Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer questions 1 through 7 on Requirements for Part 1. Case information Beginning of the year: January 1, 2021 GSO Furniture, Inc. recently hired

Please answer questions 1 through 7 on Requirements for Part 1.

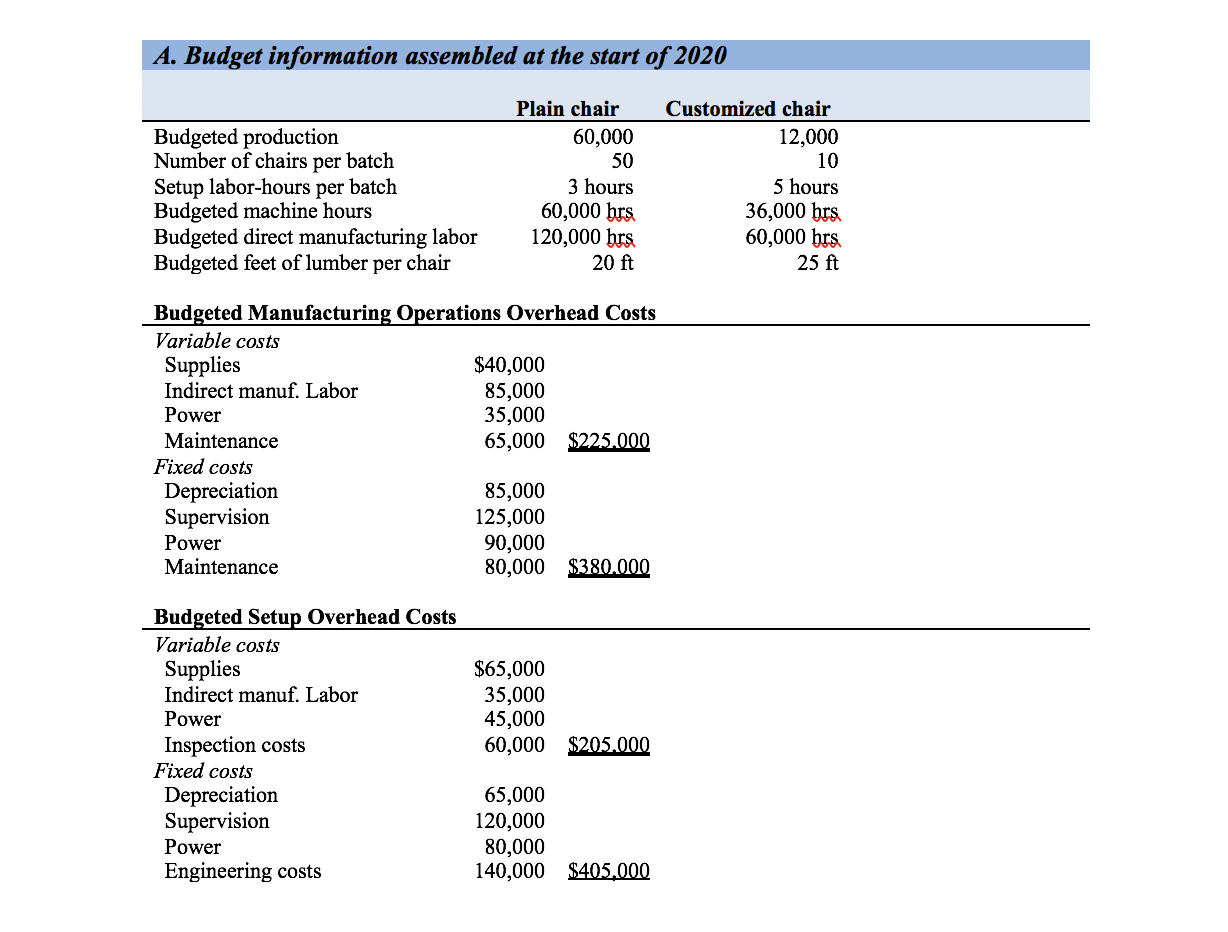

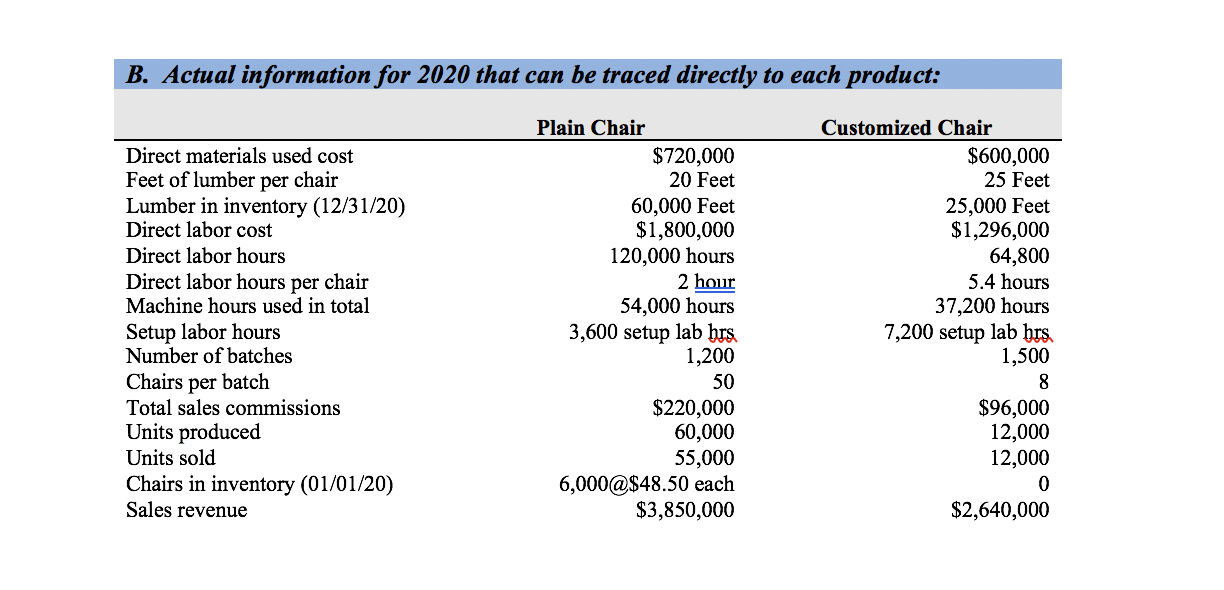

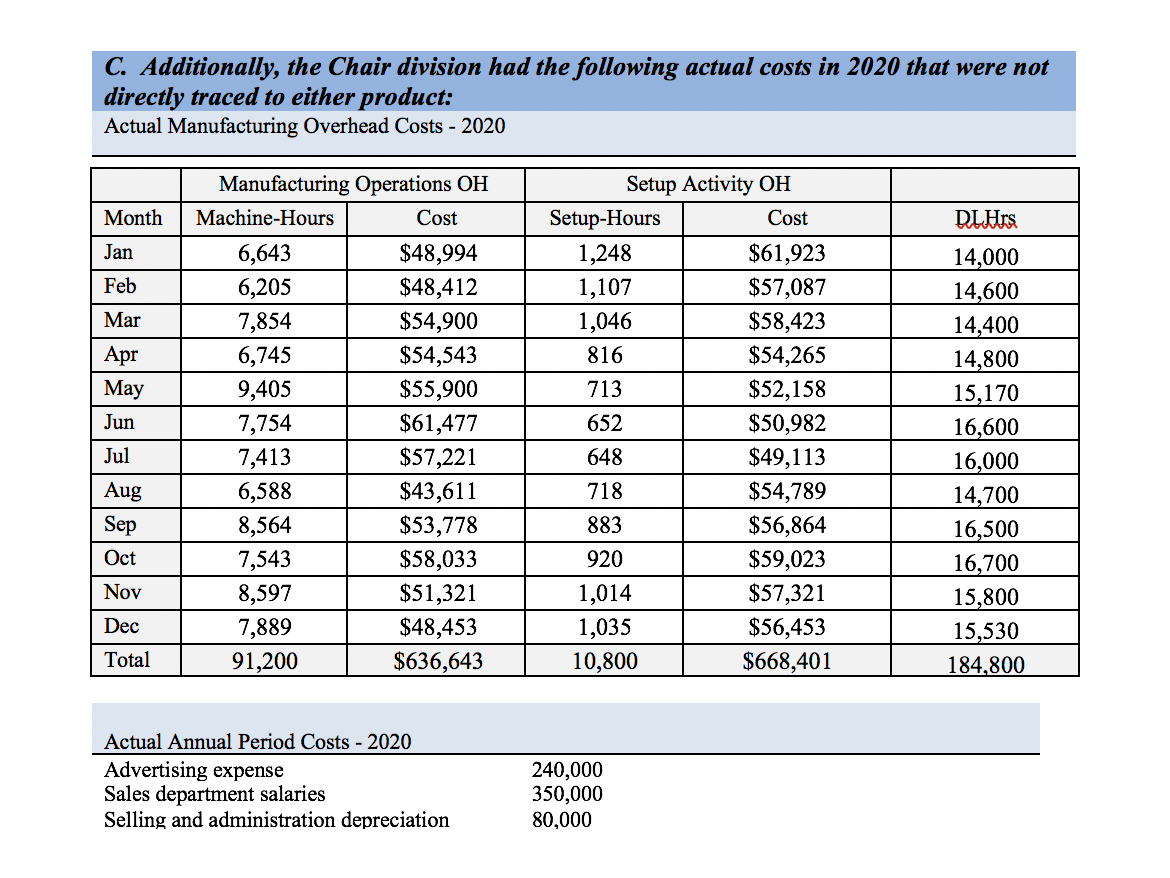

Case information Beginning of the year: January 1, 2021 GSO Furniture, Inc. recently hired your team to head up its chair division. GSO Furniture's chair division produces two products, a plain poplar chair and a customized red oak wood chair that has a finish and carvings chosen by the customer. Customized chairs are a recent innovation for the company and executives are encouraged by the projected sales growth for these chairs. Although the chair division was once the biggest contributor to GSO's success, recently performance has been challenged. It is your job to return the division to its former glory. In response to demands for more relevant costing information your predecessor introduced an ABC system. Two key production activities, 1) manufacturing operations and 2) machine setups, were identified. Production costs related to these activities are now assigned to the two lines of chairs based on the cost drivers of 1) machine-hours and 2) setup labor-hours, respectively. The old product costing system allocated all manufacturing overhead based on direct manufacturing labor hours. Your predecessor argued for a move to ABC because production runs for the custom chairs take longer to setup and allocating setup costs based on setup labor-hours better represents resources consumed by the two chair lines. The chair division is growing in complexity and part of your job is to manage and explain the more advanced accounting information systems used within the division. Cost leadership had been the focus of GSO's strategy in recent years. This approach had been called into question with the rise of the custom chair, which commanded and achieved a premium price. Customers appeared to pay limited attention to price increases for the custom chair. However, it was a different matter with established customers for the plain chair. These customers were grumbling about GSO prices and threatening to defect to the competition, especially those producers who concentrated solely on the plain chair market. An added challenge for GSO was the internal disputes amongst production and marketing managers. Disputes circled around slow response to marketing demands for expedited complex rush orders on the one hand and disruptive, short production runs causing inefficiencies in manufacturing on the other. These disputes were diverting attention away from the traditional plain chair market. After carefully arranging your corner office, you ask your assistant