Please answer everything in 30-40mins i need to submit now its due.

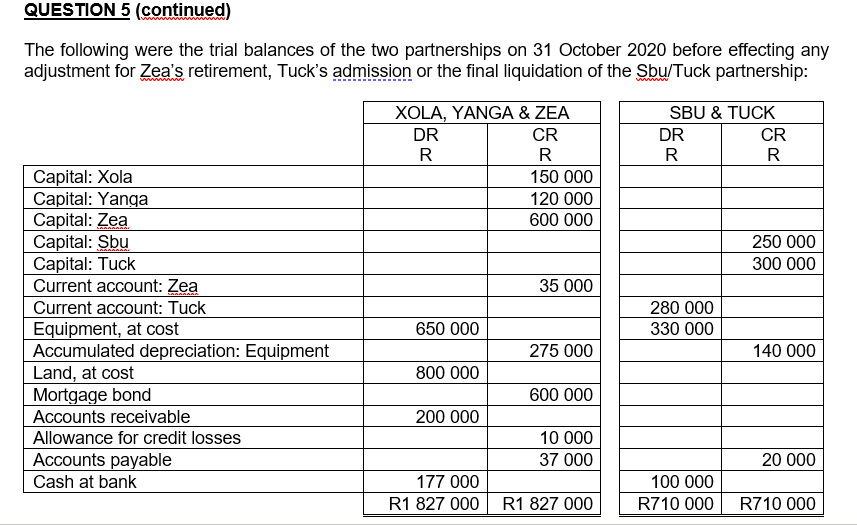

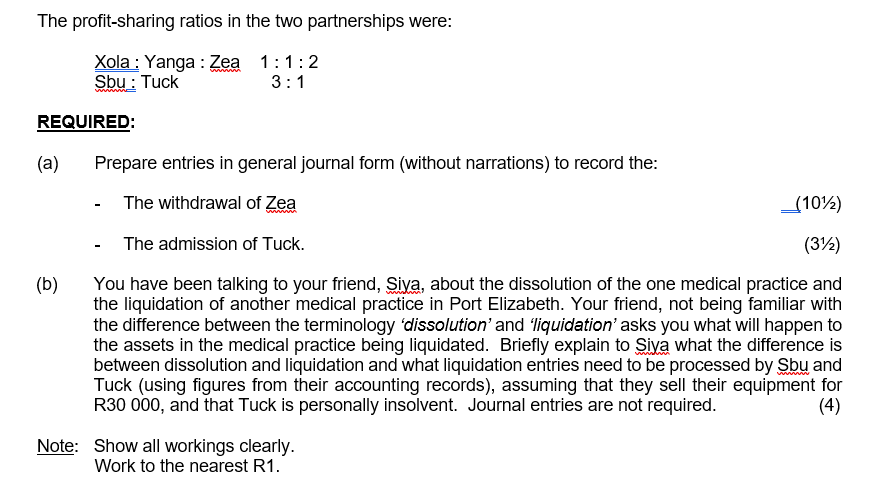

QUESTION 5 _18 marks : 32 minutes) Xola, Yanga and Zea have been in partnership for many years in a medical practice. Zea has decided to emigrate. Another medical practice in Port Elizabeth (partners: Sby and Tuck) is in the process of being liquidated. Xola and Yanga decide to replace Zea with Tuck. After lengthy negotiations, it was decided that Zea would withdraw from the partnership on 31 October 2020 and that on the same day Tuck would be admitted. As Tuck is insolvent, he is not able to contribute any tangible assets, but Xola and Yanga agree that his expertise should be accorded a value of R90 000. Xela, Yanga and Zea also agreed to the following (Tuck agreed to accept these conditions): 1. The accounting records of Xola, Yanga and Zea would be used for the new partnership 2. The non-current tangible assets of Xola, Yanga and Zea were all considered to be worth 20% more than their carrying amounts. 3. The debtors of the Xola Yanga and Zea partnership were carefully assessed, and it was agreed that a further expected credit loss of R2 500 should be provided for. 4. Goodwill was valued at R150 000 but because Zea had been the senior partner and very highly regarded in the community, Xola and Yanga decided that the value of goodwill would decrease by R50 000 when Zea withdrew. 5. In view of the lack of liquidity in the partnership of Xola, Yanga and Zea and because of Tuck's insolvency it was agreed that Xola and Yanga would pay, in their personal capacities and in their profit-sharing ratio, the amount due to Zea. 6. Tangible assets would be carried at the agreed values but goodwill would not be reflected in the new partnership of Xola, Yanga and Tuck. 7. Tuck would be entitled to 20% of the profits in the new partnership, the remaining profits being shared equally by Xola and Yanga. QUESTION 5 (continued) The following were the trial balances of the two partnerships on 31 October 2020 before effecting any adjustment for Zea's retirement, Tuck's admission or the final liquidation of the Sbu/Tuck partnership: SBU & TUCK DR CR R R XOLA, YANGA & ZEA DR CR R R 150 000 120 000 600 000 250 000 300 000 35 000 Capital: Xola Capital: Yanga Capital: Zea Capital: Sbu Capital: Tuck Current account: Zea Current account: Tuck Equipment, at cost Accumulated depreciation: Equipment Land, at cost Mortgage bond Accounts receivable Allowance for credit losses Accounts payable Cash at bank 280 000 330 000 650 000 275 000 140 000 800 000 600 000 200 000 10 000 37 000 20 000 177 000 R1 827 000 100 000 R710 000 R1 827 000 R710 000 The profit-sharing ratios in the two partnerships were: Xola : Yanga : Zea 1:1:2 Sbu : Tuck 3:1 REQUIRED: (a) (b) Prepare entries in general journal form (without narrations) to record the: The withdrawal of Zea _(102) The admission of Tuck. (372) You have been talking to your friend, Siya, about the dissolution of the one medical practice and the liquidation of another medical practice in Port Elizabeth. Your friend, not being familiar with the difference between the terminology 'dissolution' and 'liquidation' asks you what will happen to the assets in the medical practice being liquidated. Briefly explain to Siva what the difference is between dissolution and liquidation and what liquidation entries need to be processed by Sbu and Tuck (using figures from their accounting records), assuming that they sell their equipment for R30 000, and that Tuck is personally insolvent. Journal entries