Answered step by step

Verified Expert Solution

Question

1 Approved Answer

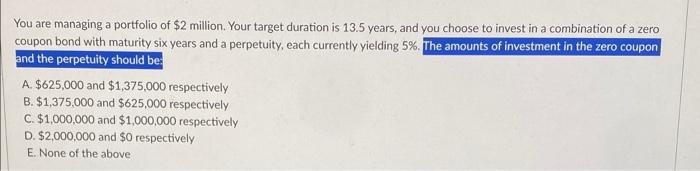

PLEASE answer ASAP! Thank you! Will like! You are managing a portfolio of $2 million. Your target duration is 13.5 years, and you choose to

PLEASE answer ASAP! Thank you! Will like!

You are managing a portfolio of $2 million. Your target duration is 13.5 years, and you choose to invest in a combination of a zero coupon bond with maturity six years and a perpetuity, each currently yielding 5%. The amounts of investment in the zero coupon and the perpetuity should be: A. $625,000 and $1,375,000 respectively B. $1,375,000 and $625,000 respectively C. $1,000,000 and $1,000,000 respectively D. $2,000,000 and $0 respectively E. None of the above Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Venture Capital And The Corporate Governance Of Chinese Listed Companies

Authors: Lin Zhang

1st Edition

1461412803,1461412811