Answered step by step

Verified Expert Solution

Question

1 Approved Answer

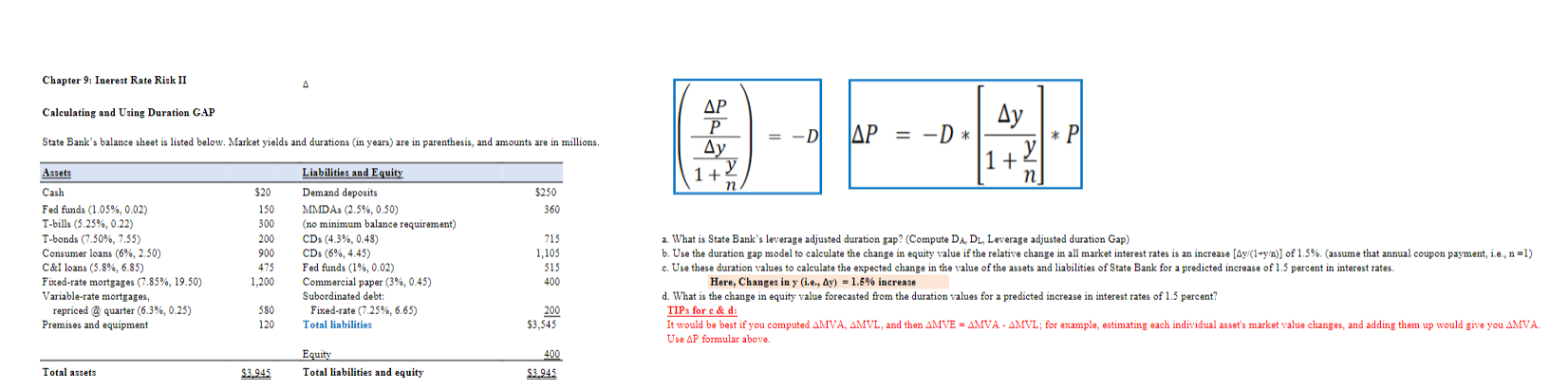

Please answer questions a-d. Thanks! Chapter 9: Inerest Rate Risk II (1+nyyPP)=D P=D[1+nyy]P c. Use these duration values to calculate the expected change in the

Please answer questions a-d. Thanks!

Please answer questions a-d. Thanks!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Build An Online Retail System For Under $150

Authors: Roger Butterworth

1st Edition

1530170044, 978-1530170043