are not required. (4) Note: Show all workings clearly. Work to the nearest R1. QUESTION 5 _18 marks : 32 minutes) Xola, Yanga and Zea have been in partnership for many years in a medical practice. Zea has decided to emigrate. Another medical practice in Port Elizabeth (partners: Sby and Tuck) is in the process of being liquidated. Xola and Yanga decide to replace Zea with Tuck. After lengthy negotiations, it was decided that Zea would withdraw from the partnership on 31 October 2020 and that on the same day Tuck would be admitted. As Tuck is insolvent, he is not able to contribute any tangible assets, but Xola and Yanga agree that his expertise should be accorded a value of R90 000. Xela, Yanga and Zea also agreed to the following (Tuck agreed to accept these conditions): 1. The accounting records of Xola, Yanga and Zea would be used for the new partnership 2. The non-current tangible assets of Xola, Yanga and Zea were all considered to be worth 20% more than their carrying amounts. 3. The debtors of the Xola Yanga and Zea partnership were carefully assessed, and it was agreed that a further expected credit loss of R2 500 should be provided for. 4. Goodwill was valued at R150 000 but because Zea had been the senior partner and very highly regarded in the community, Xola and Yanga decided that the value of goodwill would decrease by R50 000 when Zea withdrew. 5. In view of the lack of liquidity in the partnership of Xola, Yanga and Zea and because of Tuck's insolvency it was agreed that Xola and Yanga would pay, in their personal capacities and in their profit-sharing ratio, the amount due to Zea. 6. Tangible assets would be carried at the agreed values but goodwill would not be reflected in the new partnership of Xola, Yanga and Tuck. 7. Tuck would be entitled to 20% of the profits in the new partnership, the remaining profits being shared equally by Xola and Yanga. QUESTION 5 (continued) The following were the trial balances of the two partnerships on 31 October 2020 before effecting any adjustment for Zea's retirement, Tuck's admission or the final liquidation of the Sbu/Tuck partnership: SBU & TUCK DR CR R R XOLA, YANGA & ZEA DR CR R R 150 000 120 000 600 000 250 000 300 000 35 000 Capital: Xola Capital: Yanga Capital: Zea Capital: Sbu Capital: Tuck Current account: Zea Current account: Tuck Equipment, at cost Accumulated depreciation: Equipment Land, at cost Mortgage bond Accounts receivable Allowance for credit losses Accounts payable Cash at bank 280 000 330 000 650 000 275 000 140 000 800 000 600 000 200 000 10 000 37 000 20 000 177 000 R1 827 000 100 000 R710 000 R1 827 000 R710 000 The profit-sharing ratios in the two partnerships were: Xola : Yanga : Zea 1:1:2 Sbu : Tuck 3:1 REQUIRED: (a) (b) Prepare entries in general journal form (without narrations) to record the: The withdrawal of Zea _(102) The admission of Tuck. (372) You have been talking to your friend, Siya, about the dissolution of the one medical practice and the liquidation of another medical practice in Port Elizabeth. Your friend, not being familiar with the difference between the terminology 'dissolution' and 'liquidation' asks you what will happen to the assets in the medical practice being liquidated. Briefly explain to Siva what the difference is between dissolution and liquidation and what liquidation entries need to be processed by Sbu and Tuck (using figures from their accounting records), assuming that they sell their equipment for R30 000, and that Tuck is personally insolvent. Journal entries are not required. (4) Note: Show all workings clearly. Work to the nearest R1