Question: Please answer all the questions. Thanks. Based on Exhibi 6-9 (Schedule A; Itemized deductions), Also attached: . 2017 Schedule A (same as Exhibit 6-9) 2018

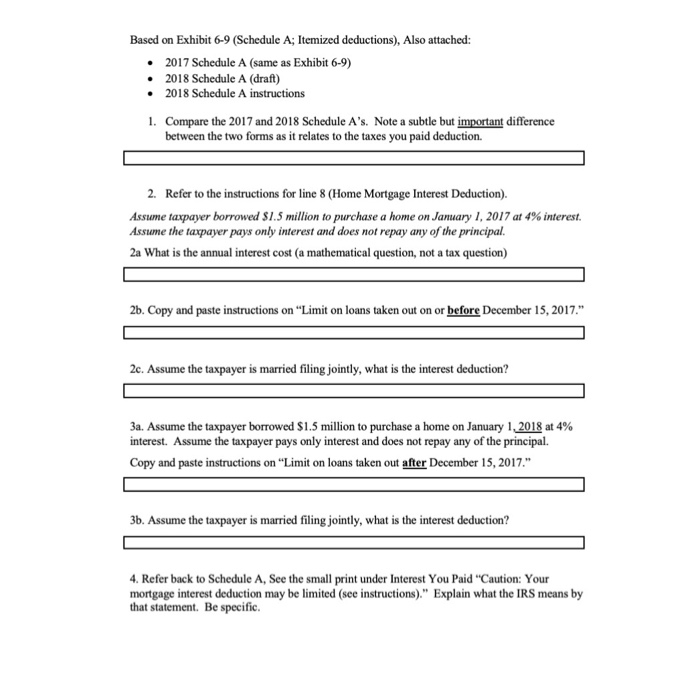

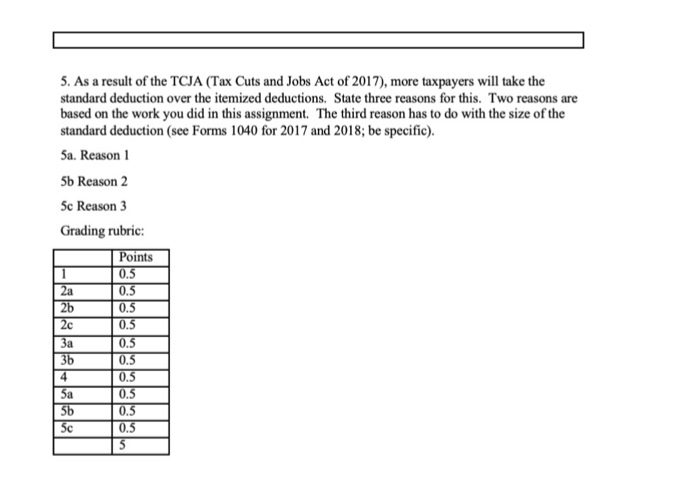

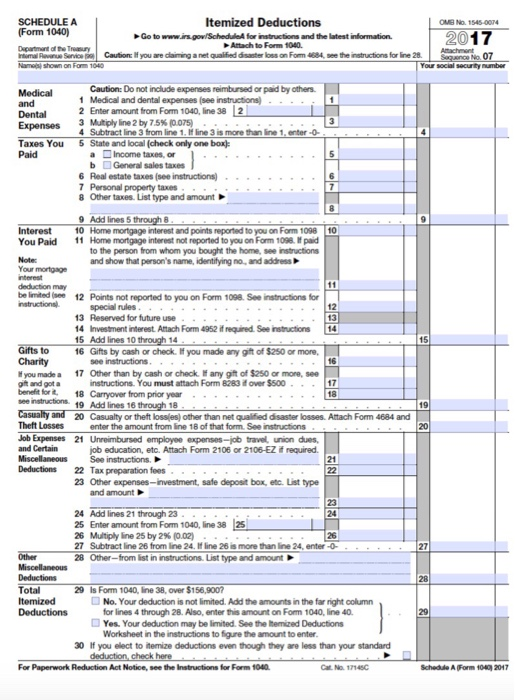

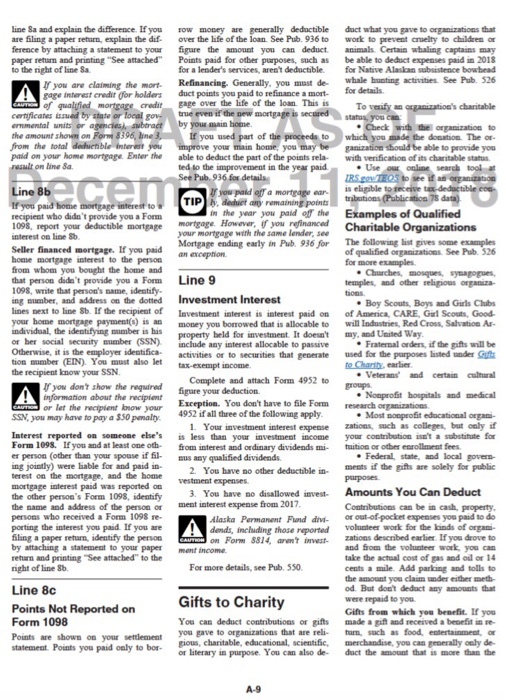

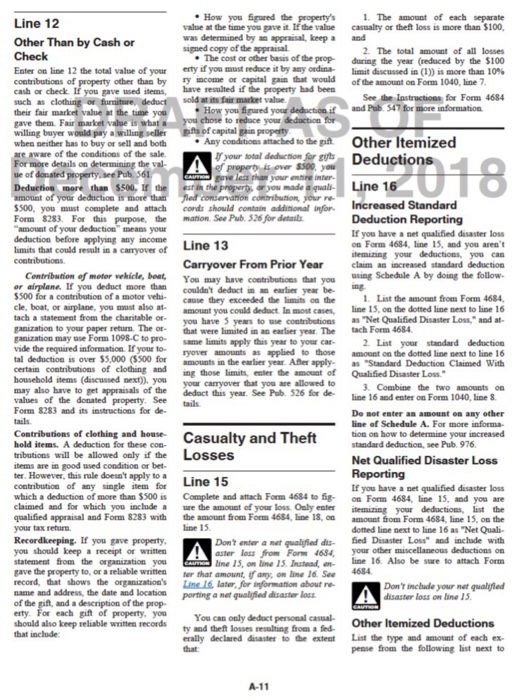

Based on Exhibi 6-9 (Schedule A; Itemized deductions), Also attached: . 2017 Schedule A (same as Exhibit 6-9) 2018 Schedule A (draft) 2018 Schedule A instructions 1. Compare the 2017 and 2018 Schedule A's. Note a subtle but important difference between the two forms as it relates to the taxes you paid deduction. 2. Refer to the instructions for line 8 (Home Mortgage Interest Deduction). Assume taxpayer borrowed $1.5 million to purchase a home on January 1, 2017 at 4% interest. Assume the taxpayer pays only interest and does not repay any of the principal. 2a What is the annual interest cost (a mathematical question, not a tax question) 2b. Copy and paste instructions on "Limit on loans taken out on or before December 15, 2017." 2c. Assume the taxpayer is married filing jointly, what is the interest deduction? 3a Assume the taxpayer borrowed $1.5 million to purchase a home on January 1,2018 at 4% interest. Assume the taxpayer pays only interest and does not repay any of the principal. Copy and paste instructions on "Limit on loans taken out after December 15, 2017." 3b. Assume the taxpayer is married filing jointly, what is the interest deduction? Refer back to Schedule A, See the small print under Interest You Paid "Caution: Your mortgage interest deduction may be limited (see instructions)." Explain what the IRS means by that statement. Be specific. 5. As a result of the TCJA (Tax Cuts and Jobs Act of 2017), more taxpayers will take the standard deduction over the itemized deductions. State three reasons for this. Two reasons are based on the work you did in this assignment. The third reason has to do with the size of the standard deduction (see Forms 1040 for 2017 and 2018; be specific). 5a. Reason 1 5b Reason 2 Sc Reason 3 Grading rubric: Points 0.5 2b 0.5 3b 0.5 0.5 0.5 0.5 0.5 0.5 5a 5b 5c SCHEDULE A (Form 1040) Itemized Deductions 15450014 2017 Attach to Form 1040 Namoi shown on Fom 1040 Your social security number Caution: Do not include expenses reimbursed or paid by others 1 Medical and dental expenses (see instructions 2 Enter amount from Form 1040, line 38 2 and Dental Expenses Taxes You Paid 3Mtphy line 2 by 7.5% 0.075) 4 Subtract line 3 from line 1. It line 3 is more than line 1, enter-0 5 State and local (check only one box a Income taxes, or b General sales taxes 6 Real estate taxes (see instructions) . . . . . . . 7 Personal property taxes 8 Other taxes. List type and amount 9 Add lines 5 through Interest 10 Home mortgage interest and points reported to you on Form 1098 10 You Paid 11 Home mortgage interest not reported to you on Form 1098. paid to the person from whom you bought the home, see instruactions and show that person's name, identifying no, and address Your mortgage be limited (see 12 Points not reported to you on Form 1098. See instructions for special rules 13 Reserved for future use 14 Investment interest. Antach Form 4952 if required. See instructions 15 Add lines 10 through 14 13 14 15 Gifts to 16 Gifts by cash or check. If you made any gift of $250 or more, Charity see instructions lfyou made a 17 Other than by cash or check lfany gft of$250 or more, see gft and got a benefit for 18 Carryover from prior year see instructions instructions. You m ust attach Form 8263 ver $500 18 19 Add lines 16 through 18 19 Casuality and 20 Casualty or theft loss(es) other than net qualified disaster losses. Attach Form 4684 and Theft Losses enter the amount from ine 18 of that form. See instructions 20 Job Expenses 21 Unreimbursed employee expenses-job travel, union dues, and Certain job education, etc. Attach Form 2106 or 2106-EZ required. See instructions, D 22 Tax preparation fees 23 Other expenses-investment, safe deposit box, etc. List type Miscellaneous Deductions 21 and amount 23 24 Add lines 21 through 23 25 Enter amount from Form 1040, line 38 25 26 Multply line 25 by 2% (002) 27 Subtract ine 26 from Ine 24. If ine 26 is more than Ine 24, enter 28 Other-from list in instructions. List type and amount 27 Total Itemized Deductions 29 Is Form 1040, line 38, over $156,9007 No. Your deduction is not limited. Add the amounts in the far right column for lines 4 through 28. Also, enter this amount on Form 1040, line 40 Yes. Your deduction may be limited. See the merged Deductions Worksheet in the instructions to figure the amount to enter 30 If you elect to itemize deductions even though they are less than your standard For Paperwork Reduction Act Notice, see the Instructions for Form 1040 Cat No. 17145C Schedule A (Form 1040) 2047 Caution: DRAFT-NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy Do not file draft forms. Also, do not rely on draft forms, instructions, and publications for filing. We generally do not release drafts of forms until we believe we have incorporated all changes. However, unexpected issues sometimes arise, or legislation is passed, necessitating a change to a draft form. In addition, forms generally are subject to OMB approval before they can be officially released. Drafts of instructions and publications usually have at least some changes before being officially released Early release drafts are at IRS.gov/DraftForms, and may remain there even after the final release is posted at information about all forms, instructions, and pubs is at IRS.gov/Forms All Almost every form and publication also has its own page on IRS.gov. For example, the Form 1040 page is at IRS.gov/Form1040: the Publication 17 page is at IRS.gov/Pub17: the Form W-4 page is at IRS.gov/W4: and the Schedule A (Form 1040) page is at IRS.gov/ScheduleA. If typing in a link above instead of clicking on it, be sure to type the link into the address bar of your browser, not in a Search box. Note that these are friendly shortcut links that will automatically go to the actual link for the page. If you wish, you can submit comments about draft or final forms, instructions, or publications at IRS.gov/FormsComments. We cannot respond to all comments due to the high volume we receive. Please note that we may not be able to consider many suggestions until the subsequent revision of the product. SCHEDULE A (Form 1040) Depatment of the Te Itemized Deductions OMB No. 1545-0074 2018 Serce 07 Go to www.irs-gov SchedulaA for instructions and the latest information. Attach to Form 1040. htm Rwarun Serce ya caution: If youare ciammng a netqualfied disaster oss on Form 4684, soe te nstruct br ie 16. Cauion: Do not include expenses reimbursed or paid by others and Dental Expenses 2 Enter amount from Form 1040, line 7 2 3 Multply ine 2 by 7.5%(0.075- 4 Subtract line 3 from line 1. I line 3 is more than l line 1, enter Taxes You Paid State and local taxes State and local income taxes or general sales taxes. You may include ether income tax but not both. If you elect to include general sales taxes instead of income taxes, check this box 8 2 general sales taxes on line 5a. b State and local real estate taxes (see instructions) o State and local personal property taxes d Add lines 5a through 5c eEnter the smaller of line 5d or $10.000 ($5,000 if married filing 50 6d 6 Other taxes. List type and amount Add lines Se and 6 Home mortgage interest and points. If you didn't use all of your 7 Interest You Paid Caution 8 home mortgage loanis) to buy, build, or improve your home, orsee instructions and check this