Question

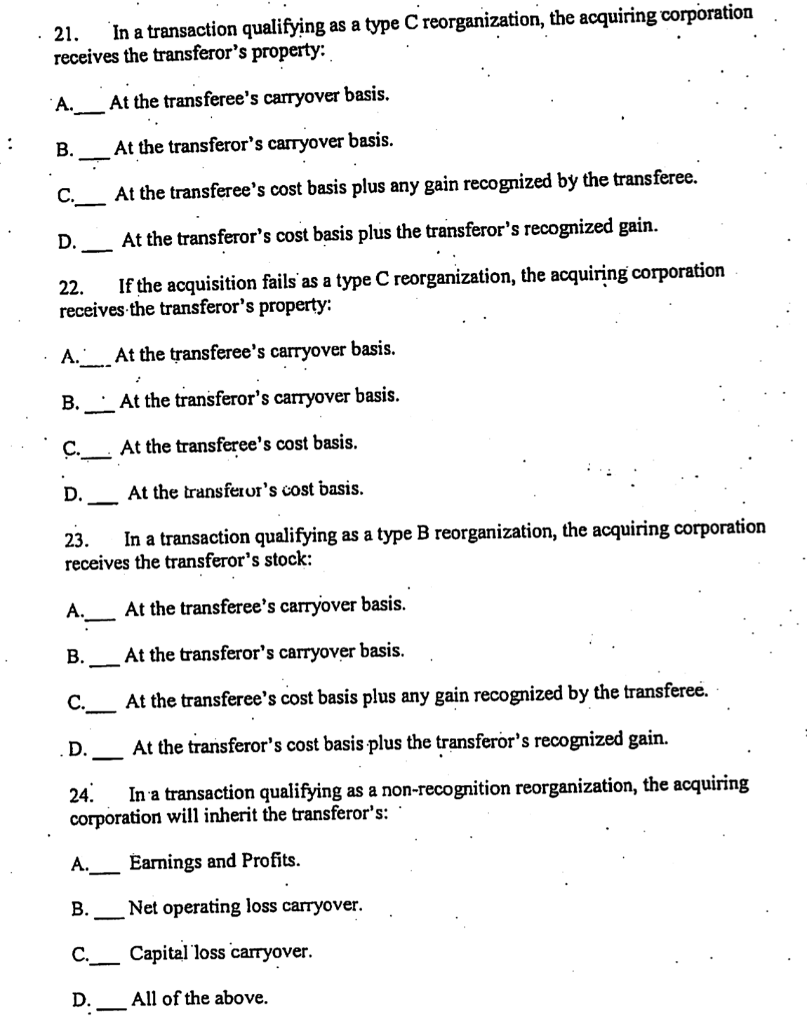

Please answer the # 21-27 multiple choice questions: 21. In a transaction qualifying as a type C reorganization, the acquiring corporation receives the transferors property:

Please answer the # 21-27 multiple choice questions:

21. In a transaction qualifying as a type C reorganization, the acquiring corporation receives the transferors property:

-

At the transferees carryover basis.

-

At the transferors carryover basis.

-

At the transferees cost basis plus any gain recognized by the transferee.

-

At the transferors cost basis plus the transferors recognized gain.

22. If the acquisition fails as a type C reorganization, the acquiring corporation receives the transferors property:

-

At the transferees carryover basis.

-

At the transferors carryover basis.

-

At the transferees cost basis

-

At the transferors cost basis.

23. In a transaction qualifying as a type B reorganization, the acquiring corporation receives the transferors stock:

-

At the transferees carryover basis.

-

At the transferors carryover basis.

-

At the transferees cost basis plus any again recognized by the transferee.

-

At the transferors cost basis plus the transferors recognized gain.

24. In a transaction qualifying as a non-recognition reorganization, the acquiring corporation will inherit the transferors:

-

Earnings and profits.

-

Net operating loss carryover.

-

Capital loss carryover.

-

All of the above.

