Answered step by step

Verified Expert Solution

Question

1 Approved Answer

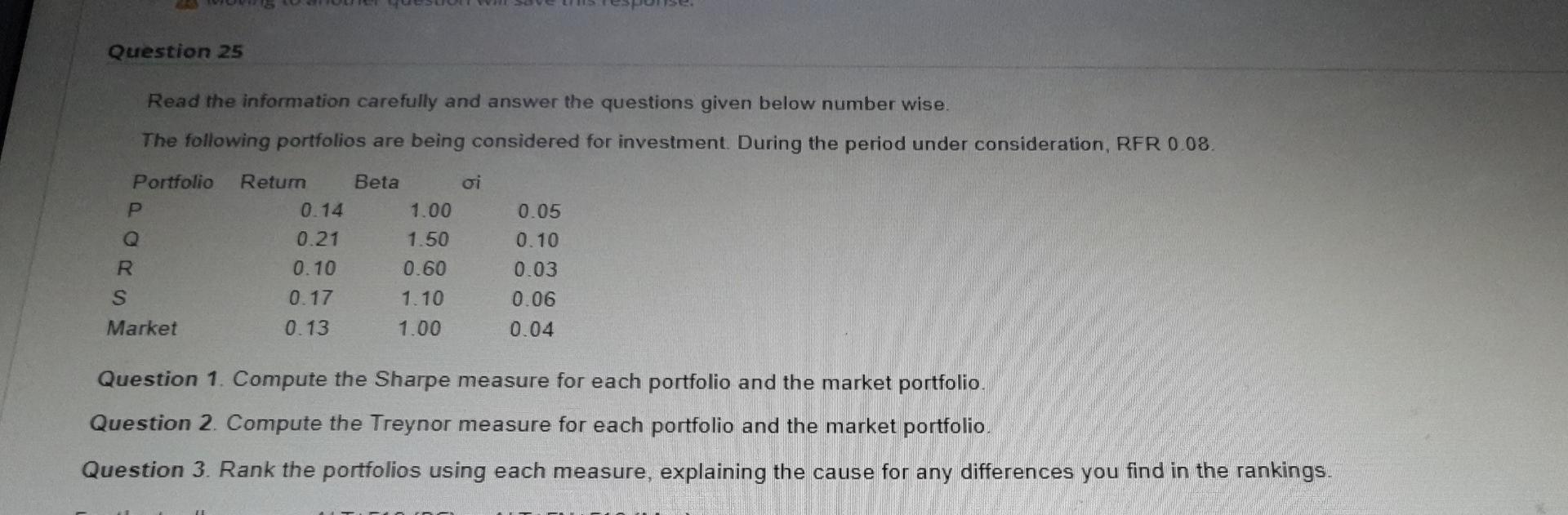

please answer ASAP Question 25 Read the information carefully and answer the questions given below number wise. The following portfolios are being considered for investment.

please answer ASAP

Question 25 Read the information carefully and answer the questions given below number wise. The following portfolios are being considered for investment. During the period under consideration, RFR 0.08. Portfolio Return Beta oi P 0.14 1.00 0.05 0.21 1.50 0.10 0.10 0.60 0.03 S 0.17 1.10 0.06 Market 0.13 1.00 0.04 Question 1. Compute the Sharpe measure for each portfolio and the market portfolio. Question 2. Compute the Treynor measure for each portfolio and the market portfolio. Question 3. Rank the portfolios using each measure, explaining the cause for any differences you find in the rankings. RStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Equity Valuation Risk And Investment A Practitioners Roadmap

Authors: Peter C. Stimes

1st Edition

0470226404, 9780470226407