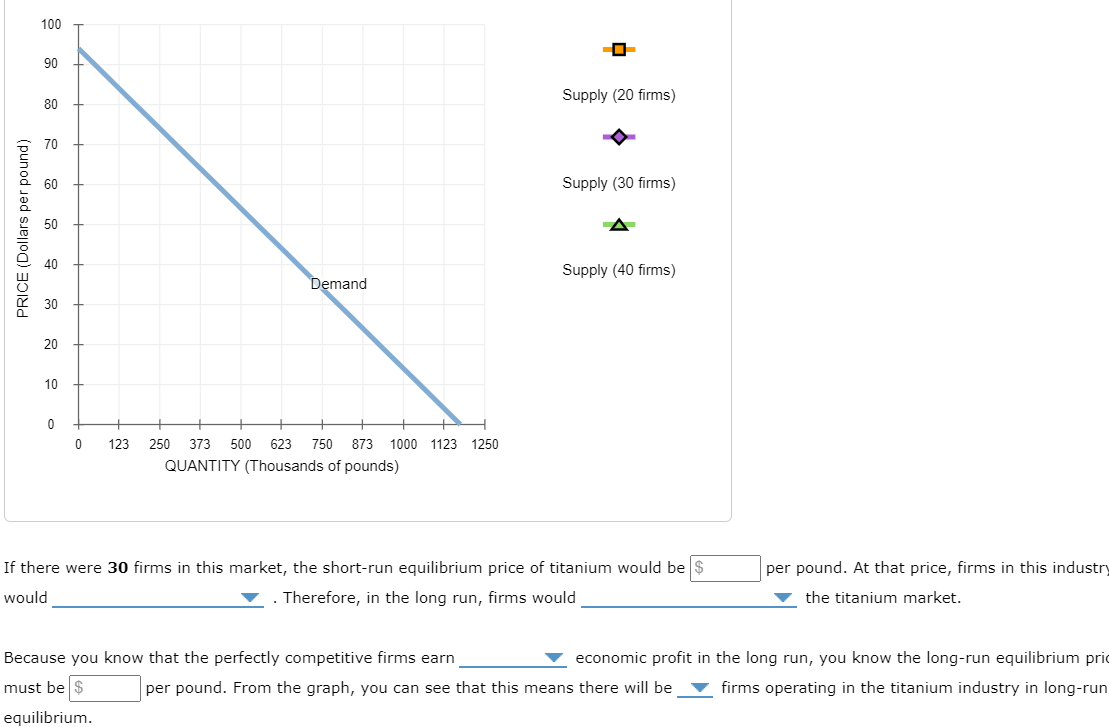

5. Deriving the short-run supply curve Consider the perfectly competitive market for halogen lamps. The following graph shows the marginal cost (M), average cost (AC), and aver variable cost (AVC) curves for a typical firm in the industry. 100 50 80 70 60 50 40 COSTS (Dollars) 30 20 10 For each price in the following table, use the graph to determine the number of lamps this firm would produce in order to maximize its profit. Assume that when the price is exactly equal to the average variable cost, the firm is indifferent between producing zero lamps and the profit-maximizing quantity. Also, indicate whether the firm will produce, shut down, or be indifferent between the two in the short run. Lastly, determine whether it will make a profit, suffer a loss, or break even at each price. Price Quantity (Dollars per lamp) (Lamps) Produce or Shut Down? Profit or Loss? 15 v w v 20 v v v 25 v w v 55 v v v 70 v w v 85 v v v On the following graph, use the orange points (square symbol) to plot points along the portion of the firm's short-run supply curve that corresponds to prices where there is positive output. Note: You are given more points to plot than you need. Plot your points in the order in which you would like them connected. Line segments will connect the points automaticallv. 100 90 80 Firm's Short-Run Supply 70 60 50 PRICE (Dollars per lamp) 40 30 20 10 0 10 20 30 40 50 60 70 80 90 100 QUANTITY (Thousands of lamps) suppose there are 7 firms in this industry, each of which has the cost curves previously shown.On the following graph, use the orange points (square symbol) to plot points along the portion of the industry's short-run supply curve that corresponds to prices where there is positive output. (Note: You are given mare points to plot than you need. Do not plot the extra points) Then, place the black point (plus symbol) on the graph to indicate the short-run equilibrium price and quantity in this market. Note: Dashed drop lines will automatically extend to both axes. 0= 90 a0 Industry's Short-Run Supply 70 + 50 Equilibrium 50 40 PRICE (Dollars per lamp) 30 + 20 + 0 + + + + + + + b + b i 0 70 140 210 280 350 420 4%0 560 630 TOO At the current short-run market price, firms will in the short run. In the long run, 2. The demand curve facing a competitive firm Falero is one of more than a hundred competitive firms in New York City that produce extra-large cardboard boxes for moving. The following graph shows the daily market demand and supply curves. 5 4 40 + Suppl 35 Demand 30 25 m - PRICE (Dollars per extra-large box) 0 o e On the following graph, use the green line (triangle symbol) to plot the demand curve for Falero's extra-large cardboard boxes. 50 A 45 Demand 40 35 30 25 PRICE (Dollars per extra-large box) 20 15 10 0 1 2 3 4 5 6 7 8 9 10 QUANTITY (Thousands of extra-large boxes)Fill in the price and the total, marginal, and average revenue Falero earns when it produces 0, 1, 2, or 3 boxes each day. Quantity Price Total Revenue Marginal Revenue Average Revenue (Boxes) (Dollars per box) (Dollars) (Dollars) (Dollars per box) 1111 L. i L, The demand curve that Falero faces is identical to which of its other curves? Check all that apply. (J Marginal cost curve O Marginal revenue curve (J Average revenue curve (J supply curve 3. Profit maximization using total cost and total revenue curves Suppose Clancy