for the division's budget for 2021. To your dismay you are told that the division's records are in disarray and the budget can't be located. Since you are short on time you decide to use the information from the last year's (2020) records to conduct an initial examination of the division. These records include some budget estimates assembled before the start of 2020, and actual information for the year 2020. A. Budget information assembled at the start of 2020 Budgeted production Number of chairs per batch Setup labor-hours per batch Budgeted machine hours Budgeted direct manufacturing labor Budgeted feet of lumber per chair Plain chair 60,000 50 3 hours 60,000 hrs 120,000 hrs 20 ft Customized chair 12,000 10 5 hours 36,000 hrs 60,000 hrs 25 ft Budgeted Manufacturing Operations Overhead Costs Variable costs Supplies $40,000 Indirect manuf. Labor 85,000 Power 35,000 Maintenance 65,000 $225.000 Fixed costs Depreciation 85,000 Supervision 125,000 Power 90,000 Maintenance 80,000 $380.000 Budgeted Setup Overhead Costs Variable costs Supplies Indirect manuf. Labor Power Inspection costs Fixed costs Depreciation Supervision Power Engineering costs $65,000 35,000 45,000 60,000 $205.000 65,000 120,000 80,000 140,000 $405.000 B. Actual information for 2020 that can be traced directly to each product: Direct materials used cost Feet of lumber per chair Lumber in inventory (12/31/20) Direct labor cost Direct labor hours Direct labor hours per chair Machine hours used in total Setup labor hours Number of batches Chairs per batch Total sales commissions Units produced Units sold Chairs in inventory (01/01/20) Sales revenue Plain Chair $720,000 20 Feet 60,000 Feet $1,800,000 120,000 hours 2 hour 54,000 hours 3,600 setup lab hrs 1,200 50 $220,000 60,000 55,000 6,000@$48.50 each $3,850,000 Customized Chair $600,000 25 Feet 25,000 Feet $1,296,000 64,800 5.4 hours 37,200 hours 7,200 setup lab brs 1,500 8 $96,000 12,000 12,000 0 $2,640,000 C. Additionally, the Chair division had the following actual costs in 2020 that were not directly traced to either product: Actual Manufacturing Overhead Costs - 2020 Month Jan Feb Mar Apr May Jun Manufacturing Operations OH Machine-Hours Cost 6,643 $48,994 6,205 $48,412 7,854 $54,900 6,745 $54,543 9,405 $55,900 7,754 $61,477 7,413 $57,221 6,588 $43,611 8,564 $53,778 7,543 $58,033 8,597 $51,321 7,889 $48,453 91,200 $636,643 Setup Activity OH Setup-Hours Cost 1,248 $61,923 1,107 $57,087 1,046 $58,423 816 $54,265 713 $52,158 652 $50,982 648 $49,113 718 $54,789 883 $56,864 920 $59,023 1,014 $57,321 1,035 $56,453 10,800 $668,401 DLHrs 14,000 14,600 14,400 14,800 15,170 16,600 16, 14,700 16,500 16,700 15,800 15,530 184,800 Jul Aug Sep Oct Nov Dec Total Actual Annual Period Costs - 2020 Advertising expense Sales department salaries Selling and administration depreciation 240,000 350,000 80,000 . o D. Based