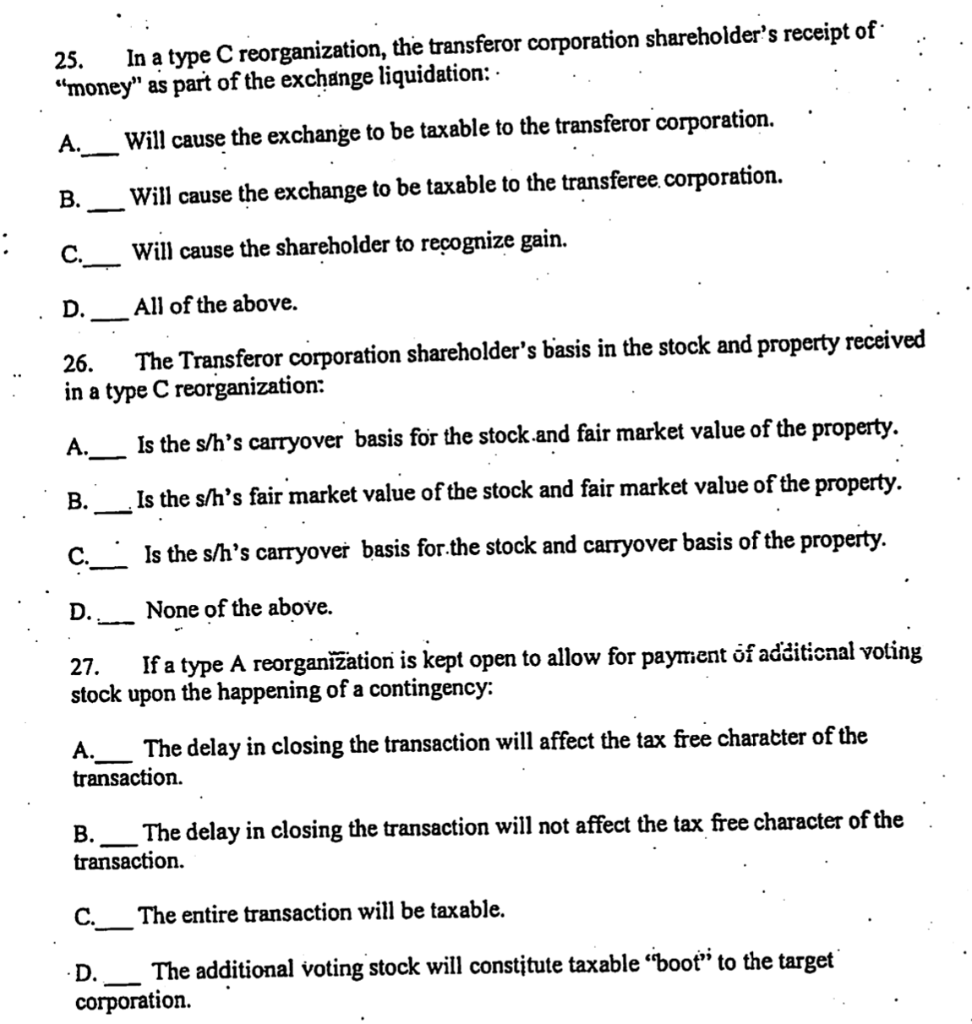

25. In a type C reorganization, the transferor corporation shareholders receipt of money as part of the exchange liquidation:

-

Will cause the exchange to be taxable to the transferor corporation

-

Will cause the exchange to be taxable to the transferee corporation.

-

Will cause the shareholder to recognize gain.

-

All of the above.

26. The transferor corporation shareholders basis in the stock and property received in a type C reorganization:

-

Is the shareholders carryover basis for the stock and fair market value of the property.

-

Is the shareholders fair market value of the stock and fair market value of the property.

-

Is the shareholders carryover basis for the stock and carryover basis of the property.

-

None of the above.

27. If a type A reorganization is kept open to allow for payment of additional voting stock upon the happening of a contingency:

-

The delay in closing the transaction will affect the tax free character of the transaction.

-

The delay in closing the transaction will not affect the tax free character of the transaction.

-

The entire transaction will be taxable.

-

The additional voting stock will constitute taxable boot to the target Corporation.

