Answered step by step

Verified Expert Solution

Question

1 Approved Answer

PLEASE ANSWER PART C _03 P9-50. TED Analyzing and Interpreting Disclosures on Consolidations Snap-on Incorporated consists of two business units: the manufacturing company (parent corporation)

PLEASE ANSWER PART C

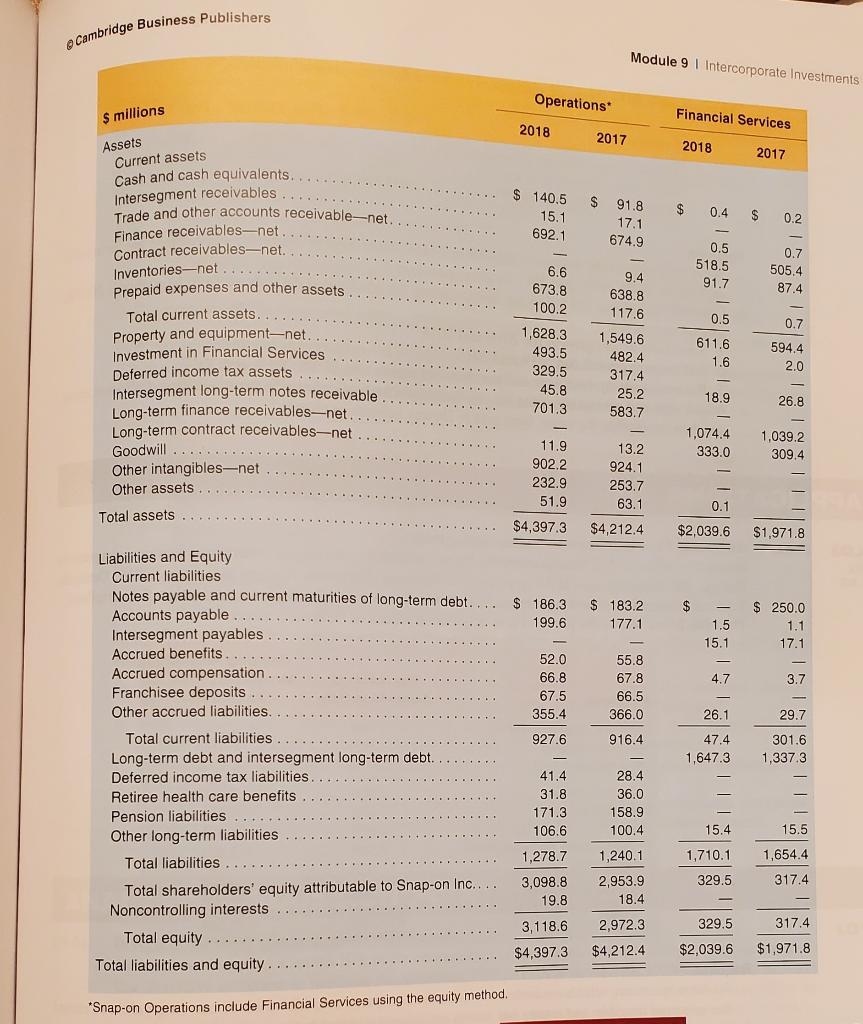

_03 P9-50. TED Analyzing and Interpreting Disclosures on Consolidations Snap-on Incorporated consists of two business units: the manufacturing company (parent corporation) and a wholly-owned finance subsidiary. These two units are consolidated in Snap-on's 10-K report. Fol- lowing is a supplemental disclosure Snap-on includes in its 10-K report that shows the separate balance sheets of the parent and the subsidiary. This supplemental disclosure is not mandated under GAAP but is voluntarily reported by Snap-on as useful information for investors and creditors. Using this disclosure, answer the following questions. Required a. Do the parent and subsidiary companies each maintain their own financial statements? Explain. Why does GAAP require consolidation instead of separate financial statements of individual companies? b. What is the balance of Investments in Financial Services as of December 31, 2018, on the parent's balance sheet? What is the equity balance of the financial services subsidiary to which this relates as of December 31, 2018? Do you see a relation? Will this relation always exist? c. Refer to your answer for part a. How does the equity method of accounting for the investment in the subsidiary obscure the actual financial condition of the parent company as compared with the con- solidated financial statements? d. Recall that the parent company uses the equity method of accounting for its investment in the sub- sidiary and that this account is eliminated in the consolidation process. What is the relation between consolidated net income and the net income of the parent company? Explain. e. What is the implication for the consolidated balance sheet if the fair value of the financial services subsidiary (subsequent to acquisition) is greater than the book value of its stockholders' equity? Cambridge Business Publishers Module 9 1 Intercorporate Investments Operations $ millions Financial Services 2018 2017 2018 Assets Current assets 2017 $ $ 140.5 15.1 692.1 $ 0.4 $ 91.8 17.1 674.9 0.2 0.5 518.5 91.7 9.4 638.8 117.6 0.7 505.4 87.4 0.5 0.7 Cash and cash equivalents. Intersegment receivables Trade and other accounts receivable-net. Finance receivables-net Contract receivables-net. Inventories-net Prepaid expenses and other assets Total current assets.... Property and equipment-net. Investment in Financial Services Deferred income tax assets Intersegment long-term notes receivable Long-term finance receivables-net. Long-term contract receivables-net Goodwill ........ Other intangibles.net Other assets 6.6 673.8 100.2 1,628.3 493.5 329.5 45.8 701.3 611.6 1.6 594,4 2.0 1,549.6 482.4 317.4 25.2 583.7 18.9 26.8 1,074.4 333.0 13.2 924.1 1,039.2 309.4 11.9 902.2 232.9 253.7 51.9 $ 63.1 0.1 Total assets $4,397.3 $4,212.4 $2,039.6 $1.971.8 $ - $ 186.3 199.6 $ 183.2 177.1 1.5 15.1 $ 250.0 1.1 17.1 4.7 3.7 52.0 66.8 67.5 355.4 55.8 67.8 66.5 366.0 916.4 26.1 29.7 927.6 Liabilities and Equity Current liabilities Notes payable and current maturities of long-term debt. Accounts payable Intersegment payables Accrued benefits Accrued compensation Franchisee deposits Other accrued liabilities. Total current liabilities Long-term debt and intersegment long-term debt. Deferred income tax liabilities. Retiree health care benefits Pension liabilities Other long-term liabilities Total liabilities Total shareholders' equity attributable to Snap-on Inc.... Noncontrolling interests Total equity Total liabilities and equity 47.4 1.647.3 301.6 1,337.3 41.4 31.8 171.3 106.6 28.4 36.0 158.9 100.4 15.4 15.5 1,278.7 1,240.1 1,710.1 329.5 1,654.4 317.4 3,098.8 19.8 2,953.9 18.4 329.5 317.4 3,118.6 $4,397.3 2,972.3 $4,212.4 $2,039.6 $1,971.8 *Snap-on Operations include Financial Services using the equity method. _03 P9-50. TED Analyzing and Interpreting Disclosures on Consolidations Snap-on Incorporated consists of two business units: the manufacturing company (parent corporation) and a wholly-owned finance subsidiary. These two units are consolidated in Snap-on's 10-K report. Fol- lowing is a supplemental disclosure Snap-on includes in its 10-K report that shows the separate balance sheets of the parent and the subsidiary. This supplemental disclosure is not mandated under GAAP but is voluntarily reported by Snap-on as useful information for investors and creditors. Using this disclosure, answer the following questions. Required a. Do the parent and subsidiary companies each maintain their own financial statements? Explain. Why does GAAP require consolidation instead of separate financial statements of individual companies? b. What is the balance of Investments in Financial Services as of December 31, 2018, on the parent's balance sheet? What is the equity balance of the financial services subsidiary to which this relates as of December 31, 2018? Do you see a relation? Will this relation always exist? c. Refer to your answer for part a. How does the equity method of accounting for the investment in the subsidiary obscure the actual financial condition of the parent company as compared with the con- solidated financial statements? d. Recall that the parent company uses the equity method of accounting for its investment in the sub- sidiary and that this account is eliminated in the consolidation process. What is the relation between consolidated net income and the net income of the parent company? Explain. e. What is the implication for the consolidated balance sheet if the fair value of the financial services subsidiary (subsequent to acquisition) is greater than the book value of its stockholders' equity? Cambridge Business Publishers Module 9 1 Intercorporate Investments Operations $ millions Financial Services 2018 2017 2018 Assets Current assets 2017 $ $ 140.5 15.1 692.1 $ 0.4 $ 91.8 17.1 674.9 0.2 0.5 518.5 91.7 9.4 638.8 117.6 0.7 505.4 87.4 0.5 0.7 Cash and cash equivalents. Intersegment receivables Trade and other accounts receivable-net. Finance receivables-net Contract receivables-net. Inventories-net Prepaid expenses and other assets Total current assets.... Property and equipment-net. Investment in Financial Services Deferred income tax assets Intersegment long-term notes receivable Long-term finance receivables-net. Long-term contract receivables-net Goodwill ........ Other intangibles.net Other assets 6.6 673.8 100.2 1,628.3 493.5 329.5 45.8 701.3 611.6 1.6 594,4 2.0 1,549.6 482.4 317.4 25.2 583.7 18.9 26.8 1,074.4 333.0 13.2 924.1 1,039.2 309.4 11.9 902.2 232.9 253.7 51.9 $ 63.1 0.1 Total assets $4,397.3 $4,212.4 $2,039.6 $1.971.8 $ - $ 186.3 199.6 $ 183.2 177.1 1.5 15.1 $ 250.0 1.1 17.1 4.7 3.7 52.0 66.8 67.5 355.4 55.8 67.8 66.5 366.0 916.4 26.1 29.7 927.6 Liabilities and Equity Current liabilities Notes payable and current maturities of long-term debt. Accounts payable Intersegment payables Accrued benefits Accrued compensation Franchisee deposits Other accrued liabilities. Total current liabilities Long-term debt and intersegment long-term debt. Deferred income tax liabilities. Retiree health care benefits Pension liabilities Other long-term liabilities Total liabilities Total shareholders' equity attributable to Snap-on Inc.... Noncontrolling interests Total equity Total liabilities and equity 47.4 1.647.3 301.6 1,337.3 41.4 31.8 171.3 106.6 28.4 36.0 158.9 100.4 15.4 15.5 1,278.7 1,240.1 1,710.1 329.5 1,654.4 317.4 3,098.8 19.8 2,953.9 18.4 329.5 317.4 3,118.6 $4,397.3 2,972.3 $4,212.4 $2,039.6 $1,971.8 *Snap-on Operations include Financial Services using the equity methodStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting For Non-Accountants

Authors: David Horner

12th Edition

1789664306, 9781789664300