Answered step by step

Verified Expert Solution

Question

1 Approved Answer

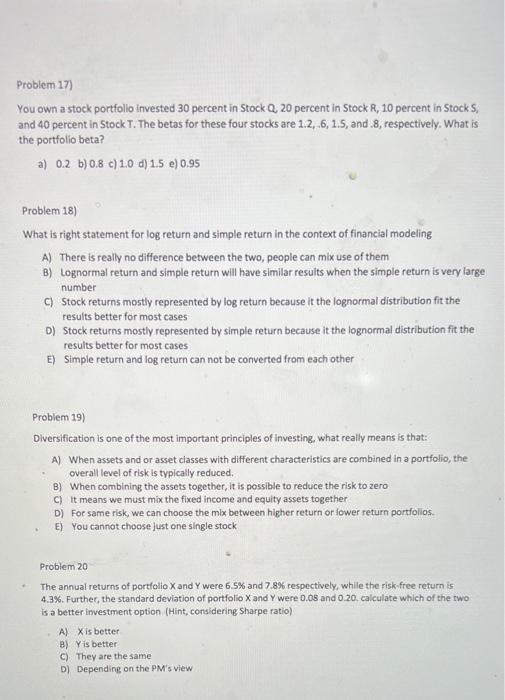

Please answer all the questions. Problem 17) You own a stock portfolio invested 30 percent in Stock Q, 20 percent in Stock R, 10 percent

Please answer all the questions.

Problem 17) You own a stock portfolio invested 30 percent in Stock Q, 20 percent in Stock R, 10 percent in Stocks, and 40 percent in Stock T. The betas for these four stocks are 1.2 .6,1.5, and.8, respectively. What is the portfolio beta? a) 0.2 b) 0.8 c) 1.0 d) 1.5 e) 0.95 Problem 18) What is right statement for log return and simple return in the context of financial modeling A) There is really no difference between the two people can mix use of them B) Lognormal return and simple return will have similar results when the simple return is very large number C) Stock returns mostly represented by log return because it the lognormal distribution fit the results better for most cases D) Stock returns mostly represented by simple return because it the lognormal distribution fit the results better for most cases E) Simple return and log return can not be converted from each other Problem 19) Diversification is one of the most important principles of investing, what really means is that: A) When assets and or asset classes with different characteristics are combined in a portfolio, the overall level of risk is typically reduced B) When combining the assets together, it is possible to reduce the risk to zero C) it means we must mix the fixed income and equity assets together D) For same risk, we can choose the mix between higher return or lower return portfolios. E) You cannot choose just one single stock - Problem 20 The annual returns of portfolio X and Y were 6.5% and 7.8% respectively, while the risk-free return is 4.3%. Further, the standard deviation of portfolio X and Y were 0.08 and 0.20. calculate which of the two is a better investment option (Hint, considering Sharpe ratio) A) X is better B) Y is better c) They are the same D) Depending on the PM's view Problem 17) You own a stock portfolio invested 30 percent in Stock Q, 20 percent in Stock R, 10 percent in Stocks, and 40 percent in Stock T. The betas for these four stocks are 1.2 .6,1.5, and.8, respectively. What is the portfolio beta? a) 0.2 b) 0.8 c) 1.0 d) 1.5 e) 0.95 Problem 18) What is right statement for log return and simple return in the context of financial modeling A) There is really no difference between the two people can mix use of them B) Lognormal return and simple return will have similar results when the simple return is very large number C) Stock returns mostly represented by log return because it the lognormal distribution fit the results better for most cases D) Stock returns mostly represented by simple return because it the lognormal distribution fit the results better for most cases E) Simple return and log return can not be converted from each other Problem 19) Diversification is one of the most important principles of investing, what really means is that: A) When assets and or asset classes with different characteristics are combined in a portfolio, the overall level of risk is typically reduced B) When combining the assets together, it is possible to reduce the risk to zero C) it means we must mix the fixed income and equity assets together D) For same risk, we can choose the mix between higher return or lower return portfolios. E) You cannot choose just one single stock - Problem 20 The annual returns of portfolio X and Y were 6.5% and 7.8% respectively, while the risk-free return is 4.3%. Further, the standard deviation of portfolio X and Y were 0.08 and 0.20. calculate which of the two is a better investment option (Hint, considering Sharpe ratio) A) X is better B) Y is better c) They are the same D) Depending on the PM's view Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Financial Diet A Total Beginners Guide To Getting Good With Money

Authors: Chelsea Fagan, Lauren Ver Hage

1st Edition

1250176166, 978-1250176165