Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please answer for me this question by labeling step by step each answer e.g. 5.1 answer up to 5.8 QUESTION 5 (40 MARKS) Bino Lid

please answer for me this question by labeling step by step each answer e.g. 5.1 answer up to 5.8

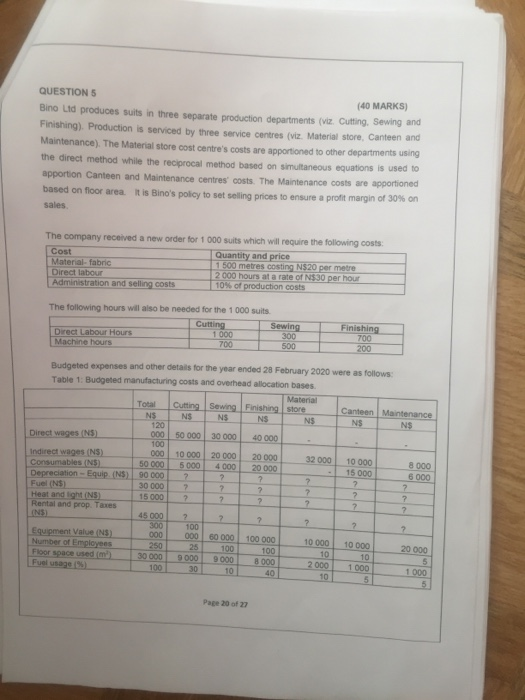

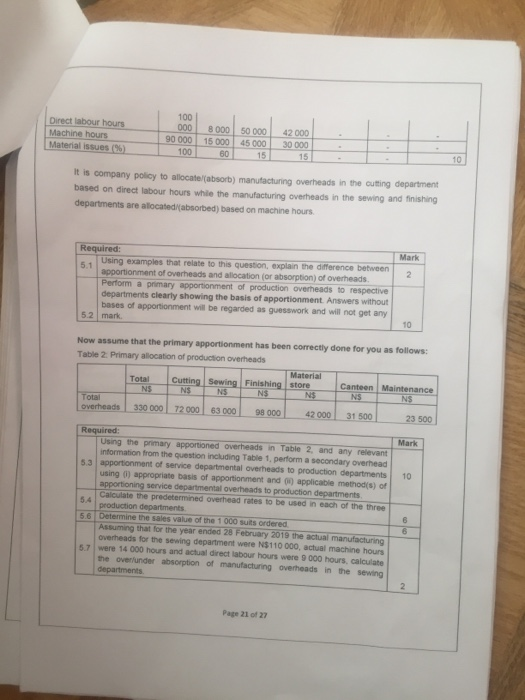

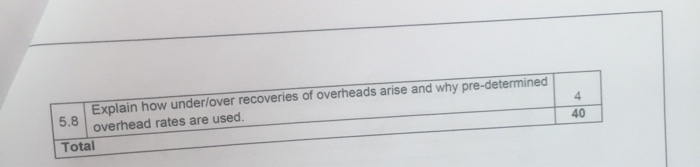

QUESTION 5 (40 MARKS) Bino Lid produces suits in three separate production departments (viz. Cutting Sewing and Finishing) Production is serviced by three service centres (viz. Material store, Canteen and Maintenance). The Material store cost centre's costs are apportioned to other departments using the direct method while the reciprocal method based on simultaneous equations is used to apportion Canteen and Maintenance centres costs. The Maintenance costs are apportioned based on floor area. It is Bino's policy to set selling prices to ensure a profit margin of 30% on sales The company received a new order for 1 000 suits which will require the following costs: Cost Quantity and price Material fabric 1 500 metres costing N$20 per metre Direct labour 12 000 hours at a rate of N$30 per hour Administration and selling costs 10% of production costs The following hours will also be needed for the 1000 suits Sewing Direct Labour Hours 1 000 Machine hours 500 Finishing 200 Budgeted expenses and other details for the year ended 28 February 2020 were as follows: Table 1: Budgeted manufacturing costs and overhead allocation bases. Material Total Cutting Sewing Finishing store Canteen Maintenance NS NS NS NS N$ NS 120 Direct wages (NS) 000 50 000 30 000 40 000 100 Indirect wages (NS) 000 10 000 20 000 20 000 32 000 10 000 8 000 Consumables (NS) 50 000 5 000 4 000 20 000 15 000 Depreciation - Equip (NS) 90 000 ? 6000 ? Fuel (NS) 30 000 7 7 Heat and ht(NS) 15 000 7 2 Rental and prop. Taxes 45 000 ? 100 Equipment ValueNS 000 000 60 000 100 000 10 000 10 000 Number of employees 250 25 100 100 20 000 10 Floor space used 10 30 000 9000 9000 8000 1000 100 300 40 1000 INS) 2000 10 Page 20 of 27 Direct labour hours Machine hours Material issues (%) 100 000 90 000 100 8000 50 000 15000 45000 00 15 42000 30 000 15 It is company policy to allocate absorb) manufacturing overheads in the cuting department based on direct labour hours while the manufacturing overheads in the sewing and finishing departments are allocated absorbed) based on machine hours. Required: Using examples that relate to this question explain the difference between apportionment of overheads and allocation or absorption) of Overheads Perform a primary apportionment of production overheads to respective departments clearly showing the basis of apportionment. Answers without bases of apportionment will be regarded as guesswork and will not get any 52 mark Now assume that the primary apportionment has been correctly done for you as follows: Table 2. Primary allocation of production overheads Material Total Cutting Sewing Finishing store Canteen Maintenance NS NS NS NS NS N S Total overheads 330 000 72 000 63000 98000 42 000 31500 Mark Required Using the primary apportioned overheads in Table 2 and any relevant information from the question including Table 1 perform a secondary overhead 5 3 apportionment of service departmental overheads to production departments using ) appropriate basis of apportionment and applicable method(s) of apportioning service departmental overheads to production departments Calculate the predetermined overhead rutes to be used in each of the three production departments 56 Determine the value of the 1000 suits ordered Assuming that for the year ended 28 February 2019 the actual manufacturing overheads for the sewing department were N$110 000, actual machine hours 5.7 were 14 000 hours and actual direct labour hours were 9 000 hours, calculate the overunder absorption of manufacturing overheads in the sewing departments Page 21 of 27 Explain how under/over recoveries of overheads arise and why pre-determined 5.8 overhead rates are used. Total QUESTION 5 (40 MARKS) Bino Lid produces suits in three separate production departments (viz. Cutting Sewing and Finishing) Production is serviced by three service centres (viz. Material store, Canteen and Maintenance). The Material store cost centre's costs are apportioned to other departments using the direct method while the reciprocal method based on simultaneous equations is used to apportion Canteen and Maintenance centres costs. The Maintenance costs are apportioned based on floor area. It is Bino's policy to set selling prices to ensure a profit margin of 30% on sales The company received a new order for 1 000 suits which will require the following costs: Cost Quantity and price Material fabric 1 500 metres costing N$20 per metre Direct labour 12 000 hours at a rate of N$30 per hour Administration and selling costs 10% of production costs The following hours will also be needed for the 1000 suits Sewing Direct Labour Hours 1 000 Machine hours 500 Finishing 200 Budgeted expenses and other details for the year ended 28 February 2020 were as follows: Table 1: Budgeted manufacturing costs and overhead allocation bases. Material Total Cutting Sewing Finishing store Canteen Maintenance NS NS NS NS N$ NS 120 Direct wages (NS) 000 50 000 30 000 40 000 100 Indirect wages (NS) 000 10 000 20 000 20 000 32 000 10 000 8 000 Consumables (NS) 50 000 5 000 4 000 20 000 15 000 Depreciation - Equip (NS) 90 000 ? 6000 ? Fuel (NS) 30 000 7 7 Heat and ht(NS) 15 000 7 2 Rental and prop. Taxes 45 000 ? 100 Equipment ValueNS 000 000 60 000 100 000 10 000 10 000 Number of employees 250 25 100 100 20 000 10 Floor space used 10 30 000 9000 9000 8000 1000 100 300 40 1000 INS) 2000 10 Page 20 of 27 Direct labour hours Machine hours Material issues (%) 100 000 90 000 100 8000 50 000 15000 45000 00 15 42000 30 000 15 It is company policy to allocate absorb) manufacturing overheads in the cuting department based on direct labour hours while the manufacturing overheads in the sewing and finishing departments are allocated absorbed) based on machine hours. Required: Using examples that relate to this question explain the difference between apportionment of overheads and allocation or absorption) of Overheads Perform a primary apportionment of production overheads to respective departments clearly showing the basis of apportionment. Answers without bases of apportionment will be regarded as guesswork and will not get any 52 mark Now assume that the primary apportionment has been correctly done for you as follows: Table 2. Primary allocation of production overheads Material Total Cutting Sewing Finishing store Canteen Maintenance NS NS NS NS NS N S Total overheads 330 000 72 000 63000 98000 42 000 31500 Mark Required Using the primary apportioned overheads in Table 2 and any relevant information from the question including Table 1 perform a secondary overhead 5 3 apportionment of service departmental overheads to production departments using ) appropriate basis of apportionment and applicable method(s) of apportioning service departmental overheads to production departments Calculate the predetermined overhead rutes to be used in each of the three production departments 56 Determine the value of the 1000 suits ordered Assuming that for the year ended 28 February 2019 the actual manufacturing overheads for the sewing department were N$110 000, actual machine hours 5.7 were 14 000 hours and actual direct labour hours were 9 000 hours, calculate the overunder absorption of manufacturing overheads in the sewing departments Page 21 of 27 Explain how under/over recoveries of overheads arise and why pre-determined 5.8 overhead rates are used. Total Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Auditing And Other Assurance Services

Authors: Ray Whittington, Kurt Pany

21st Edition

978-1259916984