Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer Question d. i and ii. thank you d) Suppose that you are quoted the following NZD/FC spot and forward rates. Spot bid-ask 3-month

Please answer Question d. i and ii.

thank you

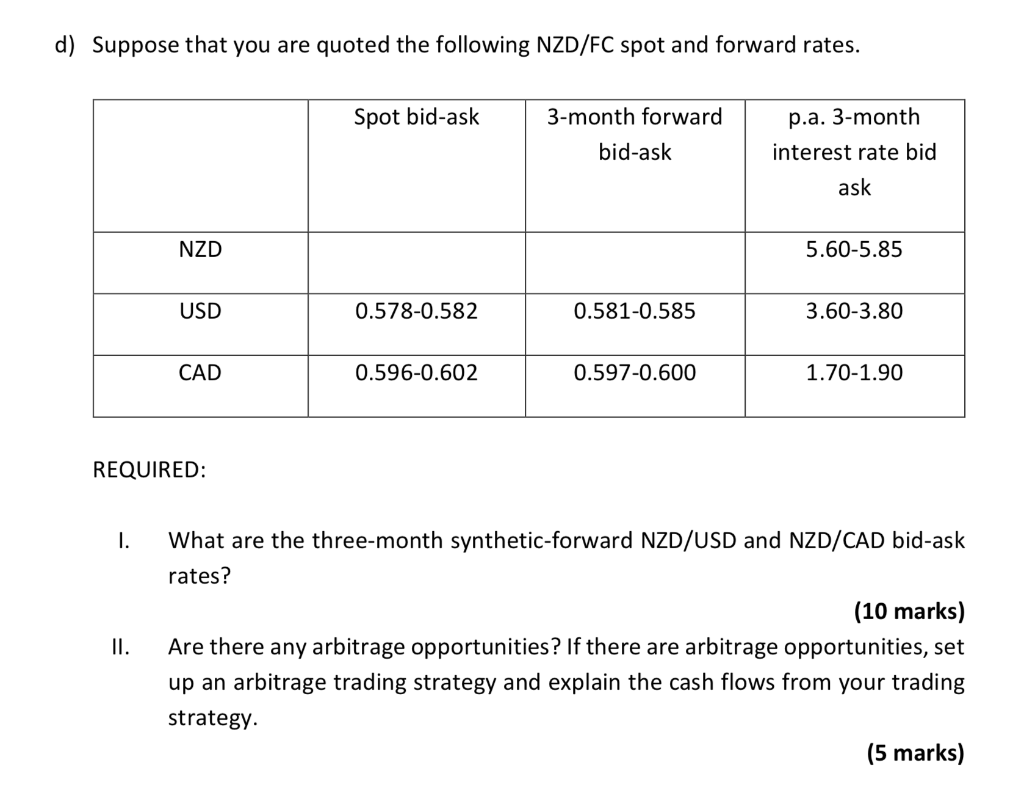

d) Suppose that you are quoted the following NZD/FC spot and forward rates. Spot bid-ask 3-month forward bid-ask p.a. 3-month interest rate bid ask NZD 5.60-5.85 USD 0.578-0.582 0.581-0.585 3.60-3.80 CAD 0.596-0.602 0.597-0.600 1.70-1.90 REQUIRED: I. What are the three-month synthetic-forward NZD/USD and NZD/CAD bid-ask rates? (10 marks) II. Are there any arbitrage opportunities? If there are arbitrage opportunities, set up an arbitrage trading strategy and explain the cash flows from your trading strategy. (5 marks) d) Suppose that you are quoted the following NZD/FC spot and forward rates. Spot bid-ask 3-month forward bid-ask p.a. 3-month interest rate bid ask NZD 5.60-5.85 USD 0.578-0.582 0.581-0.585 3.60-3.80 CAD 0.596-0.602 0.597-0.600 1.70-1.90 REQUIRED: I. What are the three-month synthetic-forward NZD/USD and NZD/CAD bid-ask rates? (10 marks) II. Are there any arbitrage opportunities? If there are arbitrage opportunities, set up an arbitrage trading strategy and explain the cash flows from your trading strategyStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Agua Sangre Life Is What Happens While You Re Making Other Plans

Authors: David Dawei

1st Edition

979-8355381578