on the information you have gathered you also make the following assumptions: Because of past financial trouble in the division, all expenses must be paid in cash. No sales are made on account (all sales are cash sales). Information for the 2021 budget is as follows: The budgeted input quantities for materials, labor and MOH (machine hours and setup labor hours) used in 2020 will also be used in the 2021 budget, except for budgeted DLHr/unit for the custom chair, which is revised up to 5.25 DL Hrs/chair. The cost of Poplar is expected to increase by 10% and Red Oak is expected to increase by 15% in 2021 over 2020 actual costs. Budgeted labor rates in 2021 are expected to be the same as actual rates in 2020. Calculate 2021 budgeted variable moh rates and total fixed moh costs from 2020 actual monthly cost and activity data. Use Regression Analysis to determine estimates for variable and monthly fixed costs. Convert monthly estimates of fixed costs into annual costs. Assume non-cash (e.g., depreciation) MOH item amounts remain unchanged from budgeted 2020 data. Production and sales forecasts are within the relevant range. Budgeted period costs: variable costs per unit and fixed costs in total for 2021 are assumed to be the same as actual period costs in 2020. A 2% increase in selling price for 2021 is expected for the Plain model and a 5% increase is expected for the Customized model. O o o o o 3 . . . Normal costing is used. There are two cost drivers for manufacturing overhead costs - machine-hours and setup labor-hours. Machine-hours is the cost driver for the variable portion of manufacturing operations overhead. Machine-hours is also used to allocate the fixed portion of manufacturing operations overhead. Setup labor-hours is the cost driver for the variable portion of machine setup overhead. Setup labor- hours is also used to allocate the fixed portion of machine setup overhead. Projected sales for the plain chair are 62,500 in 2021, 56,000 in 2022, and 58,000 in 2023. Projected sales for the customized chair are 12,500 in 2021, 15,000 in 2022, and 16,000 in 2023. Sales commission is paid as a rate per chair sold. 2021 input cost and quantity standards for direct material, direct manufacturing labor and manufacturing overhead are the same as 2021 budgeted input costs and quantities. You require an ending inventory of plain cha of 25% of next year's total ales need nized chairs are made to order and no inventory of finished goods is planned. You require an ending raw material inventory of 10% of next year's production needs for both product lines) Your beginning 2021 cash balance is $320,000. The company requires a minimum cash balance of $250,000. Assume a FIFO cost flow Assume no WIP inventory. O . Requirements for Part 1 - due Friday, October 15 Actual and Normal Costing, CVP analysis, and Activity-Based Costing a. 1. What were the 2020 budgeted indirect cost rates for the manufacturing operations activity and the machine setup activity? 