Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer all three questions, thanks! 5. Portfolio beta and weights Rafael is an analyst at a wealth management firm, one of his clients holds

Please answer all three questions, thanks!

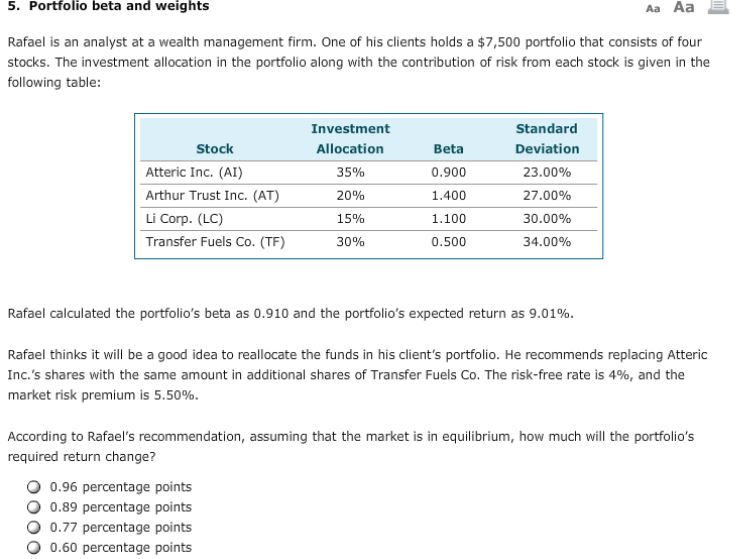

5. Portfolio beta and weights Rafael is an analyst at a wealth management firm, one of his clients holds a $7,500 portfolio that consists of four stocks. The investment allocation in the portfolio along with the contribution of risk from each stock is given in the following table Investment Allocation 35% 20% 15% 30% Standard Deviation 23.00% 27.00% 30.00% 34.00% Stock Atteric Inc. (AI) Arthur Trust Inc. (AT) Li Corp. (LC) Transfer Fuels Co. (TF) Beta 0.900 1.400 1.100 0.500 Rafael calculated the portfolio's beta as 0.910 and the portfolio's expected return as 9.01% Rafael thinksit wll be a good idea to reallocate the funds in his client's portfolio. He recommends replacing Atteric Inc.s shares with the same amount in additional shares of Transfer Fuels Co. The risk-free rate is 4%, and the market risk premium is 5.50% According to Rafael's recommendation, assuming that the market is in equilibrium, how much will the portfolio's required return change? 0.96 percentage points 0.89 percentage points O 0.77 percentage points 0.60 percentage pointsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Restaurant Financial Management

Authors: Hyung-il Jung

1st Edition

1774631431, 978-1774631430