box duction may be aHome mortgage interest and points reported to you on Form 1098 b Home mortgage interest not reported to you on Form 1098. I paid to the person from whom you bought the home, see instructions and show that person's name, identifying no, and address a Points not reported to you on Form 1098. See instructions for special rules d Reserved Add lines 8a through 8c. 8d 9 Investment interest. Attach Form 4952 i required. See 10 Add lines Se and 9 10 Gifts to Charity 1Gifts by cash or check. If you made any gift of $250 or more, see instructions 12 Other than by cash or check. If any gift of $250 or more, see instructions. You must attach Form 8283 if over $500.. Ifyou made a oen rairuchiona 14 Add lines 11 through 13 Casualty and 15 Casualty and theft loss(es) from a federally declared disaster (other than net qualified Theft Losses disaster losses). Attach Form 4684 and enter the amount from line 18 of that form. See 15 Other temized Deductions 6 Other-from list in instructions. List type and amount 16 17 Add the amounts in the far right column for lines 4 through 16. Also, enter this amount on Itemized Deductions 18 If you elect to itemize deductions even though they are less than your standard Form 1040, line 17 deduction, check here For Paperwork Reduction Act Notice, see the Instructions for Form 1040 Cat No 1714C Schedde A Fom 1040 2018 Caution: DRAFT-NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy Do not file draft forms. Also, do not rely on draft forms, instructions, and publications for filing. We generally do not release drafts of forms until we believe we have incorporated all changes. However, unexpected issues sometimes arise, or legislation is passed, necessitating a change to a draft form. In addition, forms generally are subject to OMB approval before they can be officially released. Drafts of instructions and publications usually have at least some changes before being officially released. Early release drafts are at IRS.govDraftFoms, and may remain there even after the final release is posted at IRS information about all forms, instructions, and pubs is at IRS.gov/Forms. wnloadForms. Al Almost every form and publication also has its own page on IRS.gov. For example, the Form 1040 page is at IRS.gov/Form1040; the Publication 17 page is at IRS.gov/Pub17: the Form W-4 page is at IRS.gov W4: and the Schedule A (Form 1040) page is at IRS.gov/ScheduleA. If typing in a link above instead of clicking on it, be sure to type the link into the address bar of your browser, not in a Search box. Note that these are friendly shortcut links that will automatically go to the actual link for the page If you wish, you can submit comments about draft or final forms, instructions, or publications at IRS.gov/FormsComments. We cannot respond to all comments due to the high volume we receive. Please note that we may revision of the product. not be able to consider many suggestions until the subsequent More insof espeas ou be . The supplemental part of Medicare Examples of Medical and Dental Payments You Can't Deduct More information. Pub. 502 discusses expenses you can and can't surance (Medicare B). Ir also explains when capital expenses and special care D insurance dedact expenses for disabled persons. llevistne siceesaryse and for The cost of diet food Examples of Medical andise t Dental Payments You Can Deduct ment for a specific disease To the extent you weren you can deduct what you paid for ncome protec Insurance premiums for e Medical asds such as eyeglasses The Medicare tax on your wages and dental care, inclding premiums for cotact lenses, bearing aids, brestips or the Medicare tax paid as part qualified long-term care insurance con- crutches, wheelchairs, and guide tracts as defined in Pub 502 But see usch a' lasef cjie surgery @radial TIP]-ot, atlid 6 socl se rih premiums by-any self employed heal keratotomy Lodging expenses (but ot meals you voluntarily paid for Medicare o Schedule 1 (Form 1040), line 29. You while away from home to receive medi- cant deduct insurance premius paid cal care provided by a physician in with pretax dollars because the premi ospital or a medical care facility related ums aren't included in box 1 of Form(o) W-2. If you are a retired public nificant element of personal pleasure, safety officer, you can't deduct any pre recreation, or vacation in the travel miums you paid to the extent they er Don't dedact more than $50 a night for paid for with a tax-free distribution from each a physician inNursing care for a bealthy baby. you may be able to take a credit for your to a hospital, provided there was so sig- he amount you t tions for Form 2441 paid See the Instruc- megal operations or drugs Imported drugs not approved by who meets the requirements tbe US Food and Dug Administration service and other tavsas of U.S-approved drugs maufac- Nomprescription medicines, other Travel your doctor told you to take Funeral barial or cremation costs in Pub. 502 under Lodging during 2018, you were an Ambulance igible trade adjusment assis- el costs to get medical care. If you used tance (TAA) recipient, an alter your tured without FDA approval own car, you can claim what you native TAA (ATAA) recipient, reemploy spent for gas and oil to go to and from the place you received the care; or you claim 18 cents a mile. Add parking ment TAA RT Benefit Guaranty Corporation (PBGC)can AA) recpient, or Pension ertain sicotine and tolls to the amount you claim under payee, you must reduce premiumus by any amounts used to figure eitber method e Cost of breast pumps that assist lactation coverage tax credir See ine can deduct. The amount you can Medical and Acupuncharists, chiropractors, den- deduct for qualified long-term care in- tists, eye doctors, medical doctors, occusurance contracts (as defined in Pub pational therapists, osteopathic doctors,502) depends on the age, at the end of Eer the total of your medical and des- physical therapists, podiatrists, psychia 2018, of the person for whom the premi al expenses, after you reduce these ex trists, psychoanalysts (medical care on ums were paid. See the following chart ly). and psychologists pesses by any paymests received ron inserance or otber sources. See Reim IF the person was, THEN the most and whirlpool baths your doctor ordered. at the end of If adrance payments of the premi tax credit were made, or you think you may be elipible to claim a premim ax credit, ill out Form 8962 before filling out Schedule A, line 1. See Pub 502 for tests, such as fall-body scan, pregnancy test, or blood sugar test kit *Nursing help (including your share 41-50 51-60 780 how to figure your medical and dental taxes paid) If you and paid someone to do both housework, you can deduct only the cost ofthe ming belp Hospital care (incuding meals and lodging), clinic costs, and lab fees ong-term care services (see Pub. 502) A-2 Don't forget to inchde insur as a dependent because she received wa Federal estate and gift taxes. How- TIP re premiums you paid or ges of $4.150 m 2018. You can mclude on line 1 any medical and dental expen come in respect of a decedent ses you paid in 2018 for your mother. ever, see LmIS later, if you had medical and dental care. How ever, if you claimed the self employed health insurance deduction on Schedule Certain state and local tases, in- Insurance premiums for certain non cuding tax on gasoline, car inspection fees, assessments for sidewalks or other 1 (Form 1040), line 29, reduce the pre- dependents. You may miums by the amount on line 29 or dental insurance policy that also cov ers an individual who isn't your depend- mprovements to your property, tax you paid for someone