2. Was overhead over- or under-applied for the year? By how much? Use @IF statements to indicate under-/over-applied MOH. 3. What was the unit product cost for the plain and customized Chairs under normal costing in 2020? 4. What was the Chair Division's operating income for 2020? Use normal costing and adjust for mis- applied MOH. 5. Use the 2020 actual monthly MOH information to calculate annual estimates of cost behavior (fixed and variable components) for each MOH activity. Use the High-Low method to separate variable and fixed costs. For this exercise use @VLOOKUP, @MAX, and @MIN excel functions. b. Use the Regression function found under Data: Data Analysis in Excel. Place output on a separate sheet. These estimates will be used for the 2021 budget. 6. For the Manufacturing Operations overhead activity, evaluate the selected cost driver (MHrs) and compare it to the alternative of Direct Labor Hours as the cost driver. Refer to Exhibit 10-19. i.e., run a regression for DLHrs, as the cost driver for the Manufacturing Operations activity and compare the results according to the criteria in Ex 10-19. 7. Calculate the break-even point in units (calculate the number of units of each product required), and the number of units of both products that must be sold to earn an operating income of $325,000. Use 2021 budgeted information refer to section D bullet point 2 and your results from requirement 5. Case information Beginning of the year: January 1, 2021 GSO Furniture, Inc. recently hired your team to head up its chair division. GSO Furniture's chair division produces two products, a plain poplar chair and a customized red oak wood chair that has a finish and carvings chosen by the customer. Customized chairs are a recent innovation for the company and executives are encouraged by the projected sales growth for these chairs. Although the chair division was once the biggest contributor to GSO's success, recently performance has been challenged. It is your job to return the division to its former glory. In response to demands for more relevant costing information your predecessor introduced an ABC system. Two key production activities, 1) manufacturing operations and 2) machine setups, were identified. Production costs related to these activities are now assigned to the two lines of chairs based on the cost drivers of 1) machine-hours and 2) setup labor-hours, respectively. The old product costing system allocated all manufacturing overhead based on direct manufacturing labor hours. Your predecessor argued for a move to ABC because production runs for the custom chairs take longer to setup and allocating setup costs based on setup labor-hours better represents resources consumed by the two