Textbook: Federal Income Taxation of Corporations and Shareholders, 7th Edition

Course: Taxation of Reorganizations & Liquidations

21. In a transaction qualifying as a type C reorganization, the acquiring corporation receives the transferor's property: A. _ At the transferee's carryover basis. y At the transferor's carryover basis. At the transferee's cost basis plus any gain recognized by the transferee. D. _ At the transferor's cost basis plus the transferor's recognized gain. 22. If the acquisition fails as a type C reorganization, the acquiring corporation receives the transferor's property: A. At the transferee's carryover basis. B.. At the transferor's carryover basis. At the transferee's cost basis. D._At the transferur's cost basis. 23. In a transaction qualifying as a type B reorganization, the acquiring corporation receives the transferor's stock: A._ At the transferee's carryover basis. At the transferor's carryover basis. At the transferee's cost basis plus any gain recognized by the transferee. - At the transferor's cost basis plus the transferor's recognized gain. 24. In a transaction qualifying as a non-recognition reorganization, the acquiring corporation will inherit the transferor's: A. __ Earnings and Profits. Net operating loss carryover. C. _ Capital loss carryover. All of the above. 25. In a type C reorganization, the transferor corporation shareholder's receipt of money" as part of the exchange liquidation: .. . A. __ Will cause the exchange to be taxable to the transferor corporation... B. __ Will cause the exchange to be taxable to the transferee.corporation. c. __ Will cause the shareholder to recognize gain. D. All of the above. 26. The Transferor corporation shareholder's basis in the stock and property received in a type C reorganization: A.__ Is the s/h's carryover basis for the stock.and fair market value of the property. B. _ Is the s/h's fair market value of the stock and fair market value of the property. c.__ Is the s/h's carryover basis for the stock and carryover basis of the property. D. None of the above. 27. If a type A reorganization is kept open to allow for paymient of additional voting stock upon the happening of a contingency: A. __ The delay in closing the transaction will affect the tax free character of the transaction. B. ___ The delay in closing the transaction will not affect the tax free character of the transaction. c. The entire transaction will be taxable. D. _ The additional voting stock will constitute taxable boot to the target corporation. 21. In a transaction qualifying as a type C reorganization, the acquiring corporation receives the transferor's property: A. _ At the transferee's carryover basis. y At the transferor's carryover basis. At the transferee's cost basis plus any gain recognized by the transferee. D. _ At the transferor's cost basis plus the transferor's recognized gain. 22. If the acquisition fails as a type C reorganization, the acquiring corporation receives the transferor's property: A. At the transferee's carryover basis. B.. At the transferor's carryover basis. At the transferee's cost basis. D._At the transferur's cost basis. 23. In a transaction qualifying as a type B reorganization, the acquiring corporation receives the transferor's stock: A._ At the transferee's carryover basis. At the transferor's carryover basis. At the transferee's cost basis plus any gain recognized by the transferee. - At the transferor's cost basis plus the transferor's recognized gain. 24. In a transaction qualifying as a non-recognition reorganization, the acquiring corporation will inherit the transferor's: A. __ Earnings and Profits. Net operating loss carryover. C. _ Capital loss carryover. All of the above. 25. In a type C reorganization, the transferor corporation shareholder's receipt of money" as part of the exchange liquidation: .. . A. __ Will cause the exchange to be taxable to the transferor corporation... B. __ Will cause the exchange to be taxable to the transferee.corporation. c. __ Will cause the shareholder to recognize gain. D. All of the above. 26. The Transferor corporation shareholder's basis in the stock and property received in a type C reorganization: A.__ Is the s/h's carryover basis for the stock.and fair market value of the property. B. _ Is the s/h's fair market value of the stock and fair market value of the property. c.__ Is the s/h's carryover basis for the stock and carryover basis of the property. D. None of the above. 27. If a type A reorganization is kept open to allow for paymient of additional voting stock upon the happening of a contingency: A. __ The delay in closing the transaction will affect the tax free character of the transaction. B. ___ The delay in closing the transaction will not affect the tax free character of the transaction. c. The entire transaction will be taxable. D. _ The additional voting stock will constitute taxable boot to the target corporationStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Microeconomics

Authors: Michael Parkin

6th Edition

0321112075, 9780321112071