else, and license fees mamage, drivers, and ance (TAA) recipient an altar under age 27), You can't deduct any nims attributable to this individual she Benefit Guaranty Corporation (PBGC) you mst complete Form 8853 earlier. However, if Line 5 had family coverage when you add this individnal to your policy and The deduction for state and local tae limited to $10.000 ($5 000 if maried on line 1 the full amount of you premiums ule A, don 't include any of the following. medical and dental insurance tases are the taxes that you inchude on lines 5a, 5b, and 5c Any amounts you inchuded on See Pub. 502 for more information orm $883, line 4 or on Form 14095 Reimbursements. If your insuranc Include taxes imposed by a U.S pos- HCTC) Reimbursement Reguest Form part of your expenses, and you paid only on lines Sa, 5b, and Sc. However, doat coverage premiums yow paid to U ine 1 only the amount you paid. If you paid that are allocable to excluded in- The Health Coverage Tax Credit company paid the provider durectly for session with your state Any qualified health insurance the amount that remained, include on include any US possession tases you Treasury HCTC for eligible coverage received a reimbursement in 201S for come months for which you received the bene medical or dental it of the advance monthly payment pro 2018, reduce your 2018 expemses by thisT gram may want to take a credir TIP for US possession tax instead Any advance monthly paynts ment in 2018 for prior year medical don't reduce your 2018 of tions for Schedule 3 (Form 1040), your health plan administrator receved dental from the IRS, as shown on Form 1099- expenses by this amount. However, if line 45, for details year and the dedaction reduced your tax Line 5a you must inclade the reimbursement in income on Schedule 1 (Fomm 1040), line 21. See Pub. 502 for details on how to figure the amount to include. Whose medical and deatal expenses ust inclade ou can elect to deduct state and local general sales taxes instead of state and local in- medical and dental bills you paid in 2018 for anyone who was one of the fol- come taxes. You can t deduct botk. State and Local Income ther when the services wereamounts that have already been exch- or when you paid for them ded from your income; so, don't inchude employer-sponsored heath insuance ums are inc Yourself and your spouse. dependents you claim on your If you doa't elect to deduct general sales Your child whom you don't claim plan (cafeteria plan) unless the premi taxes, include on line 5a the state and lo- as a dependent because of the rules for your cal income taxes listed next or separated pa Form(s) W-2. Also, doa't include any * State and local income taxes with rents. See Child of dvarced or separa- tedparents m Pub 502 far more infor- other medical and dental expenses paid held from your salary daring 2018. You bythe plan unless the amount paid is -Form(s) w-2 will ow these amo nts cluded in box 1 of your Form(s) W-2 Forms W-2G, 1099.G, 1099-R. and 1099-MISC may also show state and lo- cal income taxes withbeld mation Any person you could have claim- that person received $4,150 or State and local income taxes paid gros income er Sied a josere of Taxes You Paid in 2018 for a prior year paid with your 2017 state or local come tax retarn Dost include penalties . Any person you could have claim Taxes You Can't Deduct ed as a dependent except that you or Federal income and most excise e State and local estimated tax pay. ments made during 2018, including any part of a prior year refund that you chose else's 2018 return. unemployment (FUTA), and railroad re Example You provided over half of tirement (RRTA) taxes. to have credited to your 2018 state or lo- your mother's support but can't claim ber duties A-3 State and Local General Sales Tax Deduction Worksheet Line 5a TIP Salesa Before you begin: Se'n-tutmflalofwodat dyo1 Keep for Your Records Instead of wsing this worksheet, you can find your deduction by ing the Sales Tax Deduction Calculator at IRS ROv L. Enter yoa state peoeal sales taens rom the 2013 Optional State Sales T Table Nest. I for all of 2018, you lived only in Comectiout the Distict of Columbia Idiona Kestuky Maine, Maryland to line 2 2 Did you live in Alacka, Aninoa, Arkansas, Colorada, Georpa, linos,Loisia MMn New Yok Noth Na.E Sales Tax Tables A. Dd you locality ipose a loeal peeal sales tas in 201S Ridts of California and Nd poal ules t nte was 25%.ar 25 lfyour local potal sales tax ra.chgdor bwd Yes Enter your state peoeal sailestax rate(ohown in the tibile beading for you 5. daug 2018, see th.ihd-for Ime 6 of wudla t A-5 The table amount for State A is $500 ted table amount on line 2 of the applahat ifyou ived in more than one The table amount for State B is $400. cable worksheet your state general lecality in the same state during 2018 Example. You lived in Locality rom January 1 dhrough August 31, 201 2 (243 days), and in Locality 2 from Sep- trogh 6 for each state if yos lived in more than one local 500 24336-b1 through December 31, 20is ty in the same state during 2013 and (122 days). The table amount for Locab ty 1 is $100 The table amount for Lo- line 3 of the workheet for each locality n which you lived (except a locality fo which you ed the 2018 Optional Local Sales Tax Tables to figue your local lived during 2018 imposed a local gen your local sales tax deduction, eral sales tax, enter $467 on line 1 of figured on line 6 of the worksheet separate worksbeet for State A and Stale Locality B Enter $333 on line 1 of the State A Localuty total mumber of days in the year 365) Line 2. If you checked the "No box, enter-0. online 2, and go to lane 3 lfLine 3. Ifyou livein Californaa, check you checked the "Yes" box and lived in the "No" box if your conibined state and the same locality for all of 2018, ester local general sales tax rate as 72500% the applicable amount, based on your Otherwise,check the "Yes" box and 2018 income and fanaly sue, tom the chade on line3 onlythe part of the co 2018 Optional Local Sales Tax Tables bined ratethatus more dan 72500% Example Youlivedm Locality 1 hom Ilmary 1 ough August 31, 2018 (243 day), and Locality 2 from Sep. teole 1 ough December 31, 2018 (122 days) The local geseal sales- rate for Locality l is 1% nt rate for Locality 2 17,% You would eter lf you Ined Nevada, deck the less than" columas for your No" box if your combined state "Q666-one 3 for tbe Locality 1 585-for 6tLocality worksheet md cal general sales tax rate is 68500% Otherwise, check the Yes" box and in chade on line 3 only the part of the com bined rate that is more than 6 8500% for line 1 of the worksbeet to figure your refers to the number of dependents listed on page 1 of Form 1040 (and any con- tinuation sheets) plas you and, if you are rate changed during 2018? If you filing ajount return, your spouse If you checked the "Yes" box and your local Line lfrs lived in more than one are maniedandnot filing a jointreturn, general sales tax rate changed dunne locality te same state durm 2018. you can inchude your spose in famuly 2018, re the rate to enter on line 3yu should have completed line 1 only uze only in certam cacumstances, follows. Multiply each tax rate for ontbe fint worksheet for at state and What if your local general seles tx period it was in effect by a fraction. The What if you lived in mere than omeraor of the fraction locality? is the mumber 6for any otber locality within that state one 2018 and the denominator is the total checked "Yes" box ca e 6 of aay 365). Enter of those worksbeets, multiply line 5 of he total of the roaed tax rates o at worksbeet by the amount that you entered on line 1 for that state on the 2018, look