runs a small business that manufactures teddy bears. Assume that the market for teddy bears is a perfectly competitive market, . the market price is $20 per teddy bear. The following graph shows Clancy's total cost curve. Use the blue points (circle symbal) to plot total revenue and the green points (triangle symbel) to plot profit for the first seven teddy bears that C produces, including zero teddy bears. Use the blue points (circle symbol) to plot total revenue and the green points (triangle symbaol) to plot profit for the first seven teddy bears that ( produces, including zero teddy bears. @ 175 + -0~ 150 + Total Cost Total Revenue D Profit TOTAL COST AND REVENUE (Dollars) 0 1 2 3 4 5 6 7 8 QUANTITY (Teddy bears) Calculate Clancy's marginal revenue and marginal cost for the first seven teddy bears he produces and plot them on the following graph. Use the blue points (circle symbol) to plot marginal revenue and the orange points (square symbol) to plot marginal cost. Note: Be sure to plot marginal values between whole unit values; for example if the marginal revenue of the second teddy bear is v, plot a point at (1.5, y). Line segments will connect automatically. @ 40 O 35 Marginal Revenue 30 O % Marginal Cost 20 COSTS AND REVENLUE (Dellars per teddy bear) 0 1 2 3 4 5 6 7 8 QUANTITY (Teddy bears) Clancy's profit is maximized when he produces E teddy bears. When he does this, the marginal cost of the last teddy bear he produces is , which is W than the price Clancy receives for each teddy bear he sells. The marginal cost of producing an additional teddy bear (that is, one more teddy bear than would maximize his profit) is , which is W than the price Clancy receives for each teddy bear he sells. Therefore, Clancy's profit-maximizing quantity corresponds to the intersection of the W curves. Because Clancy is a price taker, this last condition can also be written as W% 6. Short-run equilibrium Consider a perfectly competitive market for wheat in Philadelphia. There are 80 firms in the industry, each of which has the cost curves shown on the following graph: Hint: Use the black point (plus symbol) to view the coordinates of the points on the AVC, AC, and MC curves. You will not be graded for any changes made to this graph. \fThe following graph shows the market demand for wheat. Use the orange points (square symbol) to plot the short-run industry supply curve for the wheat industry. Specifically, place an orange point at the lowest point of the supply curve and another orange point at the highest point of the supply curve. (Note: You can disregard the portion of the supply curve that corresponds to prices where there is no output, since this is the industry supply curve. Plot your points in the order in which you would like them connected. Line segments will connect the points automatically.) Then, place the black point (plus symbol) on the graph to indicate the short-run equilibrium price and quantity in this market. 100 Demand 90 Supply Curve 80 70 .+ 60 Equilibrium 50 PRICE (Cents per bushel) 40 30 20 10 0 0 400 800 1200 1600 2000 2400 2800 3200 3600 4000 QUANTITY (Thousands of bushels) At the current short-run market price, firms will in the short run. In the long run, the market given the current market price.7. Short-run supply and long-run equilibrium Consider the perfectly competitive market for titanium. Assume that, regardless of how many firms are in the industry, every firm in the industry i dentical and faces the marginal cost (MC), average cost (AC), and average variable cost (AVC) curves shown on the following graph. @ COSTS (Dollars per pound) 5 10 15 20 25 30 3%/ 40 45 B0 The following diagram shows the market demand for titanium. Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 20 firms in the market. (Hint: You can disregard the portion of the supply curve that correspands to prices where there is no output, since this is the industry supply curve.) Next, use t purple points (diamond symbol) to plot the short-run industry supply curve when there are 30 firms. Finally, use the green points (triangle symbc plot the short-run industry supply curve when there are 40 firms. 100 + 'o 90 30 Supply (20 firms) = 70 -0~ c 3 o 60 Supply (30 firms) a8 u 5 50 A o 9 4 o Supply (40 firms) o T 30 + 20 + 10 + 0 = t t } } 1 } } t t i 0 123 250 373 500 23 750 873 1000 M23 1250 QUANTITY (Thousands of pounds) If there were 30 firms in this market, the short-run equilibrium price of titanium would be per pound. At that price, firms in this industry would W . Therefore, in the long run, firms would W the titanium market. Because you know that the perfectly competitive firms earn w economic profit in the long run, you know the long-run equilibrium pric must be per pound. From the graph, you can see that this means there will be 9 firms operating in the titanium industry in long-run equilibrium. True or False: Each of the firms operating in this industry in the long run earns positive accounting profit. O True O False1. Efficiency, inefficiency, and equity Shen and Valerie are 13-year-old twins who are fighting over how to spend a $200 gift certificate they jointly won in a raffle. The gift certificate is for = store that sells MP3 players. There are three kinds of MP3 players available: one that costs $150, one that costs $100, and one that costs $50. Each twin wants his or her own MP3 player. Both twins greatly prefer the $100 player to the $50 player, but they only slightly prefer the $150 player to the %100 player. The gift certificate can be used only once, regardless of whether or not the full $200 value is redesmed. Suppose their mother intervenes and uses the gift certificate to purchase each twin the $100 player. This outcome is becauseboth twins can be made better off without making either twin worse off neither twin can be made better off without making the other twin worse off 2. Public interest and price changes When the price of a good increases, it undoubtedly hurts individual consumers, since they now have to pay more for a particular good. However, there are some cases in which a price increase can actually serve the public interest. Which of the following is an example of a price increase that serves the public interest? Check all that apply. (J The entrance price of national parks is increased in an effort to reduce congestion and pollution. (J Depletion of oil resources causes the price of gas to increase, reducing the consumption of gasoline. (J The Pentagon pays $435 for a hammer because of a bureaucratic procurement process. One of the three basic coordination tasks an economy has to face is In a free-market system, the preceding question is answered by: O Democratic voting O The price mechanism O Central planning

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance