Answered step by step

Verified Expert Solution

Question

1 Approved Answer

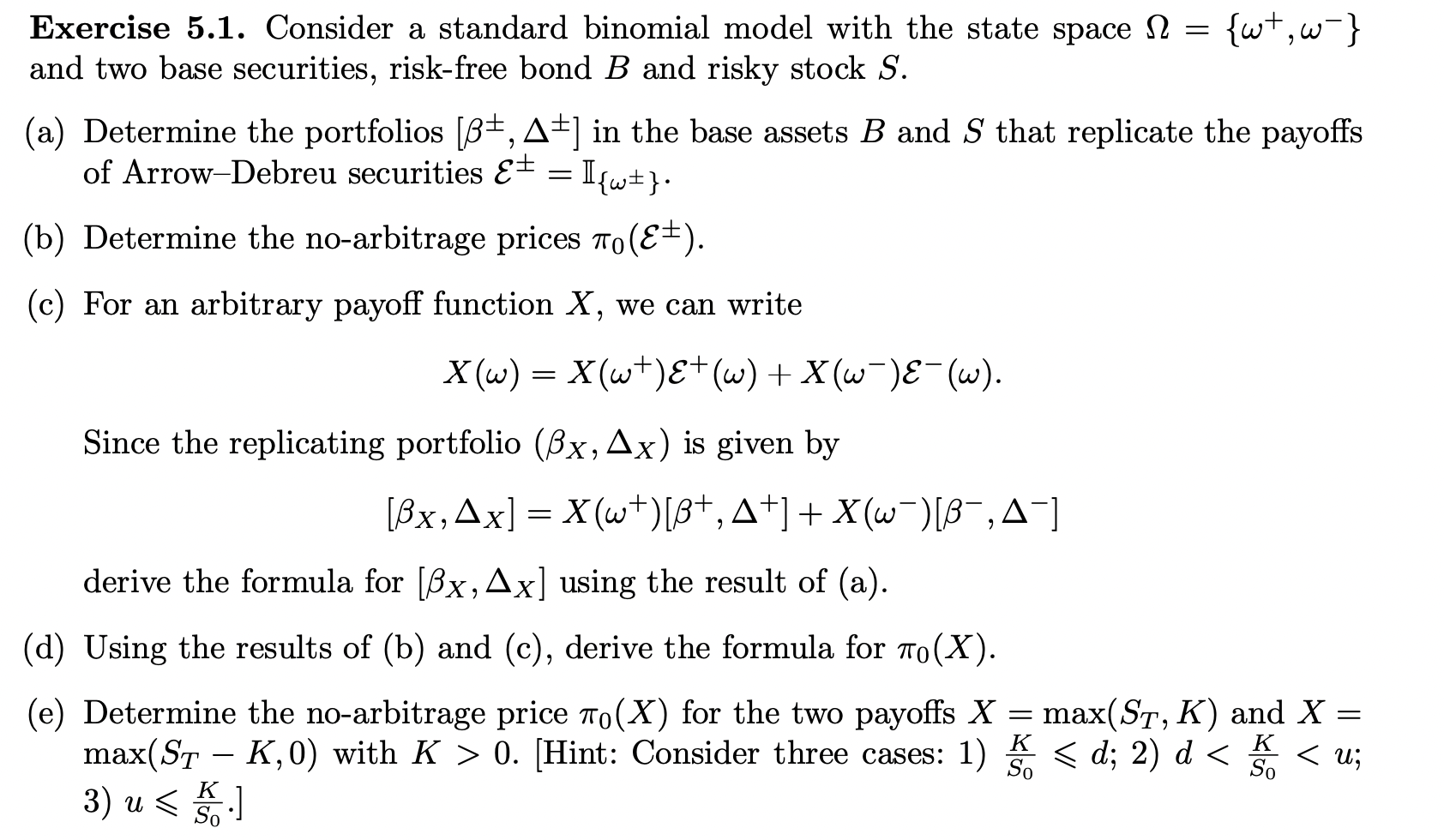

Please answer in detail showing all steps. Exercise 5.1. Consider a standard binomial model with the state space ={+,} and two base securities, risk-free bond

Please answer in detail showing all steps.

Exercise 5.1. Consider a standard binomial model with the state space ={+,} and two base securities, risk-free bond B and risky stock S. (a) Determine the portfolios [,]in the base assets B and S that replicate the payoffs of Arrow-Debreu securities E=I{}. (b) Determine the no-arbitrage prices 0(E). (c) For an arbitrary payoff function X, we can write X()=X(+)E+()+X()E(). Since the replicating portfolio (X,X) is given by [X,X]=X(+)[+,+]+X()[,] derive the formula for [X,X] using the result of (a). (d) Using the results of (b) and (c), derive the formula for 0(X). (e) Determine the no-arbitrage price 0(X) for the two payoffs X=max(ST,K) and X= max(STK,0) with K>0. [Hint: Consider three cases: 1) S0Kd;2)dStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

F For Quantitative Finance

Authors: Johan Astborg

1st Edition

1782164626, 978-1782164623