up the table mber of days in the year ( mount for each locality you lived in by local general sales tax from January 1 Line 7. Etter oae 7 any state mio- afraction. The mumerator of the fraction rough September 30, 201S (273 days) cal geeral sales taxes paid on the fol- as the taumber of days you lived m te Therate mcreased to 1 79% for the b- lowig spected items Ifyou are com- locality during 2018 and the denomina- od from October more than one worksbeet, tor 1Stbe total number of days year (365). If you lived in more than one 1.189" on line 3, figured as follows locality in the same state and the local general sales tax rate was the same for Jaary1- each locality, enter the total of the prora eptembe 1 through December pleting in the 1, 2018 (92 days). You would etr clude the total for line 7 on ouly one 30: 100 273 365-0748 and off road vehicle). Also include any December 31: 1.75x 92/365-0441 hat state on line 2 Otherwise, complete 6 for each locality and enter each prora for a leased motor vehicle. If the state sales tax ate on these items is higher thas the groeral sales tax rate, inchade the amount of tax you wouldForeign taxes you paid on real es- you deducted the real estate taxes in the year and the dedaction reduced have paid at the general sales tax rate An aircraft or boat, but only if the Itemized charges for services to your tax. See Recoveries in Pub. 525 for specific property or persons (for exam- details on how to figure the amount to ple, a $20 monthly charge per house for inclade in income. trash collection, a $5 charge for every 1,000 gallons of water consumed, or a Line 5c tax rate was the same as the general home including a mobile bome) or substan charge for mowing a lawn that home, but only if the tax rate was the grown higber than permitted under a tead to increase the value of your Enter on lne Sc the state and local per- imposesety (for example, an assessmest to Sonal property taxes you paid, but only general sales tax directly on the sale ofa baild a new sidewalk) The cost of a if the taxes were based on value alone home or on the cost of a substantial ad p property. However, a chage Example You paid a yearly fee deductible if it is used only to maithe registration of your car. Part of the in an existing publie facility in service fee was based on the car's value and part (for example, a charge to repair an exist- w based on its weight You can deduct ing sadewalk, and any interest included only the part of the fee that was based to perform a major renovation and paid C. Under your state law, your con. inthat charge). tractor is considered your agent in the If your mortgage payments include Prepayment of nest year's property construction of te home or substantial your real estate taxes, you can include taxes. Only taxes paid2018 and as. addition or the performance of a major only the amount the mortgage company sessed prior to 2019 can be deducted for renovation. The contract mast state that achually paid to the taxing autbority in 2018. State or local law determines whether and when a property tax is as- the contractor is authorized to act in 201S If you sold your home in 2018, any sessed, which is generally when the tax- real estate tax charged to the buyer payer becomes liable for the property name and mmust follow your direc- tons on construction decisions this case, you will be considered to haveshould be shown on chased any items subject to a sales tax statement and in box 6 of any Form and to have paid the sales tax directly. 1099-S you received. This amount is Line 6 considered a refund of real estate taxes Don't incude sales taxes paid on Other Taxes Enter only one total on line 6, but list the type and amount of each tax included Include on this line income taxes you re later. Any real you received a refund of state or local general sales taxes in 2018, see Refnd estate taxes you paid at closing should be shown on your settlement statement. You must look at your real as- tax bill to decide if any paid to a foreign country and nondeducnble itemized charges,skpping tax uch as those listed earlier, are included income distributions in the bill If your taxing aurhority (or lender) doesn't furnish you a copy TIP for the foreign tax instead of a your real estate tax bill, ask for it State and Local Real Estatei You may want to take a credit for Schedule 3 (Form 1040), line 45, for Don't include taxes you paid to a US fyou are a homeowmer who re- TIP ceted assistance under a StatePrepayment of next year's property Housing Finance Agency Hard ta. Only taxes paid in 2018 and as- to 2019 can be deducted for see Pub. 2018. State or local law determines 530 for the amount you can include on whether and wben a property tax is as H Fund program or an sessed, which is generally when the tax- payer becomes liable for the property Enter aline Sbtbe state and local taxes wasn't used for business, but oaly if the rate on all real property throughout the Don't include federal estate tax on in come in respect of a decedent on this line instead, include it on line 16 Refunds and rebates. If you received a refund or rebate in 2018 of real estate taxes you paid in 2018, reduce your de- daction by the amount of the refand or rebate. If you received a refund or rebate in 2018 of real estate taxes you paid in Interest You Paid purposes. Pub. 530 explains the deduc- an earlier year, don't reduce your deducThe rules for deducting interest vary, de- tion by this amount. Instead, you must pending on wbether the loan proceeds include te refund or rebateincome are used for business, personal, or in- on Schedule 1 (Form 1040), line 21, if vestmeat activities. See Pub. 535 for Don't include the following mounts taken out after December 15, 2017, you ness merest expenses. See Pub 550 for , later, for moreformation about can only deduct home mortgage interest more information about deductingwhat interest you can include on lines 8a o up to $750,000 (5375,000 if you are married fling separately) of that debt. If you also bave qualifying debt subject to busi- you wsed any home mortage $1,000,000 limitation home terest (on your Schedule A) and interest on certain stadent loans (on Schedule 1 vestment pupose, interest you $750.000 limit for debt taken out oa or fter December 15, 2017, is reduced by the amount of your qaalafying debt sub- ject to the $1,000,000 limit. An excep- interest. tion exists for cestain loans taken out af- Pub. 936 and Pub. 970 Your deduction for bome mortgage in- er December 15, 2017, but before April the interest on the loan to each use. 1, 2018 If the exception applies, you more of the folowing lts aploan may be treated in the same man ee Pub: 936 no figure your deduc as a loan taloen out on or before Dec ber 15, 2017; see Pub. 936 for more formation about this exception moe Limit fer lean precends mot used to See Pub. 936 to figure your deduction if you have loans taken out after October 13, 1987, that exceed $750,000 5375,000 if you are married filing sepa 1987 In general, if you paid interest inmortgage interest to the extent that the 2018 that applies to any period rloan proceeds from your bome mortpage 2018, you can deduct only amounts that are used to buy, beild, or substantially apply for 2018 prove the home secung tbe loan Limir when loans exceed th. Jair qualifying debt) Make sure to check market value of the home. If the total Use Schedule A to deduct qualified home mortgage interest and investment the box on line S if you had one or more amount of all mortgages is more than 2018 wih anut the fair market value of the home, see home mortgages in standing balance and you dida't use all Pub. 936 to figure your dedaction of the loan