Answered step by step

Verified Expert Solution

Question

1 Approved Answer

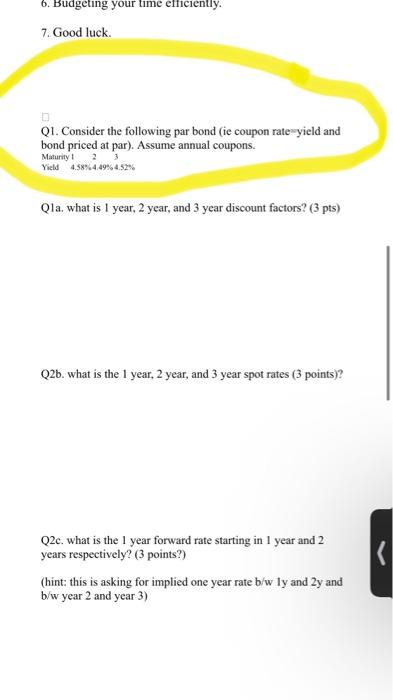

please answer Q2C only!!! based on whats citcled above Q1. Consider the following par bond (ie coupon rateryield and bond priced at par). Assume annual

please answer Q2C only!!! based on whats citcled above

Q1. Consider the following par bond (ie coupon rateryield and bond priced at par). Assume annual coupons. Q1a. what is 1 year, 2 year, and 3yeardiscountfactors? Q2b. what is the 1 year, 2 year, and 3 year spot rates (3 points)? Q2c. what is the 1 year forward rate starting in 1 year and 2 years respectively? ( 3 points?) (hint: this is asking for implied one year rate b/w 1y and 2y and b/w year 2 and year 3 ) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Finance For Dummies

Authors: Ayse Evrensel

1st Edition

111852389X, 978-1118523896