Answered step by step

Verified Expert Solution

Question

1 Approved Answer

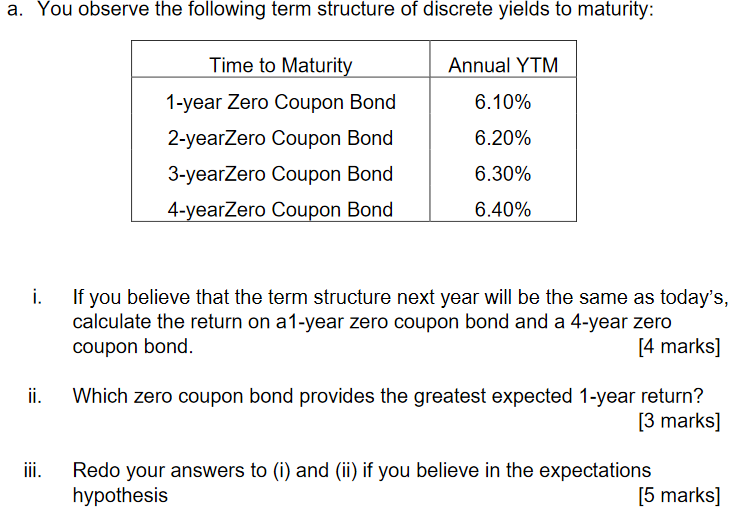

please answer question i, ii and iii thank you very much for your help a. You observe the following term structure of discrete yields to

please answer question i, ii and iii

thank you very much for your help

a. You observe the following term structure of discrete yields to maturity: Time to Maturity Annual YTM 6.10% 6.20% 1-year Zero Coupon Bond 2-yearZero Coupon Bond 3-yearZero Coupon Bond 4-yearZero Coupon Bond 6.30% 6.40% i. If you believe that the term structure next year will be the same as today's, calculate the return on a 1-year zero coupon bond and a 4-year zero coupon bond. [4 marks] ii. Which zero coupon bond provides the greatest expected 1-year return? [3 marks] iii. Redo your answers to (i) and (ii) if you believe in the expectations hypothesis [5 marks]Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management for Public Health and Not for Profit Organizations

Authors: Steven A. Finkler, Thad Calabrese

4th edition

133060411, 132805669, 9780133060416, 978-0132805667