proceeds to buy, build, or substantially improve the home. The onLine 8a to this limit is for loans takEnter on line Sa mortgage en out on or before October 13, 1987 the loan proceeds for these loans are Points reported to you on Form 1098un treated as having been used to buy less you had to use Pub. 936 to figure Housing Finance Agency Hard home. See Pub. 936 for more informa- tion about loans takes out on or before Home mortgage interest limited. If Loan program, see Pubt mount you can deduct on October 13, 1987 your hoame mortgage interest deduction is limited, only enter on line Sa the de See Pub. 936 to figure your deduction f you must check the box on line S A home mortgage is any loan that is se- Limit on loans takrn out on or be home, regardless of how the loan is la Sore December 15, 2017 For qualify Form 1098 shows any refund of over- main home or secondL ing debt taken out on or before Decem- beled. It includes first and seconed mort gages, nanced paid interest, doat reduce your deduc- only deduct home tion by the refund Instead, see the is- mortgage interest on ap to $1,000,00 sctions for Schedule 1 (Form 1040). equity loans, and re- b15, 2017, you ca ($500,000 if you ae married lingp ine 21 A home can be a house, condomini rately) of that debt. The only esception um, cooperative, mobile home, boat, or is for loans taken out on or before Octo- similar property. It must provide basic ber 13, 1987 see Pub. 936 for more in living accommodations including sleep-formation about loams taken out on or else's Form 1098 If you and at least one oth- er person (other than your spouse if fil ing jointly) were liable for and paid in- the mortgage, and the interest was reported on the other persoa's Form ing space, toilet, and cooking facilaties. before October 13, 1987 See Pub. 936 to figuse your deduction Check the bex on line S if you ha one or more home mortgages in with an outstanding balance and you didn't use all of your home mortgage proceeds from those loans to buy, build lng separately) if you have loans taken out on or before 1098 Decembe 15, 2017, hat report your share of the interest line Sb (as explained in Line 85, later) exceed $1,000,000(500,000 if you are mamied Form 1098 doess't show all interest paid. If you paid more interest to the re- or substantially improve your bome. InLt on leans takem out ftr De cipieat than is shows on Form 1098, in terest paid on home mortgage proceeds cember 15, 2017 For qualfying debt cade the larger deductible amount on A-8 line Sa and explain the difference. If you ow mopey are generally deductible duct what you gave to organizations that are filing a paper return, explain the dif. over the life of the loan See Pub. 936 to work to prevent cruelty to children o ference by attaching a statement to your figure the amount you can deduct. animals. Certain whaling captains may paper retam and printing "See attached" Points paid for other purposes, such as be able to deduct expenses pad 2018 for a lender's services, arent deductible. for Native Alaskan subsistence bowbrad to the right of line Sa the Refinancing. Generally, you must de whale buoting activities. See Pub. 526 Ort gage interest credit (for holders duct points you paid to refinance a mort- of qualifed mortage credit gage over the life of the loan. This isToey an organization's charitable cermficates isued by state or loeal g the amount shown on Form $396, line paid on your home mortgage. Enter the Check with the organization to whdyou made the donation The or- gamzairouldbe able to provide you you usedPart of the proceed, to able to deduct the part of the points rela-with verification of its charitable statu * Use onlat sease tool ted to the improvement in the year paid in the year you paid off the Examples of Qualified recipient who didn't provide you a Form 1098, report your deductible mortgage mortgage. However, if you refinaced your mortgage with the same lender, see Mortgage ending early in Pub. 936 for The following list gives some examples of qualified organizations See Pub. 526 home mortgage interest to the person from whom you bought the home and that person dida't provide you a Form Line 9 1098, write that person's name, identify ng sumber, and address on the dotted Investment Interest lines next to line Sb. If tbe recipient of Investment interest is interest paid on of Amenica CARE Gal Scouts, Good your home mortgage payment(s) ss an money you bomowedthat is allocable to win lndustnes, Red Cross, Salvation Ar- ndividual, the identifying mumber is his or her social security mumber (SSN) clude any interest allocable to Otherwise, it is the employer ideotifica activities or to securities that geerate used for the parposes listed under tion mumber (EIN). You must also let the recipient know your SSN and other seligious organiza Boy Scouts, Boys and Girls Clubs hons property beld for investment It doesnt my, and United Way Fraternal onders, if the gifts will be you don't show the required or let the recpient inow your 492f ll ture of the following sapply Complete and attach Form 4952 to figare your Exception. You don't have to file Form research organizations Veterans' and certain cural Nonprofit hospitals and medical 1. Your investment interest expense zations, such as colleges, but only if roups SSN, you may have to pay a $50 pamalty Interest reported on someone else's is less than your investment income your costribution isst a substitute for Form 1098. If you and at least onerom interest and ordinary dividends miuiion or other eerollmeat fees er person (other than your spouse if fil s any ing jointly) were liable for and paid in * Federal, state, and local gover ments if the gifts are solely 2. You have no other deductible in- public and the boe vesment expensers ersoe' Form 1os, idedfh3. You have no disallowed invest Amounts You Can Deduct ment interest expense from 2017 Contributions can be in cash, property or out-of-pocket expesses you paid to do the name and address of the person or persons who received a Form 1098 re- porting the interest you paid. If you are filing a paper return, identify the person by attaching a statement to your paper ment income return and printing See attached" to the right of line Sb dlaska Permanent Fund divi dends, on Form 8814 arent invest- volunteer work for the kinds of zations described earlie. If you drove to and from the volunteer work you can take the actual cost of gas and oil or 14 cents a mile Add parking ind tolls to the amount you claim under either meth od. But dout deduct any amounts that For more details, see Pub. 550 Points Not Reported on Gifts to Charity Gifts from which you benefit. If you You can deduct contributions or gifts made a gift and eceived a benefit re- you gave to organizations that are reli- turn, such as food, entertainment o gious, charitable, edacational, scientific, merchandise, you can generally only de- or lterary in purpose. You can also de duct the amount that is moe than the statemest Points you paid only to A-9 value of the benefit. But this rule doesa't 3. You gave gifts of property that apply to certain membership benefits increased in value or gave gits of the ine annual Gifts by Cash or Check ment of $75 or less or to certain items or benefits of token value. For details, see ts You Can't De to Enter on line 11 the total value of gifts Certain contributions that result in you made in cash or by check (inclading a credit against the taxes owed to a state ut-of pocket expenses). Example You paid $70 to a charita ble organization to attend a fund-raising dinner and the valne of the dinner was more local government. See Pub. 526 for Recordkeeping, For any cotribution made in eash regardless of the amount, you mst maintain as a record of the contributiona bank record (such as a canceled check or credit card statement) athletic eveat in the college or waivers or a written record from the charity. The written record must include the name of Travel expenses (incloding mealsthe charity, date, and amount of the com- An amount pasd to or for the Gifts of $250 or more. You can a gift of $250 or more only if you have statement from the charitable organiza ty's stadium tion showing the information in (1) and lodging) whale away from home tribution If of any property donated sonal pleasure, secaeaton, or vacation the travel keep Don't attach the record to your tax return. Instead, keep it with your other 2. Whether the organization did or didn 't give you any goods or services in retarn for your contribution. If you didDaes, fees, or bills paid to country receive any goods or services, a descrip chubs, lodges, fraternal orders, or similar Qualified tion and estimate of the value must be omps In general, you can elect to treat gifts by e Cost of raffle, bingo, or lottery cash or check as qualified contributions incladed. If you received only intangible religious benefits (such as admission to tickets But you may be able to deduct it a religious ceremony), the organization hese expenses must state this, but it doesn't have to de- later, for more infor on on gambling 2017, to certain qualified charitable or. scribe or value the benefit on line 16. See Lne 6 The gift was paid after October S, e Value of your time or services. * The gift was made for relief efforts Vale of blood given to a bloodithe disaster area of a federally de clared disaster eligible for this tax relief In figuring whether a gift is $250 or more, don't combine separate donations. bank For example, if you gave your church $25 each week for a total of $1,300, treat each $25 payment as a separate no dedaction is gift. If you made donations through pay- interest has been traesfemed roll deductions, treat each deduction The transfer of a fiuhure interest in and property. Generally, You obtained, from the qualified allowed until the entire charitable organization, a written ment that the contribution was ased (or Gifts to individuals and groups that is to be used) for relief efforts in those are operated for personal profit See Pub. 526 if you made a separate gift of $250 or more through payroll deduc-H e Gifts to foreign organizations For details, including the types of chari- However, you may be able to deduct table organizations that qualify and the gifts to certain US organizatioes that descriptions of the disaster areas eligible You must get the statement by transfer fands to foreign chanities and for this tax relief, see Pub 976 TIP the date you file your rehurn o sions) for filing your rehurn, whicheverGits certain Canadian Isaeli, and Mexican the due date (incuding exten charities See Pub. 526 for details to orgamizations engaged in to the adjusted gross income owever, certain limits is earlier. Dont attach the statement to certain political activities that are of ds- your rehurn. Instead, keep ir for your re rect financial interest to your trade or than the amount cn Form 1040, line 7 mimus all other allowable contrmbutions conds business. See section 1709) Limit on the amount you can deduet. to lobby for changes in the laws to proups whose parpFor details, see Pub. 526. See Pub. 526 to figure he amount of Gifts to civic leagues, social and Ilude any contributions that you your deduction if any of the following sports clubs, labor anions, and chambers elect to treat as qualified contributions in the total amount reported on line 11. I applies . Value of benefits seceived in co dicate the election by also entering the 1. Your cash contributions or contri- butions of ordinary income property are pection with a coatrbution to a charita amouat of your qualified coatributions more than 30% of the amount on Fom ble organization See Pub 526 for ex- onthe dotted line next to the line 11 en- 1040, line 7 2. Your gifts of capital gain property are more than 20% of tbe amount on Form 1040, line 7 . Cost of hution However, you may be able to take an edocation credit (oee line 16 and enter the total of these ex 4684, lines 32 and 3Sb, or Form 4797 Loss from other activities from Federal estate tax on income in re- *Certain urecovered investment in on line 16. If you are filing a pa line 18a per retuurn and you can't fit all your ex- penses on the dotted lines next toSchedale K-1 (Fom 1065-B). box 2 line 16, attach a statement instead show- ing the type and amount of each ex spect of a decedent of a disabled person . A deduction for amortizable bond Only the can be deducted on line le eypenses isted nextPm (for example, a dedaction alTO ler hiaiaDeductions 23 1986) ordinary loss attributable to. If yo o rectes even thou gr statt mor lowed for a bond premium or a deduction for amortizable bond mium on bonds acquired before opouses, .Pa Line 18 . Gambling losses (gambling lossesAn ordinary loss attributable to aIf you elect to itemize for state tax on include, but aren't limited to, the cost of contingent payment debt instrument or other purposes even though your itemiz (Form 1040), line 2 . Casualty and theft losses of in amounts under a claim of right if over come-producing property from Form $3,000. See Pub. 525 for details A-12 A-14 A-15 Based on Exhibi 6-9 (Schedule A; Itemized deductions), Also attached: . 2017 Schedule A (same as Exhibit 6-9) 2018 Schedule A (draft) 2018 Schedule A instructions 1. Compare the 2017 and 2018 Schedule A's. Note a subtle but important difference between the two forms as it relates to the taxes you paid deduction. 2. Refer to the instructions for line 8 (Home Mortgage Interest Deduction). Assume taxpayer borrowed $1.5 million to purchase a home on January 1, 2017 at 4% interest. Assume the taxpayer pays only interest and does not repay any of the principal. 2a What is the annual interest cost (a mathematical question, not a tax question) 2b. Copy and paste instructions on "Limit on loans taken out on or before December 15, 2017." 2c. Assume the taxpayer is married filing jointly, what is the interest deduction? 3a Assume the taxpayer borrowed $1.5 million to purchase a home on January 1,2018 at 4% interest. Assume the taxpayer pays only interest and does not repay any of the principal. Copy and paste instructions on "Limit on loans taken out after December 15, 2017." 3b. Assume the taxpayer is married filing jointly, what is the interest deduction? Refer back to Schedule A, See the small print under Interest You Paid "Caution: Your mortgage interest deduction may be limited (see instructions)." Explain what the IRS means by that statement. Be specific. 5. As a result of the TCJA (Tax Cuts and Jobs Act of 2017), more taxpayers will take the standard deduction over the itemized deductions. State three reasons for this. Two reasons are based on the work you did in this assignment. The third reason has to do with the size of the standard deduction (see Forms 1040 for 2017 and 2018; be specific). 5a. Reason 1 5b Reason 2 Sc Reason 3 Grading rubric: Points 0.5 2b 0.5 3b 0.5 0.5 0.5 0.5 0.5 0.5 5a 5b 5c SCHEDULE A (Form 1040) Itemized Deductions 15450014 2017 Attach to Form 1040 Namoi shown on Fom 1040 Your social security number Caution: Do not include expenses reimbursed or paid by others 1 Medical and dental expenses (see instructions 2 Enter amount from Form 1040, line 38 2 and Dental Expenses Taxes You Paid 3Mtphy line 2 by 7.5% 0.075) 4 Subtract line 3 from line 1. It line 3 is more than line 1, enter-0 5 State and local (check only one box a Income taxes, or b General sales taxes 6 Real estate taxes (see instructions) . . . . . . . 