chair lines. The chair division is growing in complexity and part of your job is to manage and explain the more advanced accounting information systems used within the division. Cost leadership had been the focus of GSO's strategy in recent years. This approach had been called into question with the rise of the custom chair, which commanded and achieved a premium price. Customers appeared to pay limited attention to price increases for the custom chair. However, it was a different matter with established customers for the plain chair. These customers were grumbling about GSO prices and threatening to defect to the competition, especially those producers who concentrated solely on the plain chair market. An added challenge for GSO was the internal disputes amongst production and marketing managers. Disputes circled around slow response to marketing demands for expedited complex rush orders on the one hand and disruptive, short production runs causing inefficiencies in manufacturing on the other. These disputes were diverting attention away from the traditional plain chair market. After carefully arranging your corner office, you ask your assistant for the division's budget for 2021. To your dismay you are told that the division's records are in disarray and the budget can't be located. Since you are short on time you decide to use the information from the last year's (2020) records to conduct an initial examination of the division. These records include some budget estimates assembled before the start of 2020, and actual information for the year 2020. A. Budget information assembled at the start of 2020 Budgeted production Number of chairs per batch Setup labor-hours per batch Budgeted machine hours Budgeted direct manufacturing labor Budgeted feet of lumber per chair Plain chair 60,000 50 3 hours 60,000 hrs 120,000 hrs 20 ft Customized chair 12,000 10 5 hours 36,000 hrs 60,000 hrs 25 ft Budgeted Manufacturing Operations Overhead Costs Variable costs Supplies $40,000 Indirect manuf. Labor 85,000 Power 35,000 Maintenance 65,000 $225.000 Fixed costs Depreciation 85,000 Supervision 125,000 Power 90,000 Maintenance 80,000 $380.000 Budgeted Setup Overhead Costs Variable costs Supplies Indirect manuf. Labor Power Inspection costs Fixed costs Depreciation Supervision Power Engineering costs $65,000 35,000 45,000 60,000 $205.000 65,000 120,000 80,000 140,000 $405.000 B. Actual information for 2020 that can be traced directly to each product: Direct materials used cost Feet of lumber per chair Lumber in inventory (12/31/20) Direct labor cost Direct labor hours Direct labor hours per chair Machine hours used in total Setup labor hours Number of batches Chairs per batch Total sales commissions Units produced Units sold Chairs in inventory (01/01/20) Sales revenue Plain Chair $720,000 20 Feet 60,000 Feet $1,800,000 120,000 hours 