Answered step by step

Verified Expert Solution

Question

1 Approved Answer

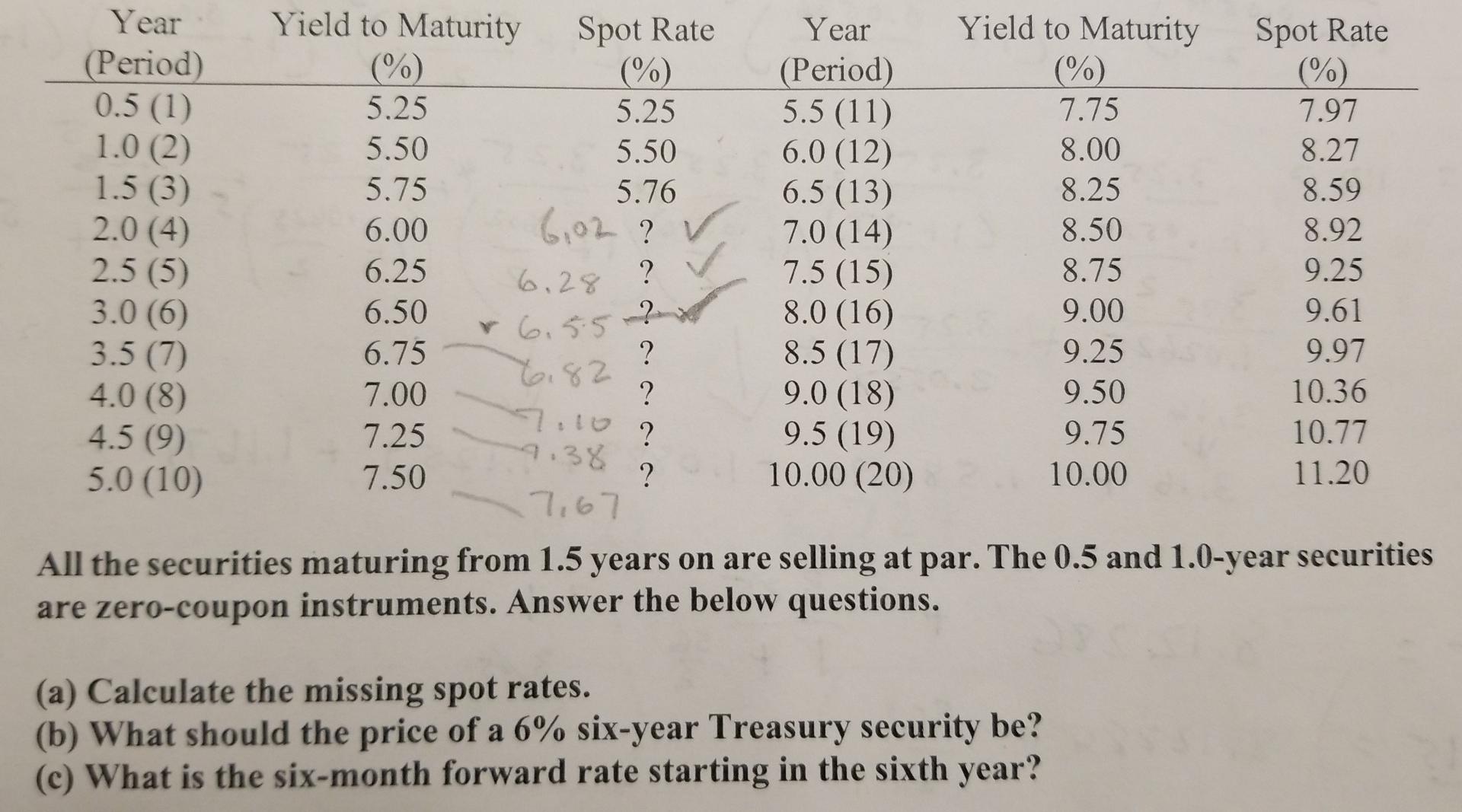

please answer b,c. show detailed work on how you got each number. I'm cant figure out those answers to b, c. thank you All the

please answer b,c. show detailed work on how you got each number. I'm cant figure out those answers to b, c. thank you

All the securities maturing from 1.5 years on are selling at par. The 0.5 and 1.0-year securities are zero-coupon instruments. Answer the below questions. (a) Calculate the missing spot rates. (b) What should the price of a 6% six-year Treasury security be? (c) What is the six-month forward rate starting in the sixth yearStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Development

Authors: Barbara Stallings

1st Edition

0815780850, 978-0815780854