7 Personal property taxes 8 Other taxes. List type and amount 9 Add lines 5 through Interest 10 Home mortgage interest and points reported to you on Form 1098 10 You Paid 11 Home mortgage interest not reported to you on Form 1098. paid to the person from whom you bought the home, see instruactions and show that person's name, identifying no, and address Your mortgage be limited (see 12 Points not reported to you on Form 1098. See instructions for special rules 13 Reserved for future use 14 Investment interest. Antach Form 4952 if required. See instructions 15 Add lines 10 through 14 13 14 15 Gifts to 16 Gifts by cash or check. If you made any gift of $250 or more, Charity see instructions lfyou made a 17 Other than by cash or check lfany gft of$250 or more, see gft and got a benefit for 18 Carryover from prior year see instructions instructions. You m ust attach Form 8263 ver $500 18 19 Add lines 16 through 18 19 Casuality and 20 Casualty or theft loss(es) other than net qualified disaster losses. Attach Form 4684 and Theft Losses enter the amount from ine 18 of that form. See instructions 20 Job Expenses 21 Unreimbursed employee expenses-job travel, union dues, and Certain job education, etc. Attach Form 2106 or 2106-EZ required. See instructions, D 22 Tax preparation fees 23 Other expenses-investment, safe deposit box, etc. List type Miscellaneous Deductions 21 and amount 23 24 Add lines 21 through 23 25 Enter amount from Form 1040, line 38 25 26 Multply line 25 by 2% (002) 27 Subtract ine 26 from Ine 24. If ine 26 is more than Ine 24, enter 28 Other-from list in instructions. List type and amount 27 Total Itemized Deductions 29 Is Form 1040, line 38, over $156,9007 No. Your deduction is not limited. Add the amounts in the far right column for lines 4 through 28. Also, enter this amount on Form 1040, line 40 Yes. Your deduction may be limited. See the merged Deductions Worksheet in the instructions to figure the amount to enter 30 If you elect to itemize deductions even though they are less than your standard For Paperwork Reduction Act Notice, see the Instructions for Form 1040 Cat No. 17145C Schedule A (Form 1040) 2047 Caution: DRAFT-NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy Do not file draft forms. Also, do not rely on draft forms, instructions, and publications for filing. We generally do not release drafts of forms until we believe we have incorporated all changes. However, unexpected issues sometimes arise, or legislation is passed, necessitating a change to a draft form. In addition, forms generally are subject to OMB approval before they can be officially released. Drafts of instructions and publications usually have at least some changes before being officially released Early release drafts are at IRS.gov/DraftForms, and may remain there even after the final release is posted at information about all forms, instructions, and pubs is at IRS.gov/Forms All Almost every form and publication also has its own page on IRS.gov. For example, the Form 1040 page is at IRS.gov/Form1040: the Publication 17 page is at IRS.gov/Pub17: the Form W-4 page is at IRS.gov/W4: and the Schedule A (Form 1040) page is at IRS.gov/ScheduleA. If typing in a link above instead of clicking on it, be sure to type the link into the address bar of your browser, not in a Search box. Note that these are friendly shortcut links that will automatically go to the actual link for the page. If you wish, you can submit comments about draft or final forms, instructions, or publications at IRS.gov/FormsComments. We cannot respond to all comments due to the high volume we receive. Please note that we may not be able to consider many suggestions until the subsequent revision of the product. SCHEDULE A (Form 1040) Depatment of the Te Itemized Deductions OMB No. 1545-0074 2018 Serce 07 Go to www.irs-gov SchedulaA for instructions and the latest information. Attach to Form 1040. htm Rwarun Serce ya caution: If youare ciammng a netqualfied disaster oss on Form 4684, soe te nstruct br ie 16. Cauion: Do not include expenses reimbursed or paid by others and Dental Expenses 2 Enter amount from Form 1040, line 7 2 3 Multply ine 2 by 7.5%(0.075- 4 Subtract line 3 from line 1. I line 3 is more than l line 1, enter Taxes You Paid State and local taxes State and local income taxes or general sales taxes. You may include ether income tax but not both. If you elect to include general sales taxes instead of income taxes, check this box 8 2 general sales taxes on line 5a. b State and local real estate taxes (see instructions) o State and local personal property taxes d Add lines 5a through 5c eEnter the smaller of line 5d or $10.000 ($5,000 if married filing 50 6d 6 Other taxes. List type and amount Add lines Se and 6 Home mortgage interest and points. If you didn't use all of your 7 Interest You Paid Caution 8 home mortgage loanis) to buy, build, or improve your home, orsee instructions and check this box duction may be aHome mortgage interest and points reported to you on Form 1098 b Home mortgage interest not reported to you on Form 1098. I paid to the person from whom you bought the home, see instructions and show that person's name, identifying no, and address a Points not reported to you on Form 1098. See instructions for special rules d Reserved Add lines 8a through 8c. 8d 9 Investment interest. Attach Form 4952 i required. See 10 Add lines Se and 9 10 Gifts to Charity 1Gifts by cash or check. If you made any gift of $250 or more, see instructions 12 Other than by cash or check. If any gift of $250 or more, see instructions. You must attach Form 8283 if over $500.. Ifyou made a oen rairuchiona 14 Add lines 11 through 13 Casualty and 15 Casualty and theft loss(es) from a federally declared disaster (other than net qualified Theft Losses disaster losses). Attach Form 4684 and enter the amount from line 18 of that form. See 15 Other temized Deductions 6 Other-from list in instructions. List type and amount 16 17 Add the amounts in the far right column for lines 4 through 16. Also, enter this amount on Itemized Deductions 18 If you elect to itemize deductions even though they are less than your standard Form 1040, line 17 deduction, check here For Paperwork Reduction Act Notice, see the Instructions for Form 1040 Cat No 1714C Schedde A Fom 1040 2018 Caution: DRAFT-NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy Do not file draft forms. Also, do not rely on draft forms, instructions, and publications for filing. We generally do not release drafts of forms until we believe we have incorporated all changes. However, unexpected issues sometimes arise, or legislation is passed, necessitating a change to a draft form. In addition, forms generally are subject to OMB approval before they can be officially released. Drafts of instructions and publications usually have at least some changes before being officially released. Early release drafts are at IRS.govDraftFoms, and may remain there even after the final release is posted at IRS information about all forms, instructions, and pubs is at IRS.gov/Forms. wnloadForms. Al Almost every form and publication also has its own page on IRS.gov. For example, the Form 1040 page is at IRS.gov/Form1040; the Publication 17 page is at IRS.gov/Pub17: the Form W-4 page is at IRS.gov W4: and the Schedule A (Form 1040) page is at IRS.gov/ScheduleA. If typing in a link above instead of clicking on it, be sure to type the link into the address bar of your browser, not in a Search box. Note that these are friendly shortcut links that will automatically go to the actual link for the page