Answered step by step

Verified Expert Solution

Question

1 Approved Answer

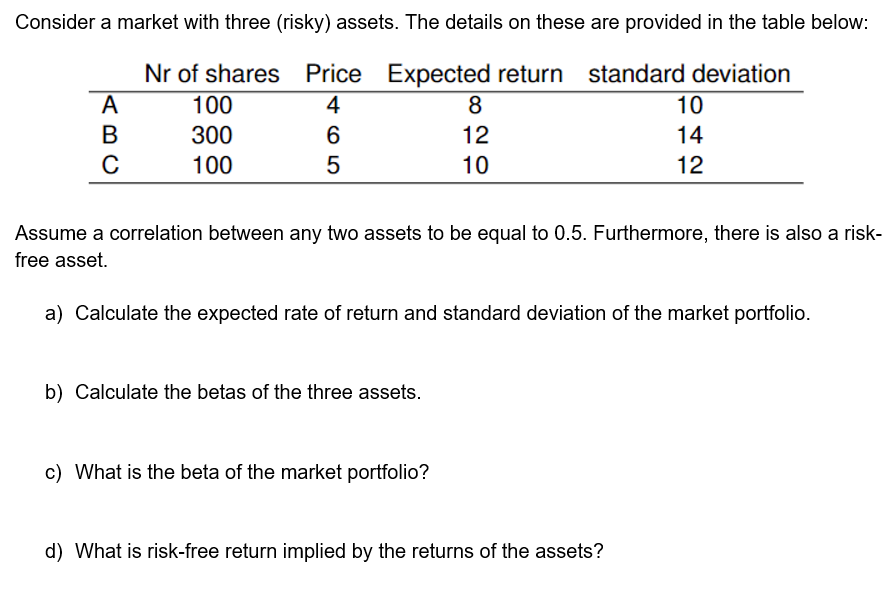

Please answer asap. Thank you in advance. Will upvote on the spot. Consider a market with three (risky) assets. The details on these are provided

Please answer asap. Thank you in advance. Will upvote on the spot.

Consider a market with three (risky) assets. The details on these are provided in the table below: Assume a correlation between any two assets to be equal to 0.5 . Furthermore, there is also a risk free asset. a) Calculate the expected rate of return and standard deviation of the market portfolio. b) Calculate the betas of the three assets. c) What is the beta of the market portfolio? d) What is risk-free return implied by the returns of the assetsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Adjusted Performance And Bank Governance Structures

Authors: Christoph Böhm

1st Edition

3631639163, 3653027306, 9783631639160, 9783653027303