Question

Please answer only if you can answer all the questions correctly!!! Please Skip and leave for other experts if you cannot. I need proper explained

Please answer only if you can answer all the questions correctly!!! Please Skip and leave for other experts if you cannot. I need proper explained answers for each question.

31. A market risk manager seeks to calculate the price of a 2-year zero-coupon bond. The 1-year interest rate today is 10.0%. There is a 50% probability that the 1-year interest rate will be 12.0% and a 50% probability that it will be 8.0% in 1 year. Assuming the risk premium of duration risk is 50 bps each year, and the bonds face value is EUR 1,000, which of the following is the correct price of the zero-coupon bond? A. EUR 822.98 B. EUR 826.74 C. EUR 905.30 D. EUR 921.66

32. A financial analyst is pricing a 5-year call option on a 5-year Treasury note using a successfully validated pricing model. Current interest rate volatility is high, and the analyst is concerned about the effect this may have on short-term rates when pricing the option. Which of the following actions would best address the potential for negative short-term interest rates to arise in the model? A. When short-term rates are negative, the financial analyst adjusts the risk-neutral probabilities. B. When short-term rates are negative, the financial analyst increases the volatility. C. When short-term rates are negative, the financial analyst sets the rate to zero. D. When short-term rates are negative, the financial analyst sets the mean-reverting parameter to 1.

33. An investment bank has been using VaR as its main risk measurement tool. ES is suggested as a better alternative to use during market turmoil. What should be understood regarding VaR and ES before modifying current practices? A. For the same confidence level, ES is always greater than VaR. B. If a VaR backtest at a specified confidence level is accepted, then the corresponding ES will always be accepted. C. While VaR ensures that the estimate of portfolio risk is less than or equal to the sum of the risks of that portfolios positions, ES does not. D. While ES is more complicated to calculate than VaR, it is easier to backtest than VaR.

34. A derivative trading desk at a bank decides that its existing VaR model, which has been used broadly across the firm for several years, is too conservative. The existing VaR model uses a historical simulation over a 3-year look-back period, weighting each day equally. A quantitative analyst in the group quickly develops a new VaR model, which uses the delta-normal approach. The new model uses volatilities and correlations estimated over the past 4 years using the RiskMetrics EWMA method. For testing purposes, the new model is used in parallel with the existing model for 6 weeks to estimate the 1- day 99% VaR. After 6 weeks, the new VaR model has no exceedances despite consistently estimating VaR to be considerably lower than the existing model's estimates. The analyst argues that the lack of exceedances shows that the new model is unbiased and pressures the banks model evaluation team to agree. Following an overnight examination of the new model by one junior analyst, instead of the customary evaluation that takes several weeks and involves a senior member of the team, the model evaluation team agrees to accept the new model for use by the desk. Which of the following statements is a correct conclusion for this replacement? A. Delta-normal VaR is more appropriate than historical simulation VaR for assets with non-linear payoffs. B. Changing the look-back period and weighting scheme from 3 years, equally weighted, to 4 years, exponentially weighted, will understate the risk in the portfolio. C. Overnight examination by the junior analyst increased the desks exposure to model risk due to the potential for incorrect calibration and programming errors. D. A 99% VaR model that generates no exceedances in 6 weeks is necessarily conservative.

35. The senior management team of a small regional bank has established a committee to review procedures and implement best practices related to entering into significant contracts with third-party vendors. The committee is reviewing one proposed relationship with a third-party vendor who would have a significant responsibility for marketing the banks financial products to potential customers. In establishing policies to reduce the operational risk associated with this potential vendor contract, which of the following recommendations would be most appropriate? A. The bank should review all third-party audit reports of the vendor that are publicly available. B. The bank should ensure that the vendor's sales representatives are compensated mainly with commissions from the sale of the banks products. C. The bank should prevent the third-party vendor from having access to any of its critical processes. D. The bank should be responsible for developing the vendor's contingency planning process to mitigate risk exposure to the vendor.

36. The Basel Committee recommends that banks use a set of early warning indicators in order to identify emerging risks and potential vulnerabilities in their liquidity position. Which of the following is an early warning indicator of a potential liquidity problem?

A. Credit rating upgrade B. Increased asset diversification C. Rapid growth in the leverage ratio with significant dependence on short-term repo financing D. Decreased collateral haircuts applied to the banks collateralized exposures

38. During a training seminar, a supervisor at Firm W discusses different types of operational risk that the firm may face, which could be in the short-term or over a longer-term period. Which of the following is an example of a loss caused by an operational risk of Firm W? A. After a surprise announcement by the central bank that interest rates would increase, bond prices fall and Firm W incurs a significant loss on its bond portfolio. B. The data capture system of Firm W fails to capture the correct market rates causing derivative trades to be transacted at incorrect prices, resulting in significant losses. C. As a result of an increase in commodity prices, the share price of a company that Firm W invested in falls significantly, causing major investment losses. D. A counterparty of Firm W fails to settle its debt to Firm W, and in doing this, it is in breach of a legal agreement to pay for services rendered.

39. A bank owned several retail branch buildings that were destroyed in a hurricane. A financial analyst at the bank wants to determine the correct costs to include in reporting this loss in its operational risk event database. Which of the following costs associated with this loss should be included in the operational loss report? A. Costs of insurance premiums paid to insure the buildings before the storm took place B. A provision for the estimated opportunity costs of lost banking business at the affected branches C. Legal costs paid to obtain construction permits to rebuild the destroyed branch buildings D. Costs of a program to train branch managers on ways to prepare buildings to mitigate potential damage from future hurricanes

40. A risk analyst is implementing an enterprise risk management system at a bank. During the process, the analyst takes an inventory of risks faced by the bank and categorizes these risks as market, credit, or operational risks. Which of the following observations of the banks data should be considered unexpected if compared to similar industry data? A. The operational risk loss distribution has many small losses, and therefore a relatively low mode. B. The operational risk loss distribution is symmetric and fat-tailed. C. The credit risk distribution is asymmetric and fat-tailed. D. The market risk distribution is symmetric.

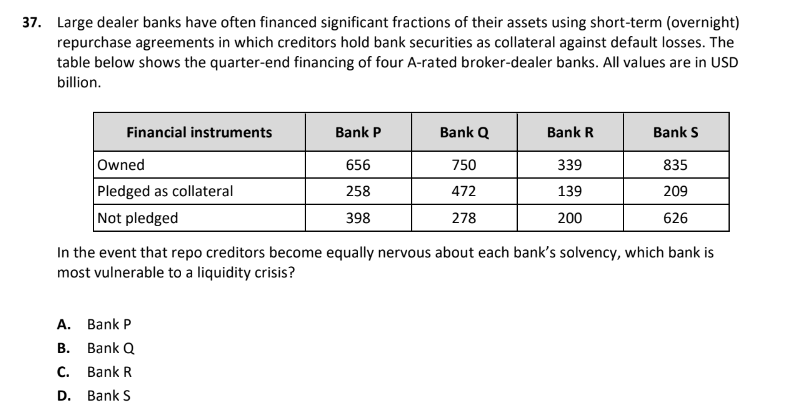

Large dealer banks have often financed significant fractions of their assets using short-term (overnight) repurchase agreements in which creditors hold bank securities as collateral against default losses. The table below shows the quarter-end financing of four A-rated broker-dealer banks. All values are in USD billion. In the event that repo creditors become equally nervous about each bank's solvency, which bank is most vulnerable to a liquidity crisis? A. Bank P B. Bank Q C. Bank R D. Bank SStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials Of Managerial Finance

Authors: Scott Besley, Eugene F. Brigham

13th Edition

0324258755, 9780324258752