2 hour 54,000 hours 3,600 setup lab hrs 1,200 50 $220,000 60,000 55,000 6,000@$48.50 each $3,850,000 Customized Chair $600,000 25 Feet 25,000 Feet $1,296,000 64,800 5.4 hours 37,200 hours 7,200 setup lab brs 1,500 8 $96,000 12,000 12,000 0 $2,640,000 C. Additionally, the Chair division had the following actual costs in 2020 that were not directly traced to either product: Actual Manufacturing Overhead Costs - 2020 Month Jan Feb Mar Apr May Jun Manufacturing Operations OH Machine-Hours Cost 6,643 $48,994 6,205 $48,412 7,854 $54,900 6,745 $54,543 9,405 $55,900 7,754 $61,477 7,413 $57,221 6,588 $43,611 8,564 $53,778 7,543 $58,033 8,597 $51,321 7,889 $48,453 91,200 $636,643 Setup Activity OH Setup-Hours Cost 1,248 $61,923 1,107 $57,087 1,046 $58,423 816 $54,265 713 $52,158 652 $50,982 648 $49,113 718 $54,789 883 $56,864 920 $59,023 1,014 $57,321 1,035 $56,453 10,800 $668,401 DLHrs 14,000 14,600 14,400 14,800 15,170 16,600 16, 14,700 16,500 16,700 15,800 15,530 184,800 Jul Aug Sep Oct Nov Dec Total Actual Annual Period Costs - 2020 Advertising expense Sales department salaries Selling and administration depreciation 240,000 350,000 80,000 . o D. Based on the information you have gathered you also make the following assumptions: Because of past financial trouble in the division, all expenses must be paid in cash. No sales are made on account (all sales are cash sales). Information for the 2021 budget is as follows: The budgeted input quantities for materials, labor and MOH (machine hours and setup labor hours) used in 2020 will also be used in the 2021 budget, except for budgeted DLHr/unit for the custom chair, which is revised up to 5.25 DL Hrs/chair. The cost of Poplar is expected to increase by 10% and Red Oak is expected to increase by 15% in 2021 over 2020 actual costs. Budgeted labor rates in 2021 are expected to be the same as actual rates in 2020. Calculate 2021 budgeted variable moh rates and total fixed moh costs from 2020 actual monthly cost and activity data. Use Regression Analysis to determine estimates for variable and monthly fixed costs. Convert monthly estimates of fixed costs into annual costs. Assume non-cash (e.g., depreciation) MOH item amounts remain unchanged from budgeted 2020 data. Production and sales forecasts are within the relevant range. Budgeted period costs: variable costs per unit and fixed costs in total for 2021 are assumed to be the same as actual period costs in 2020. A 2% increase in selling price for 2021 is expected for the Plain model and a 5% increase is expected for the Customized model. O o o o o 3 . . . Normal costing is used. There are two cost drivers for manufacturing overhead costs - machine-hours and setup labor-hours. Machine-hours is the cost driver for the variable portion of manufacturing operations overhead. Machine-hours is also used to allocate the fixed portion