If you wish, you can submit comments about draft or final forms, instructions, or publications at IRS.gov/FormsComments. We cannot respond to all comments due to the high volume we receive. Please note that we may revision of the product. not be able to consider many suggestions until the subsequent More insof espeas ou be . The supplemental part of Medicare Examples of Medical and Dental Payments You Can't Deduct More information. Pub. 502 discusses expenses you can and can't surance (Medicare B). Ir also explains when capital expenses and special care D insurance dedact expenses for disabled persons. llevistne siceesaryse and for The cost of diet food Examples of Medical andise t Dental Payments You Can Deduct ment for a specific disease To the extent you weren you can deduct what you paid for ncome protec Insurance premiums for e Medical asds such as eyeglasses The Medicare tax on your wages and dental care, inclding premiums for cotact lenses, bearing aids, brestips or the Medicare tax paid as part qualified long-term care insurance con- crutches, wheelchairs, and guide tracts as defined in Pub 502 But see usch a' lasef cjie surgery @radial TIP]-ot, atlid 6 socl se rih premiums by-any self employed heal keratotomy Lodging expenses (but ot meals you voluntarily paid for Medicare o Schedule 1 (Form 1040), line 29. You while away from home to receive medi- cant deduct insurance premius paid cal care provided by a physician in with pretax dollars because the premi ospital or a medical care facility related ums aren't included in box 1 of Form(o) W-2. If you are a retired public nificant element of personal pleasure, safety officer, you can't deduct any pre recreation, or vacation in the travel miums you paid to the extent they er Don't dedact more than $50 a night for paid for with a tax-free distribution from each a physician inNursing care for a bealthy baby. you may be able to take a credit for your to a hospital, provided there was so sig- he amount you t tions for Form 2441 paid See the Instruc- megal operations or drugs Imported drugs not approved by who meets the requirements tbe US Food and Dug Administration service and other tavsas of U.S-approved drugs maufac- Nomprescription medicines, other Travel your doctor told you to take Funeral barial or cremation costs in Pub. 502 under Lodging during 2018, you were an Ambulance igible trade adjusment assis- el costs to get medical care. If you used tance (TAA) recipient, an alter your tured without FDA approval own car, you can claim what you native TAA (ATAA) recipient, reemploy spent for gas and oil to go to and from the place you received the care; or you claim 18 cents a mile. Add parking ment TAA RT Benefit Guaranty Corporation (PBGC)can AA) recpient, or Pension ertain sicotine and tolls to the amount you claim under payee, you must reduce premiumus by any amounts used to figure eitber method e Cost of breast pumps that assist lactation coverage tax credir See ine can deduct. The amount you can Medical and Acupuncharists, chiropractors, den- deduct for qualified long-term care in- tists, eye doctors, medical doctors, occusurance contracts (as defined in Pub pational therapists, osteopathic doctors,502) depends on the age, at the end of Eer the total of your medical and des- physical therapists, podiatrists, psychia 2018, of the person for whom the premi al expenses, after you reduce these ex trists, psychoanalysts (medical care on ums were paid. See the following chart ly). and psychologists pesses by any paymests received ron inserance or otber sources. See Reim IF the person was, THEN the most and whirlpool baths your doctor ordered. at the end of If adrance payments of the premi tax credit were made, or you think you may be elipible to claim a premim ax credit, ill out Form 8962 before filling out Schedule A, line 1. See Pub 502 for tests, such as fall-body scan, pregnancy test, or blood sugar test kit *Nursing help (including your share 41-50 51-60 780 how to figure your medical and dental taxes paid) If you and paid someone to do both housework, you can deduct only the cost ofthe ming belp Hospital care (incuding meals and lodging), clinic costs, and lab fees ong-term care services (see Pub. 502) A-2 Don't forget to inchde insur as a dependent because she received wa Federal estate and gift taxes. How- TIP re premiums you paid or ges of $4.150 m 2018. You can mclude on line 1 any medical and dental expen come in respect of a decedent ses you paid in 2018 for your mother. ever, see LmIS later, if you had medical and dental care. How ever, if you claimed the self employed health insurance deduction on Schedule Certain state and local tases, in- Insurance premiums for certain non cuding tax on gasoline, car inspection fees, assessments for sidewalks or other 1 (Form 1040), line 29, reduce the pre- dependents. You may miums by the amount on line 29 or dental insurance policy that also cov ers an individual who isn't your depend- mprovements to your property, tax you paid for someone else, and license fees mamage, drivers, and ance (TAA) recipient an altar under age 27), You can't deduct any nims attributable to this individual she Benefit Guaranty Corporation (PBGC) you mst complete Form 8853 earlier. However, if Line 5 had family coverage when you add this individnal to your policy and The deduction for state and local tae limited to $10.000 ($5 000 if maried on line 1 the full amount of you premiums ule A, don 't include any of the following. medical and dental insurance tases are the taxes that you inchude on lines 5a, 5b, and 5c Any amounts you inchuded on See Pub. 502 for more information orm $883, line 4 or on Form 14095 Reimbursements. If your insuranc Include taxes imposed by a U.S pos- HCTC) Reimbursement Reguest Form part of your expenses, and you paid only on lines Sa, 5b, and Sc. However, doat coverage premiums yow paid to U ine 1 only the amount you paid. If you paid that are allocable to excluded in- The Health Coverage Tax Credit company paid the provider durectly for session with your state Any qualified health insurance the amount that remained, include on include any US possession tases you Treasury HCTC for eligible coverage received a reimbursement in 201S for come months for which you received the bene medical or dental it of the advance monthly payment pro 2018, reduce your 2018 expemses by thisT gram may want to take a credir TIP for US possession tax instead Any advance monthly paynts ment in 2018 for prior year medical don't reduce your 2018 of tions for Schedule 3 (Form 1040), your health plan administrator receved dental from the IRS, as shown on Form 1099- expenses by this amount. However, if line 45, for details year and the dedaction reduced your tax Line 5a you must inclade the reimbursement in income on Schedule 1 (Fomm 1040), line 21. See Pub. 502 for details on how to figure the amount to include. Whose medical and deatal expenses ust inclade ou can elect to deduct state and local general sales taxes instead of state and local in- medical and dental bills you paid in 2018 for anyone who was one of the fol- come taxes. You can t deduct botk. State and Local Income ther when the services wereamounts that have already been exch- or when you paid for them ded from your income; so, don't inchude employer-sponsored heath insuance ums are inc Yourself and your spouse. dependents you claim on your If you doa't elect to deduct general sales Your child whom you don't claim plan (cafeteria plan) unless the premi taxes, include on line 5a the state and lo- as a dependent because of the rules for your cal income taxes list

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts