Answered step by step

Verified Expert Solution

Question

1 Approved Answer

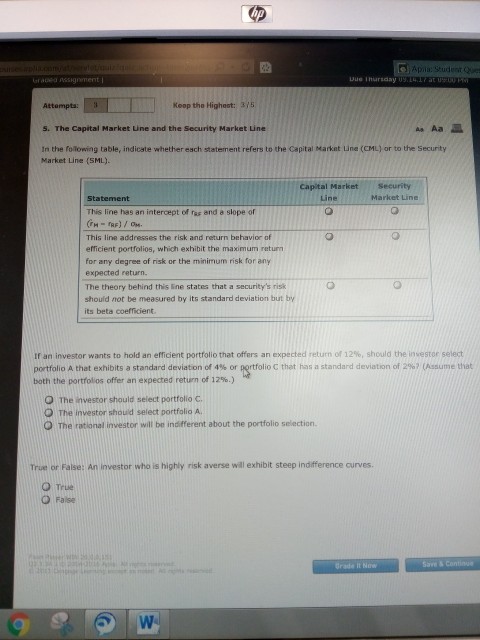

please answer completely and correctly thanks ue Thursday Attempts: ELT Keep thHighert: 3,5 5. The Capital Market ine and the Security Market Line as Aa

please answer completely and correctly thanks

ue Thursday Attempts: ELT Keep thHighert: 3,5 5. The Capital Market ine and the Security Market Line as Aa In the folowing table, indicate whether each statement refers to the Capital Markat Line (CML) or to the Security Market Line (SML). Capital Market Security Line Market Line This line has an intercept of fas and a slope of This line addresses the risk and return behavior of efficient portfolios, which exhibit the maximum return for any degree of risk or the minimum risk for any expected return. The theory behind this ine states that a security's risk should not be measured by its standard deviation but by its beta coefficient If an investor wants to hold an efficient portfolio that offers an expected return of 12%, should the investor select portfolio A that exhibits a standard deviation of 4% or Rrtfolio C that has a standard deviation of 2%? (Assume that both the portfolios offer an expected return of 12%.) O The investor should select portfolio C O The investor shouid select portfolio A O The rational investor will be indifferent about the portfolio selection True or False: An investor who is highly risk averse will exhibit steep indifference curves O True O False Grade it Novw Save&Con

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Labour Finance And Inequality

Authors: Suzanne J. Konzelmann, Simon Deakin, Marc Fovargue-Davies, Frank Wilkinson

1st Edition

1138919721, 978-1138919723