of manufacturing operations overhead. Setup labor-hours is the cost driver for the variable portion of machine setup overhead. Setup labor- hours is also used to allocate the fixed portion of machine setup overhead. Projected sales for the plain chair are 62,500 in 2021, 56,000 in 2022, and 58,000 in 2023. Projected sales for the customized chair are 12,500 in 2021, 15,000 in 2022, and 16,000 in 2023. Sales commission is paid as a rate per chair sold. 2021 input cost and quantity standards for direct material, direct manufacturing labor and manufacturing overhead are the same as 2021 budgeted input costs and quantities. You require an ending inventory of plain cha of 25% of next year's total ales need nized chairs are made to order and no inventory of finished goods is planned. You require an ending raw material inventory of 10% of next year's production needs for both product lines) Your beginning 2021 cash balance is $320,000. The company requires a minimum cash balance of $250,000. Assume a FIFO cost flow Assume no WIP inventory. O . Requirements for Part 1 - due Friday, October 15 Actual and Normal Costing, CVP analysis, and Activity-Based Costing a. 1. What were the 2020 budgeted indirect cost rates for the manufacturing operations activity and the machine setup activity? 2. Was overhead over- or under-applied for the year? By how much? Use @IF statements to indicate under-/over-applied MOH. 3. What was the unit product cost for the plain and customized Chairs under normal costing in 2020? 4. What was the Chair Division's operating income for 2020? Use normal costing and adjust for mis- applied MOH. 5. Use the 2020 actual monthly MOH information to calculate annual estimates of cost behavior (fixed and variable components) for each MOH activity. Use the High-Low method to separate variable and fixed costs. For this exercise use @VLOOKUP, @MAX, and @MIN excel functions. b. Use the Regression function found under Data: Data Analysis in Excel. Place output on a separate sheet. These estimates will be used for the 2021 budget. 6. For the Manufacturing Operations overhead activity, evaluate the selected cost driver (MHrs) and compare it to the alternative of Direct Labor Hours as the cost driver. Refer to Exhibit 10-19. i.e., run a regression for DLHrs, as the cost driver for the Manufacturing Operations activity and compare the results according to the criteria in Ex 10-19. 7. Calculate the break-even point in units (calculate the number of units of each product required), and the number of units of both products that must be sold to earn an operating income of $325,000. Use 2021 budgeted information refer to section D bullet point 2 and your results from requirement 5Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Financial Accounting (Chapters 1-17)

Authors: John Wild

25th Edition

1260780147, 9781260780147